The future is now. Space exploration has inspired generations, and Elon Musk embodies that enduring sense of childlike wonder. In this spirit, the title of our report draws on Kubrick’s visionary sci‑fi epic, which, as early as 1968, projected us into the future through the sentient computer HAL 9000. In the age of AI, this nearly sixty‑year‑old film feels remarkably modern. We can only encourage younger generations to discover it.

The largest IPO ever - and money illusion. SpaceX is expected to go public next week, on 12 June 2026, with a target price of $135 per share and a potential valuation of $1.75 trillion. The company is expected to raise $75bn, more than twice the size of the previous largest IPO (Saudi Aramco raised $29.4bn in 2019, including the greenshoe option).

- These figures are staggering and naturally raise a key question: is this sensible? Is there excessive market exuberance for a loss-making company?

- Comparing nominal dollar amounts between Aramco’s 2019 IPO and SpaceX’s 2026 IPO is misleading. In relative terms, measured as a share of total equity market capitalization, SpaceX’s IPO looks far less exceptional. The expected $75bn issuance would represent around 0.09% of the current US equity market cap, broadly in line with Aramco’s IPO in 2019 and even lower than Alibaba’s IPO in 2014 (around 0.1%). Once the figures are normalised, the SpaceX IPO no longer appears as extraordinary as headline numbers suggest.

- This is a classic example of money illusion, a behavioural bias whereby individuals focus on nominal values rather than real or relative magnitudes. The bias is often amplified by media coverage emphasising eye-catching figures, which attract attention but can ultimately be misleading.

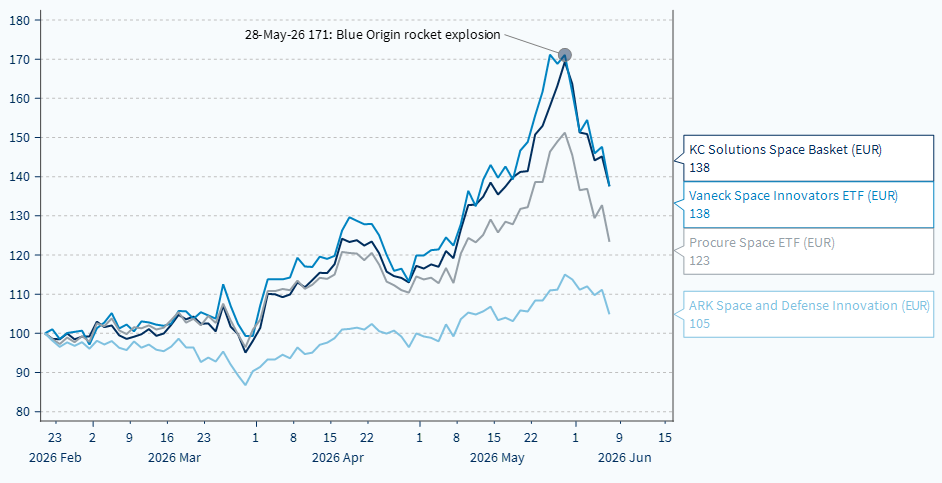

The space theme takes a breather. Ahead of the SpaceX IPO, space stocks have corrected sharply. We see four main reasons for this move:

- Profit-taking after strong performance: the theme delivered very strong gains earlier in the year, prompting investors to lock in profits;

- Inherent volatility: Since 2025, the space theme has experienced three drawdowns in excess of 20%. Each time, the rebound was swift, and we expect a similar pattern to unfold;

- An industrial risk trigger: the Blue Origin rocket explosion on 28 May served as a reminder that the space sector remains exposed to significant execution and technological risks.

- Sensitivity to interest rates: as a “growth” and richly valued segment, defence & space stocks are periodically vulnerable to rising rate expectations. The recent increase in yields has amplified the correction.

- Overall, we view the current drawdown as an opportunity for investors who were previously interested in the theme but deterred by stretched valuations.

A quick macro update. The May US job market report, released at the end of last week, came in significantly above consensus, with nonfarm payrolls rising by 172k versus expectations of 88k. The April figure was also revised up, from 115k to 179k. This stronger-than-expected data triggered a sharp rise in policy rate expectations and a rotation across equity sectors, with growth stocks typically more sensitive to higher interest rates.

- Chip stocks such as AMD, Intel, Broadcom and Qualcomm also came under pressure following Broadcom’s disappointing revenue outlook. Despite the negative market reaction, Broadcom delivered another strong quarter, beating expectations on both revenue and earnings and raising guidance for the current quarter. AI remains the core growth engine, with AI-related revenue reaching $10.8bn in F2Q26 and management guiding to $16bn in F3Q26, implying growth in excess of 200% year-on-year. However, the stock sold off as investors were positioned for an even stronger AI upside, a higher long-term revenue trajectory, and better visibility beyond 2027. Concerns around Google’s increasing insourcing efforts and intensifying competition in custom AI ASICs (Application-Specific Integrated Circuit, which are designed to accelerate artificial intelligence workloads such as neural network inference and training) also weighed on sentiment.

- Our take: what rises too quickly tends to become more volatile and is prone to corrections. In our view, a strong labour market report is not bad news, particularly as the US economy does not appear to be overheating (job creation was virtually absent in 2025). Meanwhile, inflation expectations have continued to decline in recent weeks, alongside falling oil prices. Overall, these developments could increase pressure on the Trump administration to reach a settlement with Iran to bring down oil prices and rate expectations.

- Get ready for an ECB rate hike next week. Inflation has accelerated further in May, at 3.2% in the euro area (from 3% in April) and the core CPI jumped to 2.5% (from 2.2% in April). However, the next steps are not written in stone and provided that oil prices stay close to $ 90/b or head towards 85 in the coming weeks, the ECB should stay put during the summer and revisit the subject for the September meeting.

The space theme experiences a pullback following a period of strong returns

Performance of the KC Solutions Space basket and comparable ETFs (rebased at launch on 22 February 2026)