A relief rally. Following the ceasefire agreed by Iran, Israel and the US on 7 April, markets have staged a sharp rebound across equities, bonds, gold and, more broadly, all assets that had been heavily sold in recent weeks. While this reaction is understandable, as the agreement signals de-escalation, difficult negotiations still lie ahead, particularly regarding the status of the Strait of Hormuz.

- Latest reports suggest that Iran seeks to assert control over the area and impose a toll for safe passage. In our view, it is highly unlikely that the US, Europe and Gulf states would accept such terms. It is equally doubtful that major Asian importers, i.e. China, India, Japan and Korea, would agree, given their reliance on oil and LNG flows through the Strait. Ongoing fighting at the time of writing also threatens to derail the fragile US-Iran ceasefire.

- While we expect further de-escalation, the process is likely to be gradual and uneven. However, Trump clearly seeks an off‑ramp, which remains a positive factor for risk assets.

The marginal factor. The ceasefire announced yesterday appears more as a political off-ramp for President Trump than a durable resolution. It remains unclear whether Iran is willing to soften its demands, although any sign of compromise would likely push oil prices lower. Assessing the Iranian leadership’s willingness to reach an agreement is particularly challenging, especially as the killing of senior policymakers may have led to a more hardline stance.

- Given current correlation patterns, it is relatively straightforward to identify the beneficiaries of a détente (European and Asian equities, consumer sectors and banks in equities, high-yield credit and long duration in bonds) versus those that would benefit from renewed tensions (energy, the US dollar and inflation-linked bonds). The direction of travel, however, remains unresolved and depends ultimately on risk appetite and confidence that all parties share an interest in reaching a resolution.

- We show in the report a correlation analysis for European equity sectors and find that since the beginning of the conflict, banks appear to be the most negatively correlated to oil prices. They should benefit the most from further de-escalation.

No imminent rate hikes. Recent price action has highlighted how quickly oil prices can adjust lower. Since 31 March, Brent crude has fallen by around 20%. While current levels (around $95/b) already price in some degree of de-escalation, further concrete steps will be required to anchor expectations of a lasting resolution, consistent, in our view, with Brent in the $80–85/b range. This remains our baseline scenario by the end of Q2 2026.

- One key implication is that, absent a renewed escalation, the ECB is likely to remain on hold at its 30 April meeting, retaining flexibility to reassess conditions ahead of the 11 June monetary policy meeting.

The near term and the longer term. Provided oil prices ease towards $80–85/b by the end of Q2, as we expect, the impact on growth and inflation in both the US and Europe should remain limited. Equity valuations are not cheap, but they are still below the levels observed at the end of February.

- Meanwhile, as the Q1 2026 earnings season is about to start, FactSet highlights the highest number of S&P 500 companies issuing positive EPS guidance in five years. For Q1 2026, the estimated earnings growth rate for the S&P 500 stands at 13.2% (vs. 12.8% expected in early January). If realised, this would mark the sixth consecutive quarter of double-digit earnings growth, supporting our overweight stance on US equities, which offer some diversification against the binary outcomes of ongoing conflict negotiations.

- Finally, longer-term equity themes, such as European sovereignty, global nuclear energy and defence, which we have discussed in recent reports, remain highly attractive in our view.

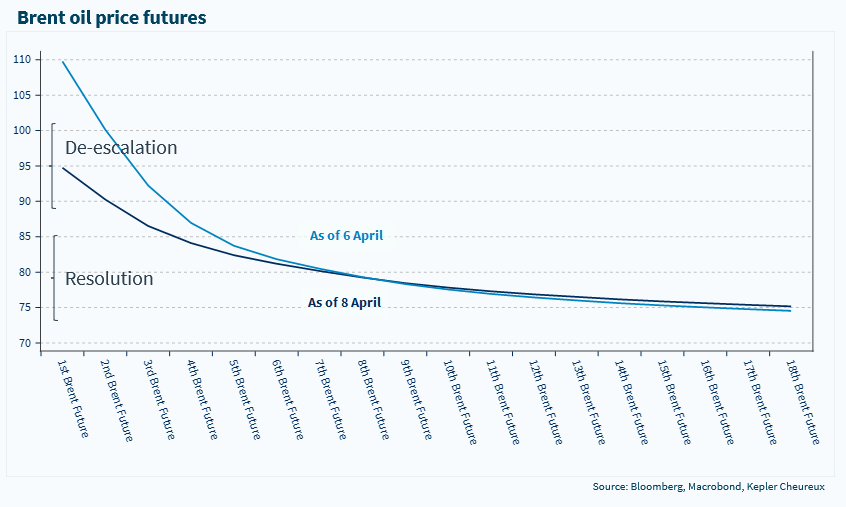

Oil prices remain the key barometer of expectations about de-escalation and resolution