The Fed initiated its rate cut cycle with a bang and we explore in this report the broader market implications. Last week, Jay Powell adeptly managed a very difficult communication exercise. Going big, i.e. cutting rates by 50 bps, carried the risk of signalling the US economy is in a weaker state than what markets think. But Jerome Powell had a good pitch: the economy is in good shape, but the central bank intends to keep it that way. Going big implicitly sent the message that the Fed is strongly committed towards supporting growth. The ECB should take notice. Of course, the other message is that the war on inflation is most likely won, as we expect too.

After the big repricing in rate expectations that occurred in recent weeks in the US, there was a risk that the pricing could be excessive. Yet, post-Fed meeting, we show in the report that markets still anticipate that the Fed will go a bit faster than what the “dot plot” suggests. This makes sense in our view. We know the Fed will not stay behind the curve and, in parallel, the bleak picture on energy commodities, due to excess supply in 25 and 26, suggests that inflationary pressures will continue to ease. In this context, we have increased the duration of our bond portfolio and find value in curve steepeners.

The Fed put is back. We show in the report that in the absence of a recession, equity markets keep rallying when the monetary easing cycle starts. And when we look at the current state of the US economy, there is no sign of deceleration in consumer spending that suggests a recession is around the corner. Lower energy prices and lower interest rates will actually improve households’ purchasing power. Within the economy though, some companies report that some consumers have been squeezed by inflation. That is precisely why inflation rates are falling as companies implicitly give purchasing power back to consumers. The same goes for corporates’ behaviour: many have reduced their inventories and have postponed new capex or prioritise their IT spending cautiously. These are the parts of the economy that could improve as policy rates are gradually eased, along with residential construction. Meanwhile Powell’s big move probably helps the rest of the world. China and EM are indeed in a better position to cut rates more aggressively, while the dollar depreciation should prove supportive for EM sovereign credit-worthiness, that we have at Overweight in our asset allocation. US elections remain nonetheless a critical milestone that can still bring surprises. As US equity markets are richly valued, some caution is still required.

European equities: upgrade Semis (OW) vs Software (UW). Powell’s move is thus a pre-condition to start revisiting some beaten down cyclical sectors. We don’t think it’s time to go “all-in” on cyclicals and, just as fixed income is expected to continue to offer a decent return, many European bond proxies should continue to perform well. We nonetheless want to seize the opportunity on Semis. They underperformed lately and the delays in deploying capex also limit the risk of over supplies. The case of ASML is important for the European sector and the news flow has been sour lately with Intel delays. It gives us an entry point on a European jewel. In front of that, we downgrade European Software because the weight of SAP has made this sector a pure “secure growth” proxy. The truly cyclical software and services companies might be better treated by the market as long as they have underperformed and offer a decent risk reward.

Week ahead: preliminary PMIs will be available in large countries. In the US, consumer confidence and monthly figures on personal income and spending will be available, as well as the PCE deflator, the Fed’s preferred measure of inflation. In Germany, the IFO business survey will be released for the ongoing month.

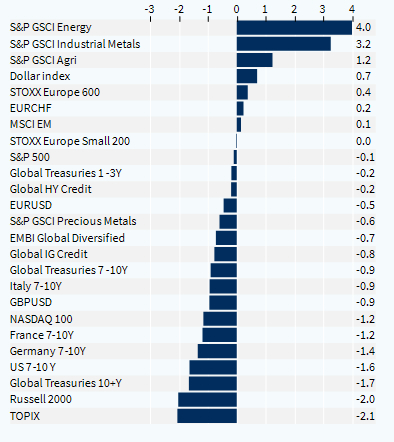

Cross-asset performance (last week, %)