Crude oil prices have experienced a sharp correction in recent weeks. The nearly 20% decline in May occurred amid a rising probability of an extension to the US–Iran ceasefire, which could allow negotiations to continue on key issues, including the Strait of Hormuz, nuclear activity, and the unfreezing of Iranian assets. Under the terms of the agreement, yet to be signed off on by Trump, the Strait of Hormuz is set to gradually reopen. Meanwhile, Bloomberg reported late last week that roughly a quarter of non-Iranian oil tankers previously stranded by the blockade have already exited the Persian Gulf. Front-month crude oil futures are now trading just above $90/b, down from $120/b a month ago.

In this report, we assess the implications of falling oil prices for rates and inflation expectations, and by extension for gold, which should paradoxically benefit from both easing geopolitical tensions through lower energy prices. Indeed, the three-month correlation between oil and gold prices stands at five-year lows, suggesting that gold could continue to appreciate if oil prices decline further, as we expect. We also show that silver and gold miners offer higher-beta exposure to the same theme. However, given that gold itself is inherently volatile, we remain cautious about leveraging this trade through miners or silver.

What about equities? Equity markets have delivered strong gains in recent months, supported by the AI supercycle and robust corporate earnings. We expect a short-term pause, as the extension of the ceasefire had been partially priced in. Nonetheless, lower energy prices are ultimately supportive for consumer spending, growth, and corporate profitability. Evidence of continued resilience in consumer demand would help reassure investors who have remained on the sidelines in recent weeks. ETF inflows into equities have been solid over the past month, yet anecdotal evidence suggests that investor positioning remains cautious, leaving room for additional inflows. Against this backdrop, we have recently shifted from a Neutral stance back to our long-standing Overweight position on equities, with a balanced allocation between the US and Europe (Neutral) and an Overweight on EM ex-China equities, Japanese equities, and EM sovereign credit.

Thematics: Defense, Space and Sovereignty. We examine the defense and space themes, which have diverged significantly in recent months. Defense equities declined by roughly 20% between late January and mid-May, somewhat surprising given the challenging geopolitical environment. By contrast, the space theme has significantly outperformed, rising by approximately 60% over the same period.

- Defense remains a volatile and heterogeneous sector but is currently recovering. We remain constructive, with a preference for global diversification across US, European and Asian names.

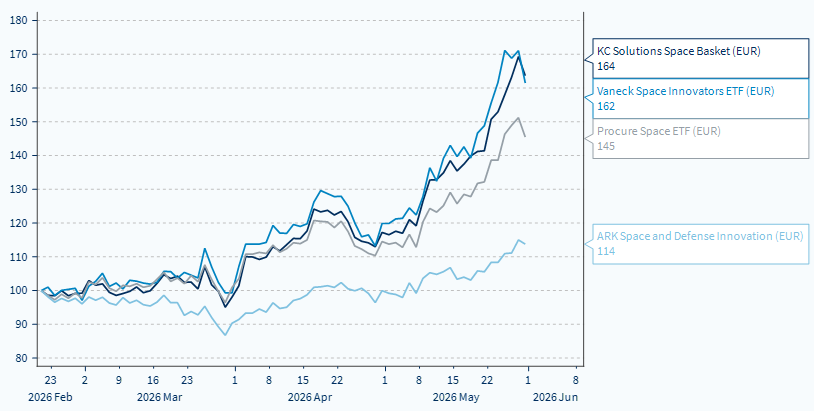

- The space theme is also inherently volatile, requiring investors to tolerate sharp price moves. In both sectors, our proprietary baskets have outperformed comparable ETFs.

- Is it too late to invest in the Space theme? This question mirrors earlier discussions on defense, which ultimately delivered exceptional returns. We believe the space theme has the potential to generate similarly strong performance. Traditional valuation metrics, particularly 12-month forward multiples, are largely irrelevant in this context, as markets are discounting earnings growth over a much longer horizon. Historical comparisons are therefore of limited use in what is potentially a new paradigm.

Space is entering a new phase of development, driven by three structural forces: defense, digitalization, and climate. Driven by technological innovation, declining launch costs, and rising demand for connectivity, security, and data, the “New Space Economy” is undergoing a profound transformation. The US remains the dominant player, accounting for 61% of global space budgets, but its lead is gradually narrowing as China’s share has risen from 2% in 2000 to 15% today. Europe, with only 10% of global spending, appears relatively behind, despite increasing strategic concerns around technological sovereignty.

- Space: a new defence/ sovereignty challenge. The war in Ukraine and broader geopolitical tensions have underscored the strategic importance of space infrastructure, now recognized as a fully operational military domain alongside land, sea, air, and cyber. Satellites are central to real-time intelligence, surveillance, missile detection, and secure communications. GPS systems have become indispensable for drones, autonomous vehicles, and precision military systems. This growing militarization is clearly reflected in public budgets, with defense-related space spending now exceeding civilian investment. Space is thus emerging as a key pillar of national sovereignty and critical infrastructure resilience.

- Space: an invisible infrastructure of global digitalization. Beyond military applications, the space economy has become a foundational pillar of the digital revolution. Satellites provide essential connectivity in remote, maritime, and aerial environments, while offering strategic redundancy in the event of terrestrial network failures or cyberattacks. They also support the development of the Internet of Things, intelligent supply chains, autonomous mobility, and smart cities. Space is equally central to the data economy. Satellites generate vast volumes of data used in artificial intelligence, meteorology, precision agriculture, and energy management. Looking ahead, the development of space-based cloud computing and in-orbit data processing could further accelerate this transformation.

- Climate as a catalyst for innovation. Space technologies have become indispensable tools for understanding and managing climate change. Satellites enable continuous monitoring of the Earth, including its most remote regions. They support the tracking of CO₂ emissions, ocean activity, and polar ice melt, while enhancing weather forecasting and early warning systems. The increasing precision of satellite data strengthens its role in natural disaster prevention and in shaping effective climate policies.

Performance of the KC Solutions Space basket and comparable ETFs (rebased at launch on 22 February 2026)