In recent weeks, fast-changing market conditions have proved challenging for investors’ nerves, though the major equity indices remain positively oriented. Investors have had to digest the rise and fall in oil prices according to the geopolitical newsflow, the renewed rise in bond yields on the back of robust macro releases in the US, and Trump’s momentum in polls (we provide an update on both topics in the report). And then, China continues to generate stimulus expectations while providing sparse details, which led markets to express second thoughts last week. We shared our views about China less than a month ago, when we doubled our exposure to EM Asia equities to 10% as we were giving China’s stimulus efforts a chance, with some caution due to past disappointments.

We continue to believe that Chinese policymakers’ abrupt policy pivot in late September sent a strong signal that their pain threshold had been reached. The shift in stance came after the Fed started to cut rates (leaving more room for the PBoC to ease), but it was also likely driven by growing concerns over social stability stemming from the economic slowdown, in particular rising youth unemployment and fiscal problems among local governments.

However, the stimulus efforts have so far failed to decisively convince markets they could spur a sustained recovery, as they have fallen short on fiscal support. Achieving the 5% GDP growth target seems within reach with the new measures announced, but policymakers appear reluctant to take bolder steps at this stage, probably as external demand remains resilient (manufacturing/exports). They are also likely holding off until the US elections to decide whether further measures to boost domestic demand are needed, should trade tensions escalate (Trump).

In this week’s report, we explore the link between Chinese equities and European equities. We find, without much surprise, that Metals & Mining, Semiconductors, Consumer Durables & Apparel (read: Luxury), as well as Automobiles, are the sectors that have the highest beta relative to the Chinese equity markets (proxied by the MSCI China). Retailing also appears to be sensitive, but this is mainly due to one stock, Prosus, which has a 25% stake in Tencent. Conversely, Telcos, Food Retailing and Utilities are the most negatively correlated to China (domestic sectors). We also explore the sensitivity of individual European stocks to China following the same methodology. In the Metals & Mining sector: Anglo American, Rio Tinto, and Antofagasta are the most correlated. In Consumer Durables & Apparel, Swatch Group, Richemont and Adidas appear to be the most strongly linked to China’s equity market. Then, within Financials, Prudential is the most sensitive on the back of its stakes in several insurance companies in China.

In our European equity sector allocation, we adopt a selective approach to the Chinese stimulus efforts:

- We upgraded Metals & Mining to Strong OW on 30 September, as China’s policies tend to directly drive demand for industrial metals through infrastructure projects and investment, giving the sector a clearer boost.

- Semiconductors (upgraded to OW on 23 September) are also exposed to China, notably ASML (China = c. 20% of revenues in 2025).

- On the other hand, we remain more cautious on Consumer Discretionary sectors exposed to China, as the improvement in consumer confidence will probably take more time to materialise and we see other issues as well.

- Autos (reiterate UW). The fundamental problems (margins under pressure) are being compounded by the collapse in European car makers’ market shares in China and the trade conflict.

- Luxury goods (reiterate N): Luxury companies still have pretty significant challenges beyond China (they raised prices too much) and they remain at risk of an escalation in the EU-China trade spat.

Week ahead: the macro agenda will be relatively light with business surveys such as the preliminary PMI in developed countries and the IFO survey in Germany being the key highlights. On the corporate earnings front, 113 companies listed in the S&P 500 will report earnings next week, of which Lockheed Martin, RTX, Northrop Gruman, General Motors, Tesla, UPS, Boeing, Verizon, T-Mobile, AT&T, Centene, IBM. In Europe, the earnings season will kick into higher gear, with 94 companies listed in the Stoxx Europe 600 due to report quarterly earnings, of which SAP, SAAB, Mercedes Benz, Volvo Cars, DNB Bank, Swedbank, Deutsche Bank, Lloyds Bank, Barclays, Sodexo, Iberdrola, Heineken, ENI, Sanofi, Electrolux, Orange.

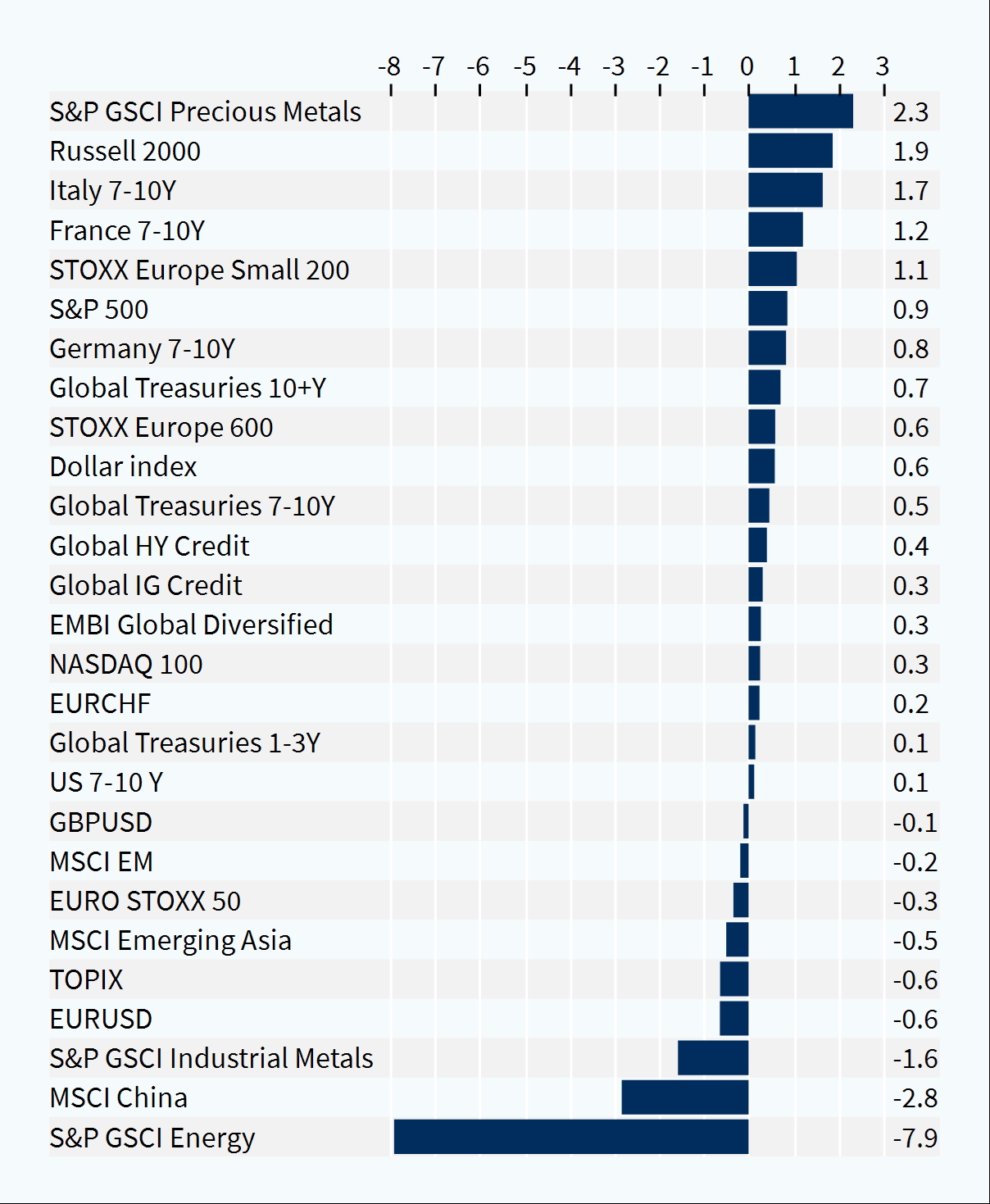

Cross-asset performance (last week, %)