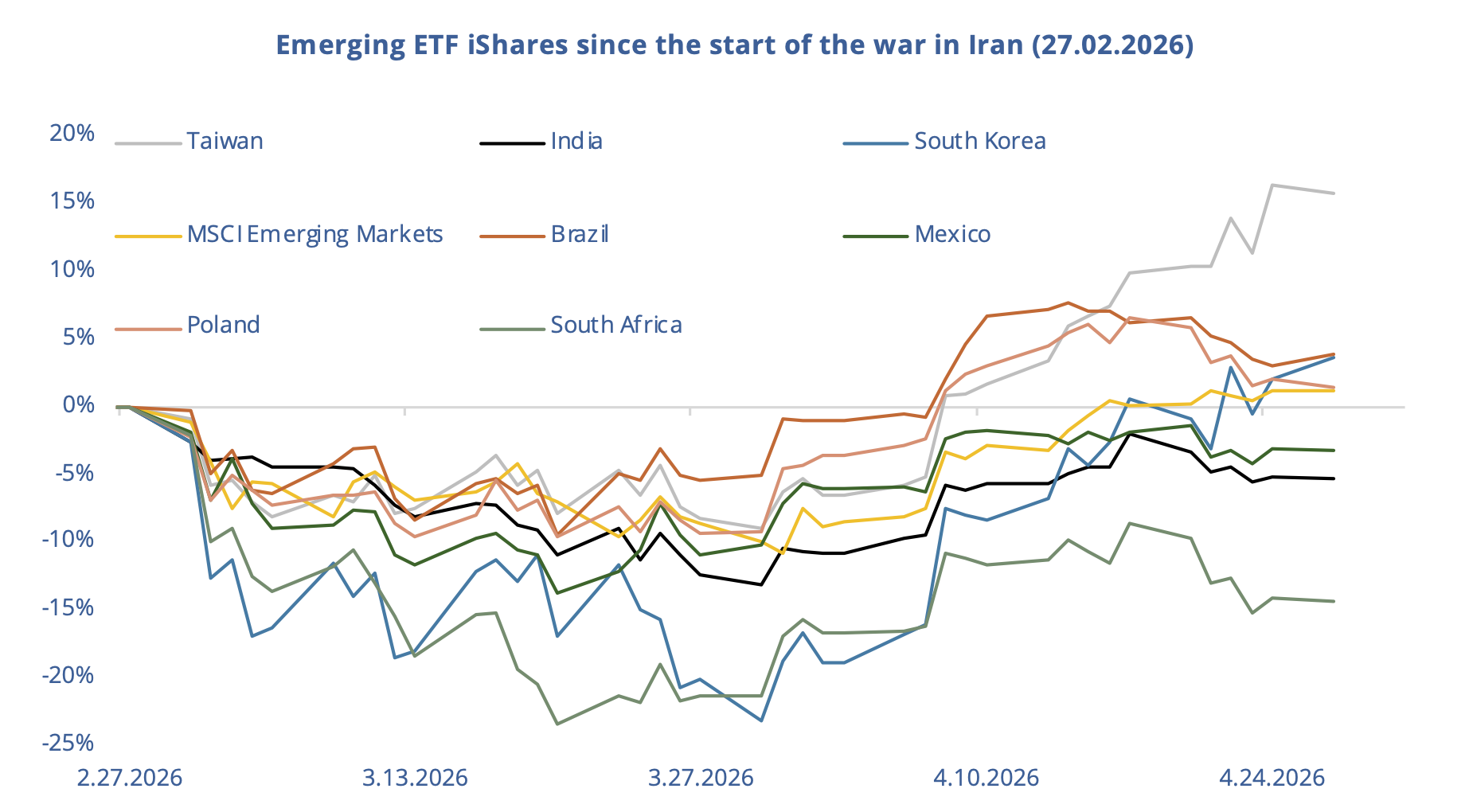

While the spectacular rebound in US equities has been the main focus of attention since the start of April (S&P 500: +12.4%), the rally has not been confined to the United States. Taken as a whole, emerging markets have also shifted back into high gear, more than erasing March’s air pocket (iShares MSCI EM: +14.9% in April, +1.9% since 27 February). Should we therefore conclude that the March correction was merely “noise”?

Let us first step back and look at the broader backdrop. The current environment is highly unusual. On the one hand, the energy crisis triggered by the war in Iran represents a significant risk for many net importers of oil, gas and agricultural commodities. On the other hand, the bright prospects for the artificial intelligence sector continue to excite investors more than ever. In other words, the tails of the distribution look exceptionally fat.

As a result, the rebound in emerging markets has been far from uniform. Performance over recent weeks has been overwhelmingly driven by regions at the heart of the AI boom. Since the start of April, the iShares MSCI South Korea ETF has resumed its parabolic trajectory: +25.6%! Its Taiwanese counterpart has also surged by +24.2%. These markets, whose fate is closely tied to that of the major US hyperscalers, are fully benefiting from the renewed enthusiasm for AI-related capex.

Other regions have also managed to stand out. Brazilian equities continue to advance (iShares MSCI Brazil: +4.0% MTD, +3.1% since 27 February). Brazil’s economy is far from the most vulnerable should the prospect of a double shock on oil and agricultural commodities materialize. The appreciation of the real speaks to this resilience: USD/BRL has now slipped below 5.0. Poland is also holding up well (iShares MSCI Poland: +12.0% MTD, +2.1% since 27 February). The presence of oil-related names such as Orlen in Polish indices is helping the country more than withstand the current environment, as the prospect of structurally higher oil prices grows stronger by the day.

But the strong headline performance of the emerging-market index also masks a number of underperformers. India (+7.5% MTD, -5.1% since 27 February) has managed to catch the April rebound, but the country’s growth outlook remains threatened by rising energy prices. On several occasions, the Reserve Bank of India has had to step in to support the rupee, which was at risk of breaking lower. South Africa (+4.6% MTD, -14.1% since 27 February) also suffered during the initial phase of the conflict. While the country’s economic activity is naturally exposed to an energy crisis, the decline in gold — which dragged gold miners lower — has been the main driver of the correction in the local equity index. That said, the stabilization of gold prices in recent days supports our view that the collapse in gold was primarily the result of investor panic between early and mid-March. We therefore remain constructive on both the metal and the region.