A new beginning. With political risks increasingly in check in France and US inflation surprising on the downside, there is room for a reversal in recent trends, which saw US big-tech equities driving global markets to an extraordinary extent. The rising probability that the Fed will be in a position to start cutting rates by September is leading to rotations into long-dated Treasuries, and from large caps to small caps in Europe and the US. Although such movements have proved short-lived in the past, we believe the disinflation trend will now become more convincing for central banks. We re-weight European equities at the expense of the US in our asset allocation but remain UW equities overall.

A postcard from Paris. In France, markets remain moderately cautious as leftists came first in the legislative election and their programme is viewed as far too expansionary. Yet, due to the unprecedented degree of fragmentation in the political landscape, we think that Macron will be compelled to nominate a moderate Prime Minister. But it remains unclear whether the next Prime Minister will be nominated in the coming days, or whether Macron will wait for September, i.e. post-Olympic Games.

Mind the gap. In the US, the earnings season is starting, and companies like to surprise markets. Yet, the consensus for the S&P 500 compiled by FactSet suggests that analysts revised Q2 earnings estimates downwards by less than usual last quarter. We believe the scope to surprise investors after the recent equity rally is quite limited. Analysts expect EPS for the S&P 500 to have grown at 8.8% in Q2 2024, year-over-year, with EPS growth for Tech/Communication Services and Health Care expected at 16-18% vs. Q2-2023.

The seasonality effect is typically adverse as we head into the summer months. We show in this report that August and September have been the weakest months in terms of S&P 500 performance over recent decades. Our technical analyst also turns more cautious on the Nasdaq. Yet, longer term, the increasing likelihood that Trump will be re-elected could prove supportive for risk assets. Also, the risk of recession appears relatively remote, as the current signs of consumer spending and labour market moderation should help the Fed in terms of easing the monetary stance and support the economy.

European bond proxies. With the expectation that US 10Y yields will continue to slide, we reiterate our positive stance on key bond proxies such as Real Estate, Food & Beverages, Household and Personal Care, Business Services, and Med-Techs.

We also upgrade the Utilities sector to OW (Neutral), which is the second-most inversely correlated to US 10Y rates. You shouldn’t be surprised; we flagged the opportunity in Renewables some three months ago, as they looked excessively battered but are key enablers of the energy transition in the EU. That transition is not only required for green purposes but also because it offers a way to cut power prices and reduce the EU’s dependence on imported fossil fuels. With bond yields falling, another big component of the Utilities sector should perform better: the network companies (our top picks: Elia, Redeia, and E.ON). These companies are regulated and have huge growth opportunities, as renewables need a broader power grid.

Week ahead: In Europe, attention will switch from Paris to Frankfurt and Strasbourg. In Frankfurt, the ECB will hold its policy meeting, and while it is almost unanimously expected to keep rates unchanged, its communication will likely signal that it remains on track to proceed with a second cut in September. In Strasbourg, the European Parliament will vote on whether Ursula Von der Leyen will see a second term as President of the European Commission.

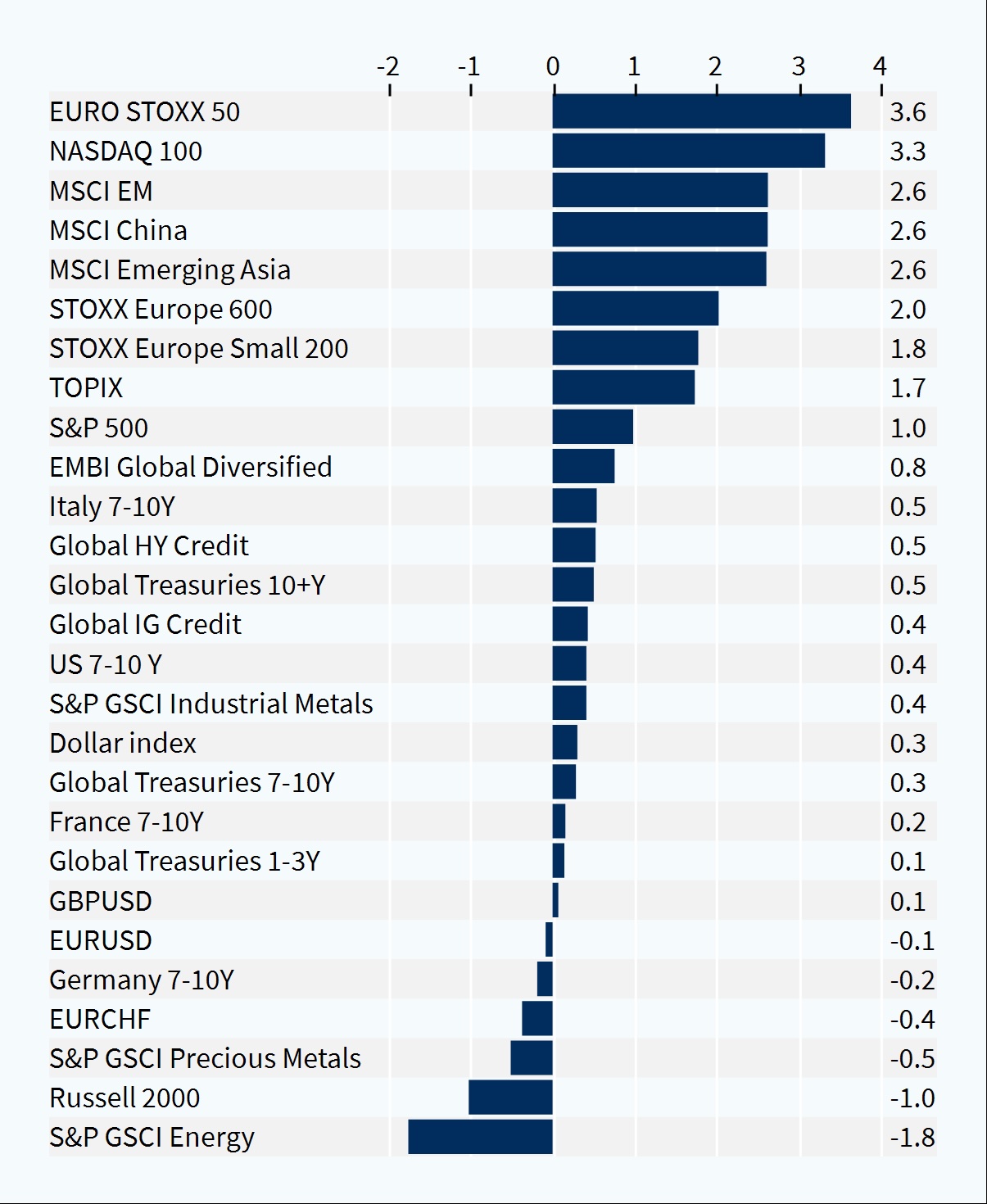

Asset classes performance - weekly (%)