Dear reader, we will take a short break. Your weekly report will return in early May with fresh ideas to help position portfolios, hopefully in calmer waters.

Geopolitics keeps markets in check. Crude oil has remained volatile in recent sessions as the strategic chess game over control of the Strait of Hormuz continues. Late last week, initial hopes of a reopening of the maritime route quickly faded over the weekend, and supply disruptions could soon begin to weigh more meaningfully on economic activity. The ceasefire between the US and Iran still appears to be holding as we go to press, but it is set to expire on Wednesday. At the same time, a second round of bilateral talks between Israel and Lebanon will take place in Washington on Thursday. Once again, a busy and potentially market‑moving week lies ahead.

Somewhat paradoxically, against this backdrop of heightened geopolitical risk, risk assets remain in recovery mode. The speed of the equity market rebound has surprised many investors. In this weekly report, we explore the factors behind the growing gap between macro uncertainty and market performance and identify two main explanations.

- First, as highlighted in recent weeks, economic activity is influenced less by spot oil prices than by pricing at the long end of the futures curve. While volatility has surged at the front end, reflecting near‑term uncertainty, the long end of the Brent curve does not point to prolonged disruptions. Eighteen‑month Brent futures are trading around USD 75/bbl, a level that poses little headwind to growth. This raises the question of whether markets are being overly complacent, or whether they are instead pricing in normalization via a potential grand bargain, including sanctions removal and a rapid increase in Iranian oil flows in the not too distant future.

- Second, the key barometer of market sentiment, US equities, continues to be underpinned by a strong earnings outlook. Profits in Q1-2026 are on track to reach record levels, with double‑digit annual growth expected for the sixth consecutive quarter. From this perspective, it is hardly surprising that the S&P 500 has returned to all‑time highs. Financials got off to a strong start last week, while the information technology sector is expected to deliver close to 45% EPS growth in Q1 2026.

How to position portfolios. We turned outright Overweight equities in early April, based on the view that the asset class would benefit the most, in relative to bonds, from an environment of modest inflation and resilient growth under a short‑lived conflict scenario. So far, consensus economic forecasts have not been materially revised lower. That said, the longer oil disruptions persist, the more damaging they become for household confidence, private consumption and, ultimately, profit expectations. Europe still appears most at risk from this perspective.

- For now, we continue to believe that all parties have an incentive to pursue negotiations. However, following the sharp April market rebound, the risk‑reward of this tactical equity trade has diminished. At the same time, we see limited appeal in bonds as an effective hedge against a conflict‑escalation scenario.

- Our positioning, therefore, remains implicitly short oil. Within equities, we stay Overweight Japan and EM Asia, while in fixed income, we favour Italian BTPs. Within commodities, we retain some exposure to gold as a hedge against geopolitical and macro uncertainty.

- Within European equities, consumer‑related themes and real estate remain speculative in our view. Instead, we are more comfortable with banks, metals and mining, which offer a more effective way to position portfolios for higher near‑term inflation while preserving exposure to growth resilience.

CHART OF THE WEEK

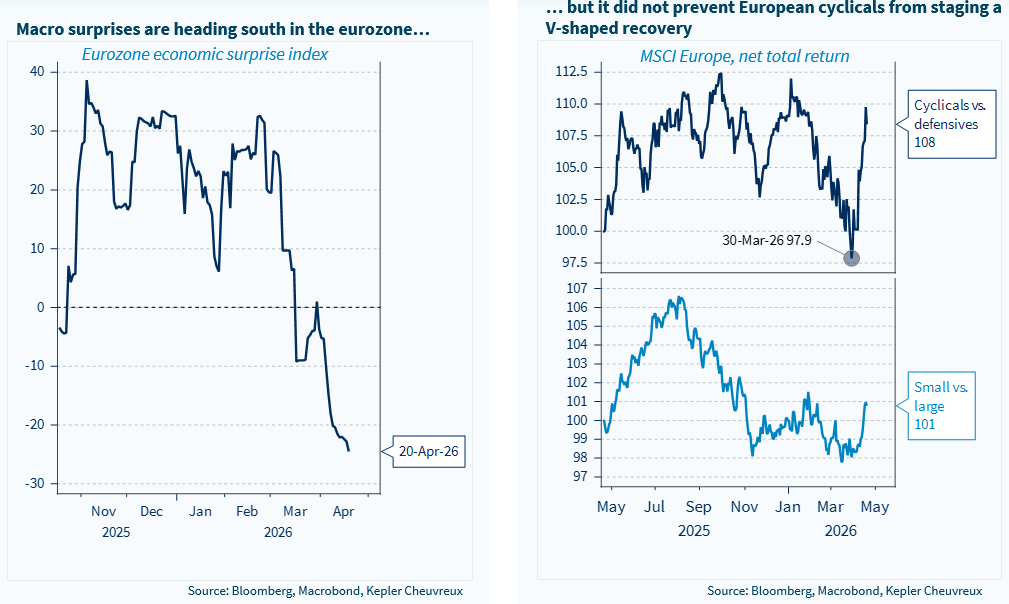

Europe sends mixed signals as growth momentum eases, yet cyclical stocks rebound sharply