The robust earnings season shifted investors’ focus away from geopolitics and back toward corporate fundamentals. However, the situation in Hormuz remains unresolved, and investor patience is starting to wear thin.

- The US blockade was arguably a strategic move, helping to ease concerns over further damage to regional energy infrastructure while limiting US military spending and equipment depletion. Meanwhile, Iran is facing mounting economic pressure and could soon struggle to finance itself if commodity exports are significantly curtailed.

- As a result, Trump appears to have gained a relatively stronger position vis-à-vis Iran, although domestically he remains under pressure amid declining approval ratings on economic management and the approach of the midterm elections.

The passage of time has so far worked in favour of the US position, with markets giving Trump some breathing room. However, crude oil prices have resumed their upward trajectory, while bond markets are increasingly coming under pressure.

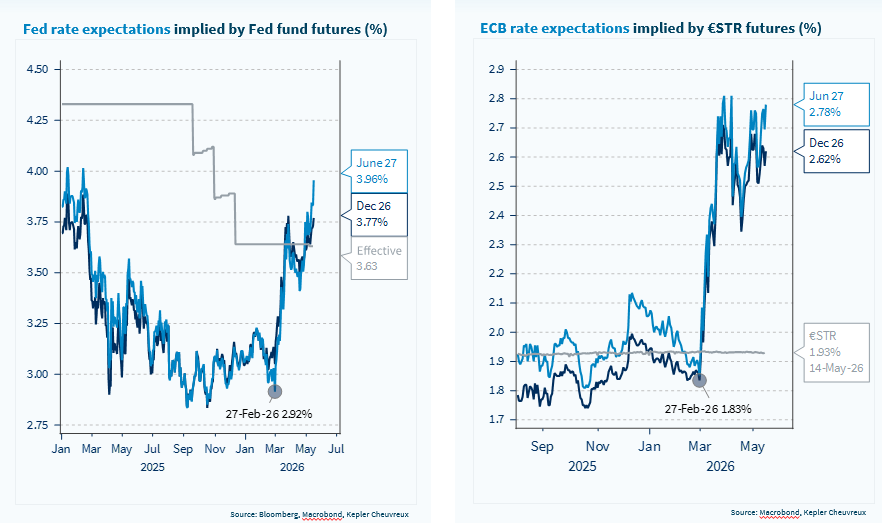

- Bond markets are coming under renewed selling pressure as inflation expectations continue to build, as we show in the report. April inflation data released last week in the US came in slightly above expectations, while persistently elevated energy prices are also increasing pressure on governments to introduce support measures aimed at easing household energy costs. However, market tolerance for unfunded fiscal expansion remains extremely limited at present.

- In the UK, Starmer is facing growing challenges within the Labour Party, adding market concerns that the next prime minister could pursue a more expansionary fiscal agenda.

Market developments illustrate the concerns we have been expressing for some time. From a portfolio construction perspective, bonds are currently not an effective hedge for equity exposure. To the extent that the main downside risk remains conflict escalation and rising inflation expectations, bonds are as risky as equities, though still less volatile. The main alternative to equities at present to de-risk portfolios is thus simply cash. Against this backdrop, we are implementing some adjustments to our asset allocation (see details in the report), that we see as tactical.

Going forward, the main upside risk is the possibility of an agreement between the US and Iran, which would likely drive oil prices sharply lower.

- Trump could also step back and agree to negotiate a nuclear deal at a future date. In that scenario, Hormuz would reopen, and both equity and bond markets would recover. Yet reaching that point may require additional pressure from financial markets.

- The downside risks are well known: renewed military strikes, energy shortages in Europe and Asia, and higher inflation and interest rates that could cause a recession. While we continue to believe that these downside scenarios are unlikely to fully materialise, the probability that markets begin pricing them in again has increased.

- Provided the current energy crisis does not persist for too long, we still expect the economic damage to remain limited and the inflation shock to prove temporary. However, over time, that assumption is becoming increasingly difficult to maintain.

In terms of investment themes that avoid making a direct bet on either conflict escalation or resolution: i) utilities offer an attractive AI ecosystem exposure through data-centre energy supply, while combining appealing valuations with relatively low volatility; ii) Telecommunications also remains a defensive allocation, given its limited exposure to energy costs, trade tensions and AI disruption; iii) Industrials are exposed to higher energy prices but benefit from pricing power, while capital goods should gain from the electrification trend driven by recurring energy shocks. Within industrials, defence has recently lost momentum, and we favour the space economy theme instead. Finally, both European sovereignty and the global nuclear revival remain highly relevant structural themes.

The European sovereignty theme received another boost last week, with EU legislators and governments agreeing on a Critical Medicines Act aimed at reducing persistent shortages of key drugs and lowering dependence on imports. Our EU sovereignty basket, for which we provide a performance update in this report, is built around the five pillars of the Draghi report, including secure healthcare and food supply, themes that are being further reinforced by this latest initiative.

The big beautiful rise in policy rate expectations