There is always a psychological barrier when you get close to record highs, and equity markets in Europe and the US are now just 3-5% short of early 2002 levels, when interest rates were at 0%.

One associated question is how long it will take to get there, and how far above equity markets can go in 2024. In our view, the upside is limited in price return terms in Europe and the US, considering the growth and inflation deceleration. But taking into account dividends and buybacks, our medium-term stance on equities is not too defensive, at slight Underweight.

- Recent macro releases still to point to a robust pace of job creation in the US, which should continue to support consumption. The strength of the labour market, nonetheless, tends to be a lagging indicator for markets, and we see no reason to reconsider our views.

In this special edition of our weekly report, we dig into eight key calls from a cross-asset perspective, following the release of our 2024 outlook.

- Key call #1: bull steepening of the EUR yield curve. We believe inflation is starting to be something of the past. Although fixed income markets have started to price in sharp rate cuts from central banks in 2024, any pushback from them next week during their regular monetary policy meetings would offer attractive entry points.

- Key call #2: IG credit, bank tier 2, corporate hybrids. IG credit keeps an attractive risk/ reward profile, while we are more selective on high yield ahead of the growth deceleration that is taking shape in Europe. With regards to corporate hybrids and financials, yields are very elevated, while extension risk has receded, with the majority of hybrid issuers having exercised the call at the first call date.

- Key call #3: increase bond duration. We find equities richly valued versus bonds and expect the bond market rally that has started to take shape to continue into 2024 as inflation keeps falling. Next week, the US CPI release for November should see an additional easing in price pressures.

- Key call #4: reduce Japanese equities. The BoJ is in a corner. It wants to normalise monetary policy, but the window of opportunity is closing, as other global central banks have finished their rate hike cycle. The USD/JPY has room to fall substantially, which would be a severe headwind for Japanese equities after a great run in 2023.

- Key call #5: EM equities, prefer Brazil/India in core EM. We find valuation appeal in EM equities on top of significant growth potential in countries such as Brazil and India. Brazil is cheaply valued, oil production is rising fast, politics are quiet. India is richly valued but should be the growth star of the next decade. Investors should not focus too much on valuation, as India is structurally richly valued due to its Tech bias. China could surprise on the upside.

- Key call 6: reweighting some growth sectors in European equities. Although our overall sector allocation maintains a value bias, we upgrade MedTech and luxury, two growth sectors, on the back recent weakness and support from lower yields ahead. We also upgrade professional and business services. We downgraded Pharma, and we still favour the high dividend style.

- Key call #7: OW EM sovereign credit in hard currency. Yields are near 8%, while sovereign risk in core emerging markets is low. EM central banks are ahead of the curve with regards to rate cuts, and external balance sheets are strong, suggesting refinancing in USD is not an issue. Political risk appears highly manageable as well.

- Key call #8: buy gold in commodities. We stay constructive on gold in 2024, though the recent rally suggests a pause is due. Falling interest rates, a complex geopolitical environment, and strong demand from EM central banks are likely to lift gold prices to new highs. Energy commodities deserve a tactical look after the severe pullback recently.

Week ahead:

- The US CPI for November, as well as the ECB/Fed monetary policy meetings, will be key milestones. The consensus expects US inflation to have marginally decelerated to 3.1% YOY from 3.2% in October, while the core CPI is expected to have remained unchanged at 4%. US retail sales and industrial production for November will also be released.

- We expect the Fed/ECB to keep rates on hold, but not yet (explicitly) pivot. The median dot for the end-2024 Fed funds rate will be revised down by 25bps to 4.875%, in our view.

- In China, retail sales and industrial production figures for November will also be available. The consensus expects a rebound, which has failed to materialise so far this year.

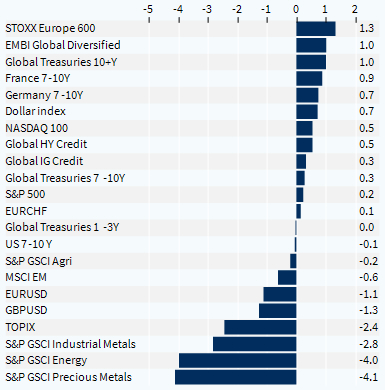

Asset classes performance (1 week)