We have been travelling over recent days and apologise for the irregular publication schedule of this weekly report. That said, client discussions often provide valuable inspiration. This edition, therefore, focuses on one of the market’s most debated themes: the apparent disconnect between the sharp rebound in equity markets and persistent geopolitical uncertainty, which could weigh on future economic activity and earnings growth.

Uncertainty is often assumed to be negative for both economic growth and corporate profits. However, that logic holds only all else being equal, which is clearly not the case today. The current energy shock is unfolding against the backdrop of a powerful AI‑driven capex boom, which is providing an important cushion.

From a macroeconomic perspective, recently released US GDP data illustrate a growing divergence between household consumption, which is weakening under the combined pressure of trade tariffs and higher energy prices, and non‑residential investment, which was the largest contributor to GDP growth in Q1. From a corporate earnings standpoint, US technology EPS grew by 51% in Q1‑2026, as shown in the report. This is more than sufficient to offset the headwinds stemming from higher energy prices, even as the consumer discretionary sector is also delivering earnings above expectations (even excluding Amazon).

In Europe, the picture is somewhat different. Recent data confirm the stagflationary flavour of the Iran shock, and there is no comparable capex boom to act as a buffer. That said, the Q1‑2026 European earnings season is also turning out better than expected, driven by positive surprises from energy and financials. Earnings growth in these sectors stands at 48% and 16%, respectively, well above expectations. Of the 46 financial companies that have reported so far in Europe (as of 7 May), 72% have beaten expectations.

Our take: there is indeed a disconnect between adverse newsflow and market performance. However, markets ultimately react to corporate profits and are designed to look through short‑term noise. Historically, geopolitical events tend to have a limited and short‑lived impact on markets, although this ultimately depends on how disruptive those events prove to be.

In the second part of this report, we analyse sensitivities to oil price fluctuations. We compute 50‑day correlations between equity markets and the 3‑month Brent futures contract, in order to avoid the excess volatility observed at the very front end of the Brent curve.

- We find that the Nikkei 225, Chinese equity benchmarks and the FTSE 100 are the least correlated equity markets to oil prices. In the UK, this low correlation is partly explained by the index’s significant exposure to energy stocks (around 11%). In China, the impact of energy price fluctuations has been cushioned by an aggressive build‑up of oil inventories over recent years. The low sensitivity of the Japanese equity market to oil prices came as a surprise to us, even after running the correlations with lags to account for time‑zone differences.

- On the other hand, we find that the EuroStoxx 50 is the equity benchmark most negatively correlated with oil prices. This is consistent with the region’s status as a major net energy importer and with the index’s bias towards cyclical sectors.

- Focusing next on European equity sectors, capital goods, banks and semiconductors emerge as the sectors most negatively correlated with oil price movements.

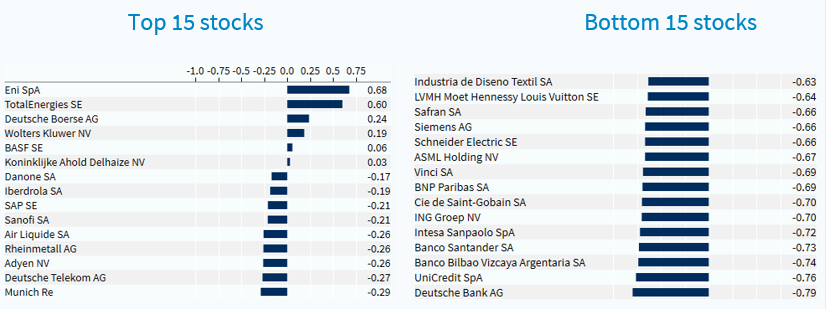

- At the single‑stock level within the EuroStoxx 50, Deutsche Bank (Hold), UniCredit (not rated), BBVA (Hold), Santander (Buy), Intesa Sanpaolo (Buy) and ING (Buy) show the strongest negative correlations with oil prices. By contrast, ENI (Hold) and TotalEnergies (Hold) are, unsurprisingly, the most positively correlated with oil prices. We also identify a group of stocks that are not significantly correlated with oil prices, including Deutsche Börse (Buy), BASF (Hold), Danone (Buy), Iberdrola (Buy), SAP (Buy), Sanofi (Hold), Air Liquide (Buy), Rheinmetall (Buy), Deutsche Telekom (Buy) and Munich Re (Buy).

So what?

Our analysis helps identify potential beneficiaries of conflict de‑escalation and declining oil prices, which underpins our implied multi-asset portfolio positioning, as detailed in the report. Meanwhile, stocks with limited sensitivity to oil prices may appeal to investors unwilling to take a strong, or speculative, view on the outcome of the conflict.

Euro Stoxx 50 : 50-day correlation (since conflict started) with 3-month Brent future