Some weeks ago, we released the first episode of this series in which we expressed our bullish stance on bonds.

Since then, we had to put this view on mute temporarily, to take tactical positions on the spectacular equity market rebound that took place last month.

- But with mounting evidence that inflation is converging fast to central bank targets, the Fed/ ECB stance is likely to switch from hawkish to neutral pretty soon. In this context, we put renewed emphasis this week on the historical opportunity that lies ahead on this asset class.

Most recent macro developments are very supportive:

- The euro area CPI released last week (for November) was below consensus expectations, at 2.4% year-over-year (from 2.9% in October). This is the second month in a row that inflation falls below 3%. Although this is a preliminary release without all the details, every sub-component (food, energy, goods and services) decelerated.

- The OPEC+ meeting saw Saudi Arabia extending the voluntary 1mb/d oil supply cut until end Q1-2024, as expected (see OPEC meeting wrap-up). This was largely priced in and no market impact. Meanwhile, the lack of compliance from other OPEC+ members (UAE, Iraq, Russia) and rising supplies from the US / Iran continued to drag oil prices lower, a tailwind for disinflation and by extension for bonds.

- In the US, Christopher Waller, one of the most hawkish and influential FOMC members, opened the door to a pause or even a cut if inflation continues to slow. These are the first signs of an upcoming Fed pivot. The ECB is still behind the curve on that front, but with inflation below 2.5% in November, and growth decelerating sharply, we believe the members of the governing council will have to update their hawkish software pretty soon as well.

With markets already pricing in aggressive rate cuts in 2024 (more than 100 bps for both the Fed and the ECB as we go to press), there could nonetheless be some pushback from central banks in the coming weeks. This would be, in our view, a very good entry point to increased bond duration in portfolios and/ or to play curve steepeners.

- The key milestones ahead are the December 13th &14th Fed/ ECB monetary policy meetings, respectively. The release of their updated forecasts for growth and inflation as well as the Fed “dot plot” will be key to guide market expectations. They have no reason for them to maintain the hawkish bias, but they could keep the stance on hold until early 2024, arguing that the inflation outlook remains uncertain.

A focus on European credit markets. We have been positive on credit for some time, especially on investment grade (IG) credit. Although spreads were unchanged in recent months, and even tightened for financials, our views were challenged by market conditions. The rise in interest rates was a headwind for credit in total return terms, but conditions have now markedly improved. We stay Overweight IG and recommend selectivity in High Yield. The wall of debt has been pushed out until 2025-2026, but borrowing costs will continue to rise for lowest rated issuers.

Finally, we provide our monthly update on flows and positioning. The key takeaway is that long positions on the Nasdaq hit 5-year highs. Although we are not particularly bearish on a 6-12 months' timeframe, the stretched positioning comforts our recent decision to reduce equities in our asset allocation.

Week ahead:

- The November US job market report will be a key milestone for the bond market outlook. Signs of additional softening in labour market tightness (i.e. net job creation below 150k and/ or unemployment rate at/ above 4%) would contribute to drag yields lower. The ISM services and the University of Michigan consumer sentiment survey for December can also have market implications.

- In the euro area, producer prices and retail sales are likely to continue to show weakness economic activity.

- In China, the services PMI and trade data will contribute to clarify the picture on growth conditions.

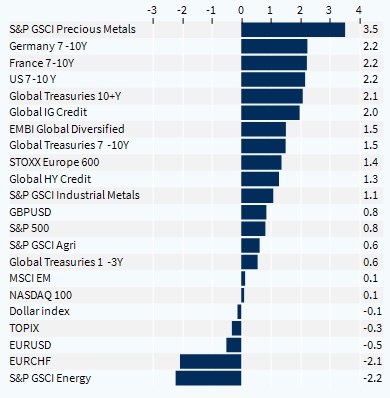

Asset classes performance (1 week)