The U.S. and Iran have reportedly agreed to extend the ceasefire and reopen the Strait of Hormuz, another in a long series of “almost-there” deals (more than 38, according to CNN). As before, key issues appear to have been deferred. What looks more convincing is the political will to de-escalate, with Trump keen to exit the conflict, and commodity markets not pricing a renewed flare-up. Against this backdrop, Brent has fallen below $85/b for the first time since the conflict began and is now drifting towards $80/b.

In this report, we assess the forthcoming market implications, focusing on inflation and rate expectations, as well as a potential broadening of equity market performance beyond Tech. On inflation and rates, the euro area presents greater downside than the U.S., where growth remains stronger and tariff-related pressures persist. That said, the ECB raised interest rates last week, and a policy pivot is unlikely to take time before September, in our view. We see scope for 2-year EUR swap rates to move back toward 2.5% by year-end, from 2.2% prior to the start of the conflict and around 2.8% currently. We also expect gold to benefit from declining inflation and rate expectations.

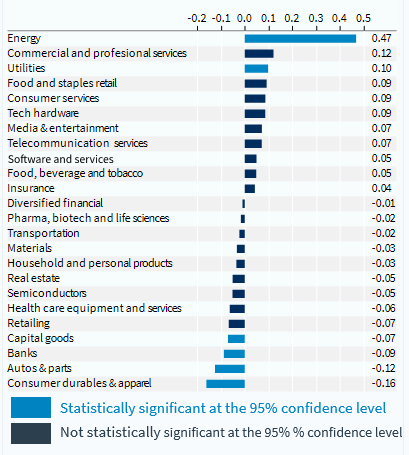

European equity implications from lower oil prices. European equities have been the most negatively correlated to oil prices. In the report, we show that consumer discretionary and banks in Europe are likely winners from falling oil prices. Some segments of industrials (capital goods and airlines) and materials (metals & mining) should also perform better, while real estate may benefit the most from lower rate expectations. Consumer durables (i.e. luxury) stand to benefit from both lower energy prices and interest rates through better household purchasing power. But demand remains speculative at this stage and selectivity remains important. Kering and Richemont are the most preferred by our equity analyst, while Hermes, LVMH, Moncler and Burberry are also rated Buy.

What could go wrong? Downside risks are easy to identify: failure to reach an agreement by mid-August (marking the end of the 60-day ceasefire extension), renewed escalation in Hormuz, a rebound in oil prices to $90–100/b, persistently high inflation, further rate hikes, and a pullback in consumer spending. That said, Trump may remain inclined to pursue compromises through the midterm elections to maximize the chances of retaining a majority, providing some near-term visibility. However, after the strong rally since late March, we maintain our asset allocation unchanged. Positioning was already geared toward conflict resolution, with an overweight in equities, particularly Asian markets (key energy importers). At our end-May rebalancing, we also extended bond duration and upgraded European equities, which we reiterate.

MSCI Europe sectors: beta versus Brent oil prices (based on weekly relative performance over 1-year)