Albeit with some initial hiccups, the ceasefire in the Middle East is holding, and peace negotiations are ongoing. This has been reassuring for markets: both equities and bonds have rebounded in recent days, reinforcing our Overweight stance on risky assets.

- Despite the fact that the Strait of Hormuz stays closed, spot oil prices have moved into the middle of our de‑escalation range ($90–100/b) and could gradually drift toward the resolution range ($75–85/b), although this process may take time.

- An optimistic scenario (that is, bearish for oil and interest rates, and bullish for equities) would be a full normalisation of relations between Iran and Western countries, which is currently being discussed as part of the peace negotiations. A complete lifting of sanctions would allow substantial investments to be deployed to revive oil and gas production. The U.S. EIA estimates that crude oil production could increase rapidly by around 20% (from 3.2 mb/d currently to 3.8 mb/d) within a 12‑month horizon, and by 40–50% over a 3–5 year horizon (to 4.5–5.0 mb/d). This scenario would clearly represent a positive outcome to the conflict, rather than a return to the pre‑conflict status quo. The probability of such a scenario has increased in recent days.

That said, while equities are rapidly approaching recent highs, the conflict is leaving more persistent scars on euro rates amid concerns about a potentially more hawkish ECB. As shown in this report, the current energy shock is indeed comparable in magnitude to the 2022 spike following Russia’s invasion of Ukraine.

- However, initial conditions differ materially. Unlike in 2022, the post‑COVID inflation shock is no longer present, and the starting point for policy rates is very different: highly accommodative then, broadly neutral today.

- Moreover, we estimate that CPI energy inflation in both the euro area and the US is more sensitive to the long end of the Brent curve (around 18 months) than to spot prices. This is reassuring, as the long end remains well anchored near $75/b.

- Taken together, these factors suggest that central banks are unlikely to engage in frenetic rate hikes, particularly in the US, where employment dynamics are weakening.

On equities, the Q1‑2026 earnings season has started, with expectations running high in the US: consensus points to 12.6% year‑on‑year EPS growth for the S&P 500, and an impressive +45% for the Information Technology sector. While the US consumer will have to deal with the impact of both higher tariffs and oil prices, European consumer faces an additional headwind from higher interest rates persisting for longer. As a result, consumer‑oriented equity themes may remain under pressure even in a full conflict‑resolution scenario.

Concurrently, correlations with Brent oil prices indicate that European banks stand to benefit the most from lower oil prices. Although the sector is no longer “value” relative to its own history, it continues to trade at a discount versus other sectors and still offers attractive shareholder remuneration through dividends and buybacks.

Finally, in line with our recent investment case on electrification, we upgrade European Industrials to Neutral (from Underweight) and marginally downgrade Healthcare from Strong Overweight to Overweight.

- Industrials are no longer cheap, particularly in Aerospace & Defense and electrical equipment. However, a new paradigm has emerged in the wake of recurrent energy shocks: defense and energy independence are set to remain structural investment priorities. In our view, these themes will remain critical drivers of capital expenditure over the coming years, supporting the sector despite elevated valuations.

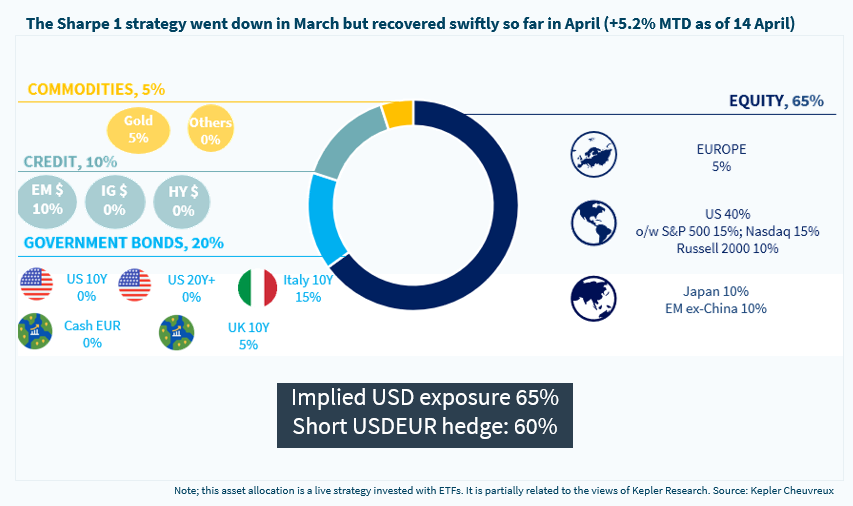

CHART OF THE WEEK | Asset allocation: Sharpe 1 multi-asset strategy