A single word is enough to stop the wind. Market sentiment is prone to flip-flops, much like the US administration. The pace at which the news flow has changed is impressive. Just a week ago, we were deeply concerned about an escalation in the Middle East and considering hedging geopolitical risk with crude oil. But the story has changed, just like concerns over section 899 of the US fiscal bill, whose controversial revenge tax was scrapped at the end of last week.

In the near term, we believe that US equity markets will test new highs. The earnings season is about to start, expectations are low, and the US administration is likely to announce trade deals ahead of the July 9 deadline. Meanwhile, July is historically one of the best-performing months before adverse seasonality starts in August/September.

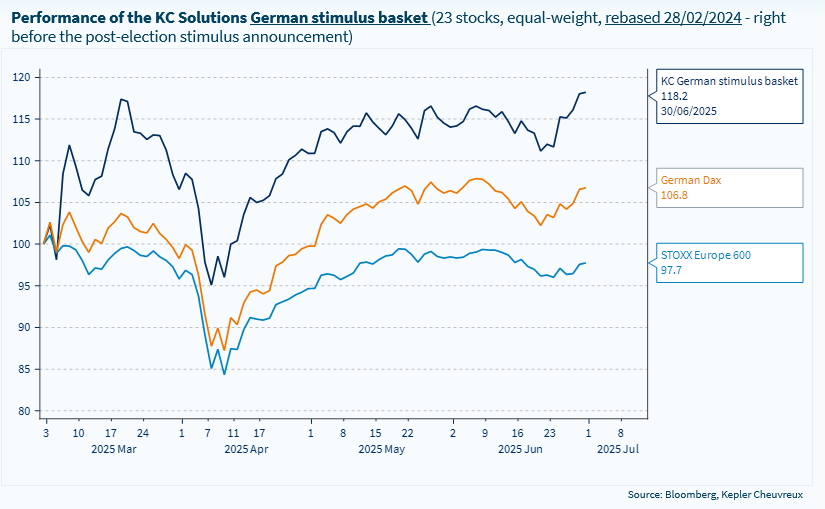

In Europe, the German cabinet approved last week a draft budget for 2025 and a budget framework for 2026. An important headline around this budget draft was the announcement of record investments to revive the economy and a strong commitment to defence spending. The drafts include investments of 116bn EUR in 2025 and 124bn EUR in 2026, which marks a 55% increase from 75bn EUR in 2024. By 2029, the federal government’s investments are planned to remain at a level of ca 120bn EUR a year. These investments are split between the core budget (mainly defence), the Infrastructure and Climate Neutrality Special Fund (the famous 500bn EUR package) and the Climate and Transformation Fund (KTF).

How to play it? In the report, we provide an update of Kepler Cheuvreux’s German stimulus and German midcap equity baskets which are particularly appealing in this context. The defence theme also pushed higher in recent days amid NATO’s members commitment to increase defence spending to 5% of GDP. Considering the stellar performance of European defence stocks, we advocate for a global approach to the theme, with US, Asian and European names.

Week ahead: A spate of data releases on the US labour market will shed light on a potential slowdown of the US economy (job openings for May, non-farm payrolls for June. The ISM business survey will also be released. In the euro area, the June CPI is expected to have stabilized at 1.9% yoy. In Japan, the Tankan survey will help towards anticipating the next steps for the BoJ which is likely to end its rate hike cycle in H2-2025. In China, the PMIs will provide insights into a potential improvement in growth dynamics.

This week's graphic