We are relaunching our Key Calls series. This is a work in progress that will be updated and expanded.

#1: Stay OW equities on robust earnings growth and the Tech, infrastructure, and defence supercycle.

Global Tech delivered stellar returns in Q2. The key question heading into H2 2026 is whether this performance can be sustained. With Tech and the Magnificent 7 now trading on more reasonable valuations, thanks to exceptional earnings upgrades, the debate has shifted from valuation excess to earnings excess. We struggle with the notion of "excess earnings" (some are even referring to an "earnings bubble").

Upward EPS revisions provide support from a strategic standpoint but leave less room for upside surprises. We agree that there is limited room for disappointment as the Q2 earnings season starts. As a result, we look for diversifiers in our recommendations, as assets that rise sharply become more volatile.

#2: There is room for a broadening of equity performance beyond Tech: Europe, US small caps.

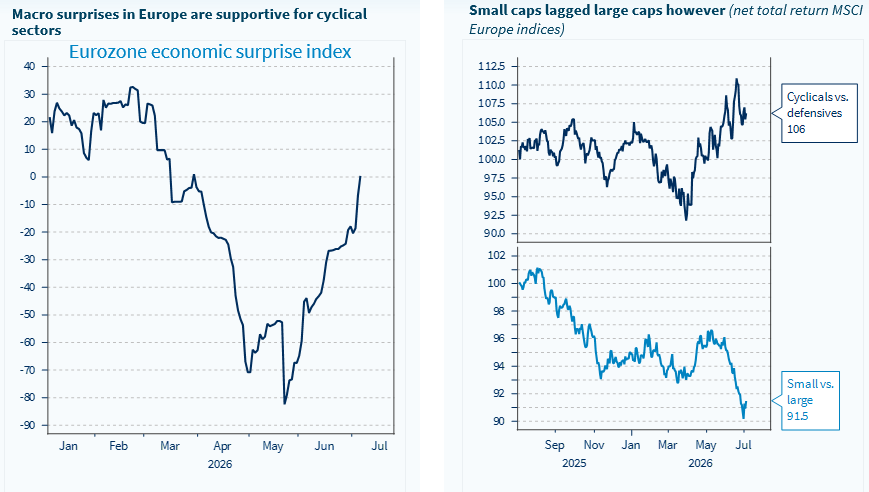

We upgraded Euro area equities at the end of May, supported by a combination of macro tailwinds: lower energy prices, an ECB that is less hawkish than commonly perceived, and Germany's renewed policy push to accelerate growth.

US small caps have started to rerate, and we believe they offer several benefits. They offer diversification versus Tech as US small caps have a bias towards industrials. The sovereignty/ reshoring push in terms of capital allocation by the authorities should also prove supportive for small caps. They also trade at a discount versus the S&P 500 & Nasdaq benchmarks.

#3: Low oil prices are here to stay: Energy-intensive industrials and the German stimulus basket.

Energy-intensive industrials are poised to benefit from the new energy landscape characterised by an oil glut that is likely to last. Within materials, metals & mining, and in particular, European steelmakers, should also benefit from it.

Germany aims at accelerating both the reform momentum and the implementation of the infrastructure package, a positive for industrials.

Our German Stimulus Basket, launched in March 2025, has returned to its previous highs. Since its inception, it has gained nearly 50%, compared with 18% for the STOXX Europe 600 and 12% for the DAX.

#4: Consumer stocks are poised to benefit from improving household purchasing power, but selectivity matters. Travel & Leisure is our preferred pick.

Lower energy prices are supporting consumers’ purchasing power, but the luxury and automotive sectors continue to face sector-specific demand challenges. Travel & Leisure is safer in our view and fits within the broader post-COVID trend that has supported spending on services and experiences rather than goods.

In Europe, excluding semiconductors that are enjoying the Tech boom, consumer services have been the best-performing sector since oil prices began their sharp decline at the end of April. Stay cautious on Autos and Neutral on Luxury.

#5: The bond carry offers attractive opportunities; the Fed may soon pivot away from its hawkish policy bias; favour high-carry sovereign issuers in Europe.

It remained tricky to deliver performance on fixed income during the first half of 2026 as inflation expectations jumped. In the near term, central banks may remain voluntarily behind the curve as inflation is still far from target.

Cooler job creation in the US in June opens the door for a softening in the Fed stance going forward. Watch next week's June US inflation release for signs of a potential "détente“ on rate expectations.

The new Fed Chair, Kevin Warsh, will need to establish his inflation-fighting credentials. As a result, the bar for adopting a more dovish stance is relatively high in the near term. However, we expect inflation to ease over June, July and August, making September an attractive entry point to extend duration in US Treasuries. Gold may then benefit from lower real interest rates in USD.

In our asset allocation, we continue to favour high-carry sovereign issuers in Europe, notably Italy and the UK, in the 7–10-year maturity segment.

CHART OF THE WEEK

Economic releases in the euro area have started to improve vs expectations; lower energy is a clear tailwind