The first milestone from the March central bank meetings gave satisfaction to markets. The ECB pre-announced, with some conditions, that the first rate cut will take place with the June meeting, as it projects that inflation will revert to the target in the next 12 months.

Powell also signaled in recent testimonies to the Congress that the Fed is on track to cut rates pretty soon. But as usual, their tortuous communication comes with “ifs and whens”. According to Lagarde, Governing Council members will only know “a little more” in April, but “a lot more” in June. To be honest, we find it a bit comical.

The next milestones are imminent, with the monetary policy meeting of the Bank of Japan on 19 March, the Fed on 20 March, and the Bank of England on 21 March. While the Fed and the BoE are highly unlikely to cut next week, they will send important guidance to markets with their economic projections, dot plot, and so on. The BoJ seems likely to hike rates by 10bps (from -0.1% to 0%). But we expect the BoJ to take baby steps, which could still cause short-term volatility in local FX and equity markets. Ultimately, we believe the BoJ is unlikely to break the virtuous circle which has started to take shape with regards to exiting the deflation trap and restoring Japanese households’ confidence in their equity market.

Meanwhile, the US CPI for February, which will be released in the coming days, will also matter in confirming our peak rates thesis. This has bullish implications for small caps, which we discussed recently, and for gold, which we discuss this week. Gold, to which we are exposed in our asset allocation, is a peculiar asset class which distributes no coupon or dividend. It is negatively correlated to interest rates and is considered a risk-free asset with no counterparty risk. It is an (unperfect) hedge with regards to geopolitical tensions, which remain elevated, and brings diversification due to its limited correlation to traditional assets.

Gold has experienced a sharp rebound since the beginning of March. The rally is a bit enigmatic, since there has been no significant fall in real interest rates, one of the key determinants of gold prices. ETF flows and CFTC positioning data also do not point to a sudden jump in investor demand. In fact, the gold rebound appears related to purchases by the PBOC (12 metric tons in February, 20t on average per month since late 2022), which is likely to remain a key tailwind going forward. After the sanctions on Russia and the asset freeze on the FX reserves of the Central Bank of Russia, there has been a wake-up call for some EM central banks to diversify their FX reserves. Gold is a natural beneficiary of this long-term trend. In the report, we conclude that gold miners are an appealing way to play the theme. They are a leveraged play on gold prices, with a beta of 1.7 in recent decades, they have lagged gold prices YTD, and are attractively valued.

Within European equities, we come back on Tech stocks which have shown the Midas touch since the pandemic. Within the Information Technology sector, we reiterate our slight preference for Software & Services (N) over Semiconductors (UW). Our top down scenario (falling bond yields and rotation into Defensives) would favour secure growth assets such as Software & Services, which exhibit more recurring revenues. For Semis, the bottom of the cycle has been reached, but the market has been playing this theme for over a year. The AI frenzy has also tended to mask the challenges still affecting the semiconductor sector, notably the prolonged inventory digestion in the industrial end-market. As the US elections approach, Software is also more immune to geopolitical risk, with barely any exposure to China. Valuation-wise, neither sector offers a very good entry point. Within Software & Services, we highlight that the Services segment looks more appealing and could eventually enjoy a cyclical recovery.

Week ahead: watch US CPI and retail sales. The market focus will then switch to the central bank meetings in Japan, the US, and the UK between 19 March and 21 March.

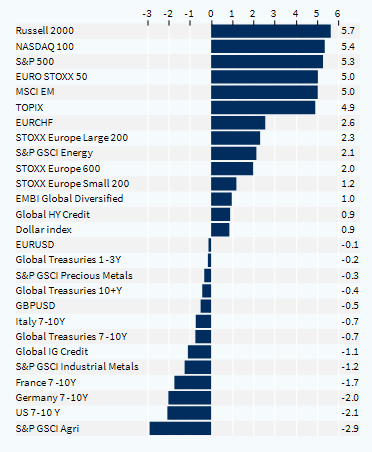

Weekly asset classes performance (%)