What is going on in French politics? After heated political debates on this side of the Atlantic as well, the first round of the French legislative election confirmed the rise of the far-right (33.1%) in a context of high turn-out (67.5%). The specificities of these elections (2nd round next Sunday with a record number of three-way runoffs) still leave many options open. We expect to have more clarity from Wednesday once second round candidates will have been confirmed.

Markets found reassurances on the small probability that the far-right gets an absolute majority in the French Parliament. At the open on Monday, French banks rebounded, the OAT/ Bund spread tightened and the EURUSD appreciated. Although uncertainty is likely to persist in the next few days, the first round of the legislative election did not bring negative surprises compared to election polls. Importantly, it was not a bloodbath for pro-EU moderate political parties. Our probability-weighted analysis suggests the small rebound on French assets should continue. In any case, the two extreme parties will likely need to compose with the center to form a majority. Yet, a strong relative majority for the far-right would still lead to a complex political equation in France in the next few years.

Diversify France. From a global market perspective, the French-related political uncertainty remains a local factor that can be easily diversified. The implications on asset prices have been regional, not global. The Spanish and Italian sovereign widened further last week (+5 bps vs. swaps). But apart from that, markets have not expressed signs of major concern ahead of the first round of the French election. Japanese equities (OW) kept rallying as the Yen reached multi-decade lows vs. USD. In Europe, we keep preferring the Swiss and UK market, with currency exposure versus Euro.

Bullish bonds. We find that economic surprises are collapsing in the US, but short dated yields remain under the control of the Fed, which has maintained a wait and see approach with regards to rate cuts so far. Next week, the US job market report will contribute to clarify the picture. We expect the upcoming numbers to confirm the disinflation picture and increase the likelihood that the Fed will start cutting rates by September. Investors show rising appetite for bond duration, with impressive inflows into long dated Treasuries (TLT US ETF).

Get ready for the earnings season. Ahead of the start of the earnings season, we revisit consensus expectations. In Europe, earnings growth expectations for 2024 have been revised slightly down YTD, while those for 2025 have been revised upwards (but primarily due to a base effect vs 2024). In the US however, analysts have continued to revise up earnings growth estimates for 2025 (2024 is flat). Sector-wise, Luxury Goods and Autos could see further negative revisions, while consensus expectations for Banks look fair according to our analysts. Chemicals still lack visibility for the second half.

Week ahead. On top of the June job market report in the US, the ISM survey will shed light on recent economic dynamics. In the euro area, the June CPI will be particularly important ahead of the 18/07 ECB meeting. The ECB has started to cut rates but has signalled a back-to-back rate cut was unlikely.

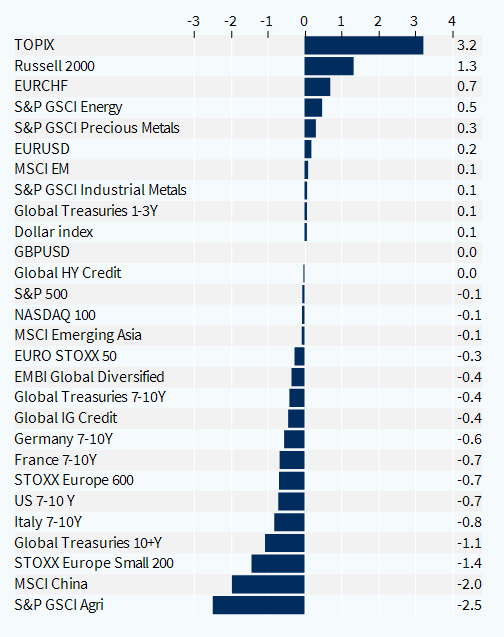

Asset classes performance - weekly (%)