The Paris Olympics will get underway at the end of the week amid an unusually gloomy mood. Not only has tourism been a disaster in June, but everyone is holding their breath, awaiting the back-to-school season with some wariness, and asking: Who will run France?

The French political scene remains fluid and unprecedented. In a first test of the new Parliament last week, Macron’s candidate as Speaker of the lower house was re-elected. She won with the support of the moderate right but the left is already threatening legal action. Even though this outcome suggests a centre-right coalition might be able to form a government, it is apparent that 56% of the assembly (Nouveau Front Populaire + Rassemblement National) would not be represented in such a government. But should the moderate left eventually break its NFP alliance to join a government, the opposition would be composed of remaining extremes that have no majority. A similar feeling that the election results have been disregarded is occurring on the EU scene, where the re-appointment of Metsola (European Parliament) and Von der Leyen (European Commission) occurred despite the far right’s significant gains in the last election.

This in stark contrast with what is happening in the US, where the rise of Trump seems irresistible. Trump is pitching, with apparent success, a platform that is pretty close to that of the EU far right: support for purchasing power and businesses through low energy prices and tax cuts, scaling back the green agenda, and curbing migration flows. It is all the more alike if you add the trade dimension and a certain degree of scepticism towards the war in Ukraine. What is still not clear to us is the extent to which Trump’s trade and migration agenda would benefit the US economy. However, in our view, a lot of investors will probably recall the experience from his first mandate, where he very much treated the level of the S&P like the key benchmark for measuring his own success. Also, Democrats’ proposal to raise corporate taxes makes Trump a relative favourite of Wall Street.

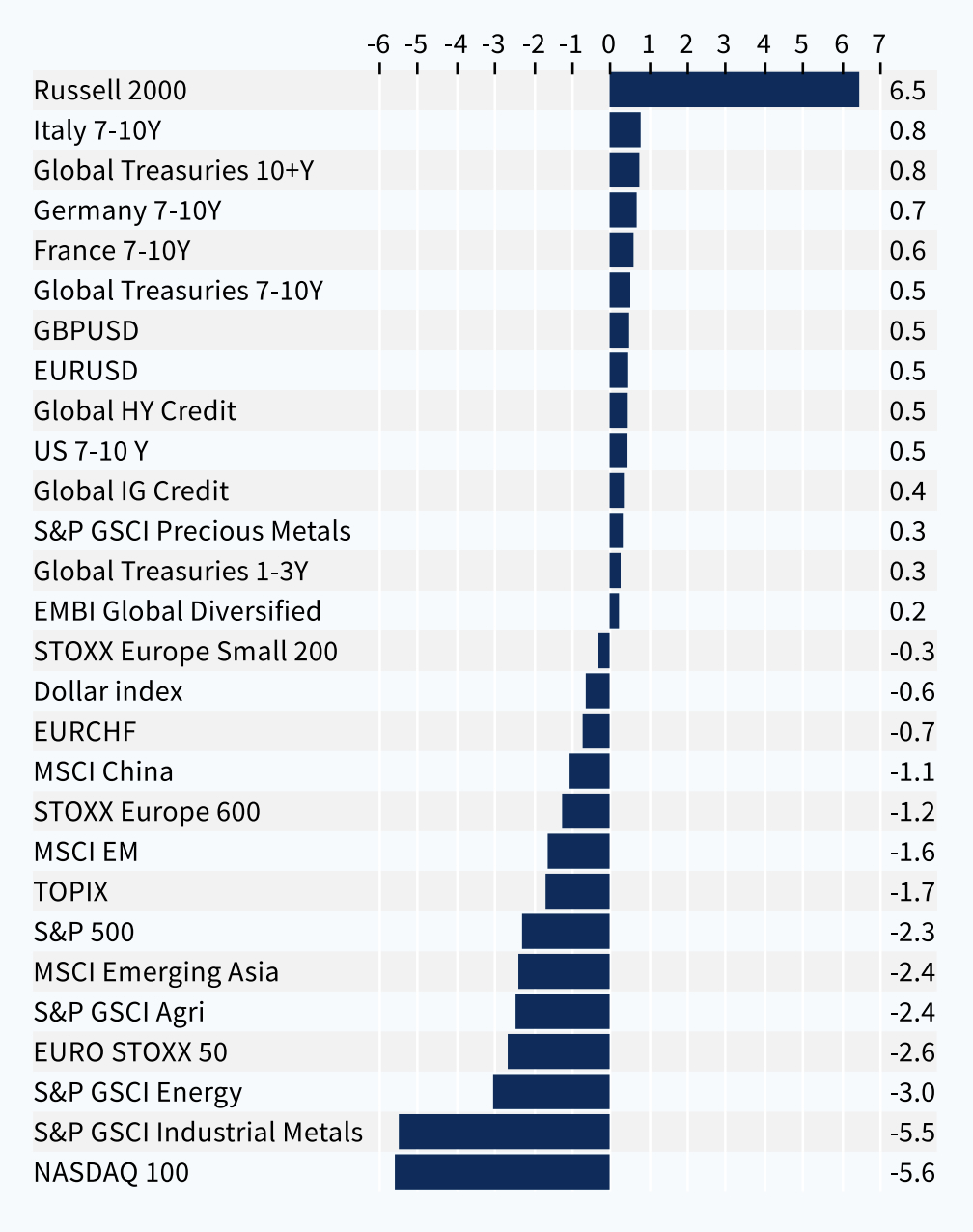

It is in that context that the “great rotation” has been taking place over the last ten days, which has seen some violent profit taking on Big Techs to the benefit of US treasuries and US SMID Caps. Europe replicated the trend on its own scale with the Eurostoxx 50 (highly concentrated) underperforming Small Caps. In our view, the CPI surprise and the probability of a Trump victory have played in synch:

- A Trump win would reinforce the chance of a favourable fiscal backdrop for US companies and the “America First” agenda favours domestic stocks against global exporters on a relative basis. His lack of enthusiasm for Big Techs that challenge his power and his sudden reversal on TikTok don’t help the sentiment on the large technology names. His trade policy would pose huge challenges for Apple, for instance. After all, the Magnificent 7 have rallied by 40% YTD! Any pretext can justify some profit taking at this altitude.

- The good CPI data and the accumulation of evidence of a softer US economy all plead for looming rate cuts. We have shown in recent months the correlation between SMID Caps and rates. In our view, this is related to smaller companies’ balance sheets (weaker and more exposed to floating rates) and their exposure to interest-rate-sensitive parts of the economy. Meanwhile, high treasury yields haven’t prevented the Magnificent 7 from performing extremely well, with their growth being so uncorrelated to US GDP and entirely driven by the AI boom. Thus, they’re not the obvious winners when rates fall.

We make the case in our report to explain why the direction of travel might still be higher for US SMID Caps, even if the odds of a Trump victory might be peaking with Biden having dropped out of the race last night. We note the betting odds of the Trump scenario barely moved. But the campaign is still very long.

Can European SMID Caps follow their US friends? Absolutely (note we turned more optimistic on the SMID relative performance at the end of March and this trade is up 4% since then). However, with the track record of stronger GDP growth in the US and potential trade disruption if Trump wins, we find it easier to defend US SMIDs over European SMIDs.

A short note from Kepler Cheuvreux: Dear Readers, the summer break is upon us, and the next article will be available on August 19th. We wish you an excellent vacation.

Cross-asset performance (since Nasdaq peak on 10 July, %)