We were on the road marketing last week, and the following editorial summarises some discussions with investors. Beyond the themes discussed in our editorial, our report discusses three issues:

- The Automotive sector: We revisit our stance (UW) after the strong performance YTD and stick to our UW rating: Pricing challenges in 2024 in the EU/US, China competition on global markets, the shrinking ICE (internal combustion engine) market in China.

- The Software & Services sector: We revisit our stance (N) after the strong performance YTD and stick to our N rating: it is difficult not to argue for a bullish fundamental case on earnings growth for Software, but valuations are getting stretched.

- ECB: We join consensus on our first interest-rate cut assumption in June and provide an update on European macro conditions. Labour continues to surprise positively despite the weak economic momentum, which involves a wait and see approach with regards to rate cuts from the ECB in early Q2.

At the end of last year, we used the English saying “Be careful what you wish for” to warn investors that the process of falling policy rates should be coupled with worsening economic momentum, as it usually does. One wants to own stocks when the cycle gets stronger - not the other way around. We still think that this classic pattern could be at work, as the US consumer has been boosted by a lot of fiscal support and low rates (locked-in in 2020/21), which are fading. This has become a very secondary question in investors’ lists of concerns, telling us that investors are expecting a “no landing” scenario.

In any case, since the timing of this economic cycle has proven to be very unusual, the common wisdom has been to “buy now, think later” as interest-rate cuts approached. This does not mean that investors lost their minds, but rather that the above classic thesis clashed with two gigantic coincidental positive drivers: 1) the levels of cash in portfolios a year ago were such that a process of FOMO (fear of missing out) started; and 2) the world discovered ChatGPT, probably the first “wow” effect since the iPhone was first launched almost 17 years ago. In some way, this also feeds this FOMO. It is evident with retail investors, although less so among professional investors, who are warming up to SMID Caps as a possible diversification.

Gigantic driver number one seems to be a story of the past, in our view, as positioning has become pretty extreme in US equities. In Europe the concept has been translated to the large, liquid, high quality growth companies. It is apparent that many European investors have become forced buyers of low freefloat companies such as Hermès and Ferrari that are in Eurostoxx 50. Said differently, there aren’t that many places to hide.

Where we stand on the “ChatGPT” rally (gigantic driver number two) is more complicated to assess, but we note the flurry of articles/commentators/fund managers out there arguing that “today is not March 2000” for a number of reasons. These people say “stay invested”, “buy the highs”, etc. And there are good reasons for that. The productivity benefits of AI are likely to filter through in the coming years and make a positive case for the economic cycle. In the meantime, the numbers being generated by US Big Techs are mind-blowing (absolute earnings, earnings growth, valuation, market capitalisation).

The consensual view is that as long as a strong antitrust case does not materialise, they have more power/resources to keep growing their share of the pool of the Western world’s profits. While it is hard to argue against that, this case is becoming quite mature and some fatigue is likely to set in. Technical analysis suggests that this situation is not far off.

In summary, we think that the US elections and a US slowdown are key fundamental triggers to temper the current “risk-on” mood, as some fatigue is likely to become evident in the current leadership of Big Techs (it’s more a case of “the Magnificent 4” than the “Magnificent 7” this year). We note that US economic surprises have started to reverse, but it is early days to be buy aggressively long dated Treasuries in our view.

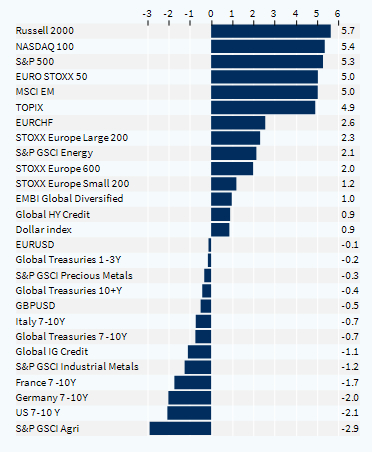

Weekly asset classes performance (%)