As September 2024 ends, it could be remembered as a turning point for China’s longest deflationary streak since 1999. Last week we explained in our weekly that the “Fed going big” offered the optionality to the rest of the world to follow suit in terms of monetary policy easing. In recent days, we got confirmation that there is willingness to do that on the Chinese front.

The ECB could also accelerate the pace of rate cuts mid-October, if core inflation data this week confirms disinflation is on track. French and Spanish numbers released last Friday gave a good indication that inflation kept falling in September. It is all the more relevant for the eurozone that the labour market is showing signs of fragility. Yield curve normalization (10-2 years or 30-2 years in euros) is an appealing avenue to play that theme, in our view.

What we think will likely happen next in China is potentially an improvement in consumer confidence if the incentives work. In effect, the measures announced so far aim at improving households’ purchasing power on the one hand (interest rate cuts), and improving market functioning on the other (re-lending, refinancing facilities). In recent years, similar measures faded rapidly. Households might well save this extra cash, while they extent of the support package still look small compared to the size of the housing oversupply problem. But it could be the beginning of the end of the deflationary streak, and there is the optionality that the authorities now turn more aggressive on the fiscal side.

It will take time to restore consumer confidence, but markets are impatient. Drawing the parallel with the US housing crisis of the last decade, it took seven years for US consumer confidence to return to the 2007 level. Yet, the market initiated its historical rebound much before, as early as March 2009! Hence, we give it a chance in our asset allocation, with a 10% weighting to a broad and diversified EM Asia index that involves a moderate exposure to Chinese equities. We see that as rather tactical for the time being, but ambitious fiscal announcements could lead us to turn positive on China for the longer run.

We have also in mind that China has another major issue. It will have to reduce its manufacturing ambitions, manage a yuan appreciation, or face a global trade war. A Trump victory in the US election would bring this issue to the forefront. The EU is also negotiating with China to raise trade barriers, as we speak. And in the past, China has never managed to rebalance its economy from exports and capex (infrastructure, real estate) to domestic consumption.

Within European sectors that have historically been sensitive to China:

- We reiterate: Luxury (N), Autos (UW), and Chemicals (OW). The world of 2024 has moved on from the world of 2016. German Autos are gradually losing their Chinese golden goose, and the Luxury sector probably needs more time to digest the disinflation wave.

- But we upgrade Basic Resources (from OW to Strong OW).

On the other hand, in our European equity allocation framework, we revisit two small sectors:

- European Consumer Services (Travel & Leisure from UW to OW): the fall in the oil price is a double positive: it makes the cost of travel cheaper and inflates consumer purchasing power. Falling rates should also help in countries with variable-rate mortgages.

- Construction Materials (from UW to OW): volumes should gradually pick up as the rate cut cycle filters through to the economy. Residential construction markets in particular should pick up.

Conversely, we downgrade the Oil & Gas sector further, from Neutral to UW. The sector has performed poorly and is relatively cheap. But cheap can get cheaper if the oil price truly re-adjusts to a new equilibrium, slowing down capex and supply.

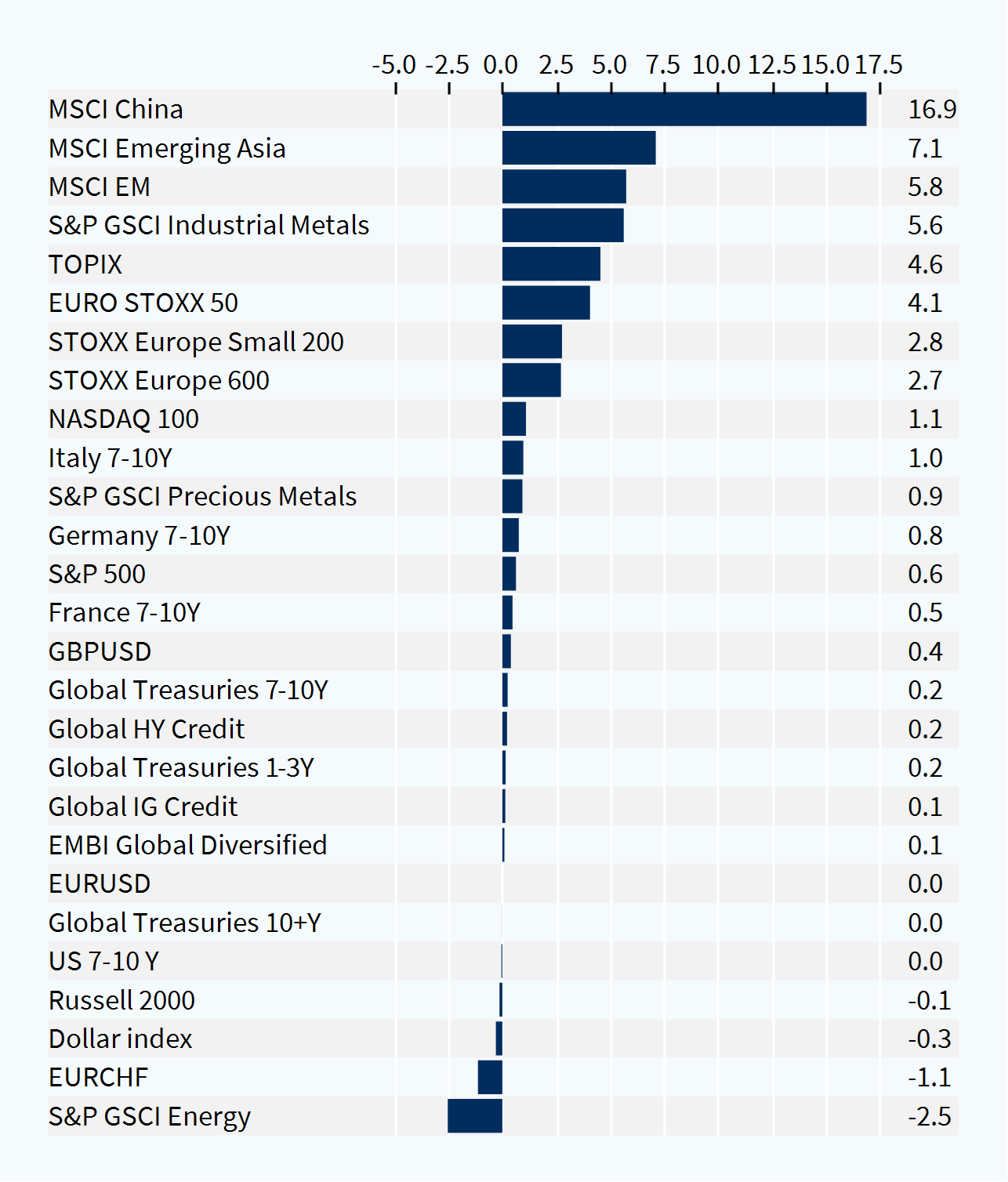

Cross-asset performance (last week, %)