Recent weeks have seen a significant repricing of Fed rate cut expectations. Until recently, expectations were tilted towards the likelihood of a soft landing, while the news flow actually brought better economic data in the US, the beginning of a reversal in policy stance from China, a sharp rebound in the oil price, and a slight rebalancing of election odds with a Trump comeback. This translated into a stronger dollar and flattish markets with significant sector rotation activity.

- Rate cut expectations are now broadly aligned with the Fed’s dot plot, implying that some inflationary pressures would have to pop in order to affect the Fed’s dot plot. This could occur should the worst-case scenario in the Middle East materialise or should China suddenly deploy a jumbo stimulus programme. Both risks are unlikely, in our view. Should the Fed do what it says it will do, the US 10Y yield should head towards 3-3.40% by the end of 2025, meaning that bonds are once again starting to be attractive at current levels.

The US election uncertainty comes into the equation though: Trump’s agenda could prove inflationary and push bond yields higher with a loose fiscal stance (see here for a fiscal assessment of the respective candidates). The outcome is now too close to call with extremely tight polls. While Harris is slightly ahead in national polls, state-level polls suggest a small margin of victory for Trump. Pennsylvania will be a key battleground state, hence the title of this report.

- We believe that whoever wins, there will be a distinction between what candidates promised and what they will actually do. Part of the answer to this gap (promises and realities) will lie in the results for the Congress itself. A divided government (which is very likely) would be the best case for bonds and the chance of aggressive rate cuts. Indeed, in that scenario, the Congress would not support any aggressive fiscal proposals from the new president.

- In the case of foreign policy, the views of both candidates are actually converging, even on Ukraine, where there is fatigue in both camps. The only notable difference is on the tariffs policy and the transactional nature of Trump versus Harris. Trump will be keener to strike deals. Deploying the “MAGA” agenda will clearly encourage investors to increase their OW in US stocks even further, as they stand to lose less from global trade woes. We could also see a switch out of bonds into equities. However, we believe that it will have to be seen whether China and Europe call his bluff and negotiate better trade deals. A Harris win, on the other hand, would give investors a pretext to diversify to the RoW with a weaker dollar and lower rates.

The earnings season will bring top-down considerations too, but expectations have come down recently. With no disasters apparent in the macro data, we think the earnings season will prove pretty neutral at a top-down level, or even contribute to some relief if companies managed to play their usual “guide low, deliver high” game.

- 2024 earnings expectations have been cut pretty significantly in Europe and in the US if you exclude the contribution of Big Techs. Of course, they shouldn’t be excluded, but it makes sense to look at it that way for comparison purposes. Indeed, the US equity market excluding Big Tech is pretty similar to the European market, but with a very different geographic mix.

- The US should end the year with strong earnings growth thanks to the incredible boom at Nvidia and other Big Techs that made up for the disappointments elsewhere: +40% earnings growth for Mag7 companies that account for over 30% of the S&P. Elsewhere, destocking, rising competition and pricing pressures, and moderate demand in Europe and China have weighed negatively. Europe will end up with almost no earnings growth in 2024.

- Looking at 2025, expectations look demanding. It is not to say they’re impossible, but we would need the combination of a favourable commodities environment, aggressive rate cuts, Chinese stimulus, and a global geopolitical truce. A Harris win sounds like a better backdrop for that to happen (more Fed cuts, allowing China to do more, no incremental trade war).

To conclude, the world is highly uncertain but there are favourable tailwinds like excess oil supply, a global rate cut cycle, and a new posture from China. There is thus no point in being excessively cautious. But ahead of pretty different potential short-term outcomes, markets are legitimately holding their breath. Our investment recommendations continue to rely on the disinflation theme. Within equities, it would especially benefit bond proxies (Utilities, Healthcare, Telecoms) and stocks that could enjoy some cyclical tailwinds from lower rates such as SMID Caps and Basic Resources.

Week ahead: the key event of the week will be the ECB meeting on 17/10 (we expect a 25bp rate cut). In the US, retail sales and industrial production will be released, while the UK and Japan will make CPI numbers available. In China, Q3 GDP, as well as industrial production and retail sales will be released. On the corporate front, the earnings season will see 44 companies listed on the S&P 500 reporting quarterly earnings, of which Goldman Sachs, Citigroup, Morgan Stanley, BofA, Blackstone, American Express as well as Johnson & Johnson, Pocter & Gamble, United Airlines, Las Vegas Sand, Schlumberger. In Europe, 17 companies listed in the STOXX 600 Europe will report, of which ASML, Ericsson, ABB, Volvo.

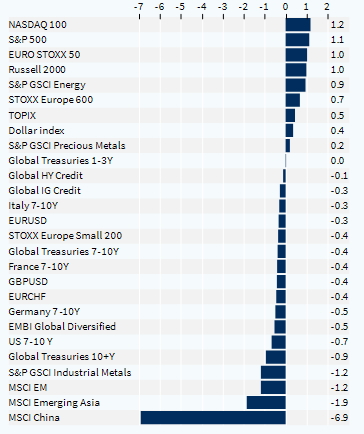

Cross-asset performance (last week, %)