On top of geopolitics and inflation concerns, now investors have to deal with another layer of complexity: renewed concerns about fragmentation risk in the euro area.

Basically, it comes down to the idea that a security issued in euros in France or in Italy is not as safe as a comparable asset issued by a German entity. It reflects the fact that the euro area is a hybrid economic system with a common currency but limited fiscal coordination. Such fragmentation risks have vanished since Draghi’s “whatever it takes” moment in the summer of 2012 in London (as the UK was inaugurating the Olympic games, a funny parallel with the Paris Olympic games next month). But they are now back with a vengeance after Macron called snap elections a week ago.

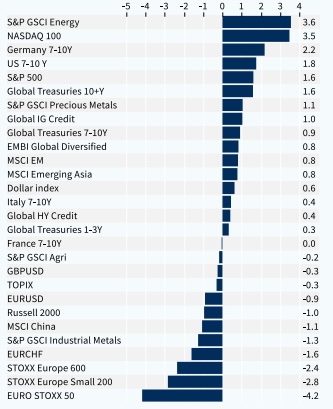

The rise of the far-right in France, which advocated for a Frexit some years ago and whose programme for the 2022 presidential election was quite expansionary on the fiscal side, brings financial stability concerns. Especially as France was not a good pupil on fiscal orthodoxy in the past decade, as we show in the report. Sovereign bonds in France sold off last week, while European banks and the EUR/USD are facing severe selling pressure.

In our view, the next few weeks will remain volatile as election polls show moderate centrist parties being squeezed by the extremes, both on the left and on the right. All the election polls that have been released since Macron called snap elections are consistent. They show Le Pen’s far-right above 30%; the leftist coalition above 25%, and Macron’s centrist coalition below 20%. The most likely outcome of this election is a hung Parliament, but the ability of the far-right to gather a majority cannot be excluded.

Uncertainty will not be cleared up until 7 July, when the election runoff will take place. And our experience accumulated over the past couple of decades suggests that many things can happen in financial markets in three weeks. As a result, diversification is king. In our allocation, we had no direct exposure to French sovereign bonds and turned Neutral on European banks several weeks ago. However, we proceeded to make the following changes to hedge our portfolio against an additional deterioration of market confidence: we fully trimmed our exposure to Italian BTPs to the benefit of UK Gilts (along with long GBP/EUR exposure). Of course, one could argue that, with a general election scheduled to happen on 4 July, the UK is not immune to political risk. But our perception is that, following the failed Truss experiment last year, any future government will proceed cautiously on the fiscal front, which makes it unlikely that politics will have a marked impact on UK assets. We also reduced the exposure to European equities, to the benefit of EM sovereign credit in USD, hence reinforcing our long USD bias versus EUR.

Meanwhile, trade wars are raging, as the EU finally adopted sanctions against Chinese BEV carmakers and now expects trade retaliation measures from China. We closed our position on EM Asia equities in late May, but we stay invested in EM ex-China equities. On European equity sectors that would be the most exposed to the risk of retaliation from China, we revisit our Underweight on Autos as well as the possible impact on cognac producers in the context of our Strong OW on Food & Beverage. This review leads us to downgrade the F&B sector by one notch to OW. Note that we downgraded the Luxury sector to Neutral some weeks ago (note here), which is another sector China might target. Overall, Food and Beer continue to have defensive merits, trading on its long-term valuation average.

Finally, US assets are offering a lot of diversification at present. Signs that the job market is cooling (initial jobless claims) and the surprisingly weak CPI dragged yields lower and fuelled US equities last week. The pieces of the growth deceleration puzzle are gradually falling into place in the US, as we have been expecting. The FOMC meeting was marginally hawkish last week, revising up the guidance on rates in 2024 and 2025. But Powell’s press conference softened the tone. The dot plot eventually aligned the Fed guidance with market expectations and, as Powell reiterated, the dot plot is not a commitment. It is just a survey of FOMC participants (including non-voting members). Overall, and once factored into our expectation that disinflation will carry on over the coming months, we think that the door to a first rate cut in September remains open. However, we now bet on two 25bps cuts this year (September and December) as opposed to three previously.

Week ahead: In the UK, the CPI is expected to have decelerated in May, while the BoE meeting should leave rates unchanged. In developed markets, preliminary PMIs for June will be available. In the US, retail sales will be released.

Asset classes performance - weekly (%)