After much speculation and hesitation, central banks eventually reached their much-awaited pivotal moment. In a critical week which saw monetary policy meetings from the Fed, the BoE, the BoJ, the SNB, and the RBA, central bankers confirmed that, outside of Japan, the path forward for rates is downwards.

The Swiss National Bank was the only one to effectively cut rates, and European rates repriced lower in anticipation that lowflation trends in Switzerland are an early signal of what might come next in the euro area. In the UK, inflation for February came in below consensus expectations and the stance within the Monetary Policy Council of the Bank of England was resolutely more dovish. Then, the Fed, by far the most important for global markets, confirmed our view that it had no reason to overreact to the recent CPI/PPI prints, which came in a few basis points above expectations.

There is no doubt in our minds that central banks are much less emotional than markets. Accordingly, we wrote last week that there was no reason for the Fed to change the near-term guidance on rates. Ultimately, the role of central bankers is to set the direction and stick to it because gyrations can be harmful to their credibility and eventually to market functioning. Since 2000, the Fed’s favoured metric to gauge inflation has been the PCE price index (Personal Consumption Expenditure), and the most recent print stood at 2.4% vs. 2% targeted. This is now a modest overshoot. But above all, current inflation is out of sync with the tight rate regime and needs to be adjusted downwards.

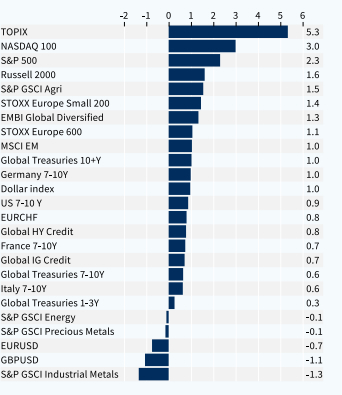

With regards to market implications, US & Japan equities rallied, bond yields fell, and the USD appreciated vs. the GBP, CHF, AUD, JPY, and EUR, though this is not because markets perceived the Fed as being hawkish but rather the other central banks as being dovish. Even the JPY depreciated vs. the USD, despite the fact that the Bank of Japan proceeded to a rate hike, in a completely desynchronized monetary cycle). The underlying message from Kazuo Ueda was actually leaning on the dovish side. And preliminary data for Q4 suggests Japanese households have continued to add to equities as they regain confidence in their stock market. Our view is that the BoJ is unwilling to break this virtuous circle and must consequently act very cautiously, which it did. In fixed income, yield curves remain deeply inverted and forwards are pricing in an inversion until 2026, which is far too aggressive in our view. Fixed income markets probably need evidence of a growth slowdown/negative inflation surprises before pricing in a steeper curve.

Going forward, we continue to believe that there is a lot of value in fixed income vs. equities. Implied interest rate volatility has started to decline in the US but remains high, as central banks are just starting their policy pivot. We continue to find equities richly valued, especially vs. bonds. But we agree that barring an exogeneous shock (geopolitics/US politics for instance), a trend reversal in equities will only occur when the market starts to fear a sharper slowdown/recession than currently anticipated. The momentum in US consumption has started to show signs of decline and excess household savings are now likely to be fully spent. Yet, the labour market remains strong, and consumers are confident. Consensus US GDP growth forecasts have recently been sharply revised upwards, which opens the door to potential disappointments ahead. Overall, we still advocate a slight Underweight stance in equities, while we have started to extend the duration of our bond allocation (reweighting IG vs. HY credit) and reiterated our appetite for gold (and gold miners in equities). Our long US dollar bias, especially versus the CHF, has also met our expectations.

Week ahead: the data release agenda will be relatively light, though in the US, the Conference Board consumer confidence survey, comprehensive consumer spending data for February, and the PCE price index (the Fed’s preferred measure on inflation) will be closely watched. In Japan, the Tokyo CPI for March will matter for the JPY and Japanese equities outlook.

Weekly asset classes performance (%)