Emerging markets are making a remarkable comeback, both in the minds and portfolios of investors. After a remarkable 2025 (+34%), the iShares MSCI Emerging Markets Index is accelerating even further, rising by nearly 12% in the first six weeks of 2026. This resurgence can be attributed to several factors, and we believe it has a bright future ahead.

First, investors are diversifying their positions outside the United States. The geopolitical argument is fully at play here. Last year, the Trump administration's abrupt reversals in its trade war already raised numerous questions about America's primacy as an investment destination. In recent weeks, the extreme tensions surrounding Greenland and the pressure exerted by the Trump administration on the Federal Reserve have heightened their distrust. From an economic perspective, growth in emerging markets offers promising prospects, with the IMF forecasting GDP growth of 4.0% in 2026, compared to only 1.6% for advanced economies.

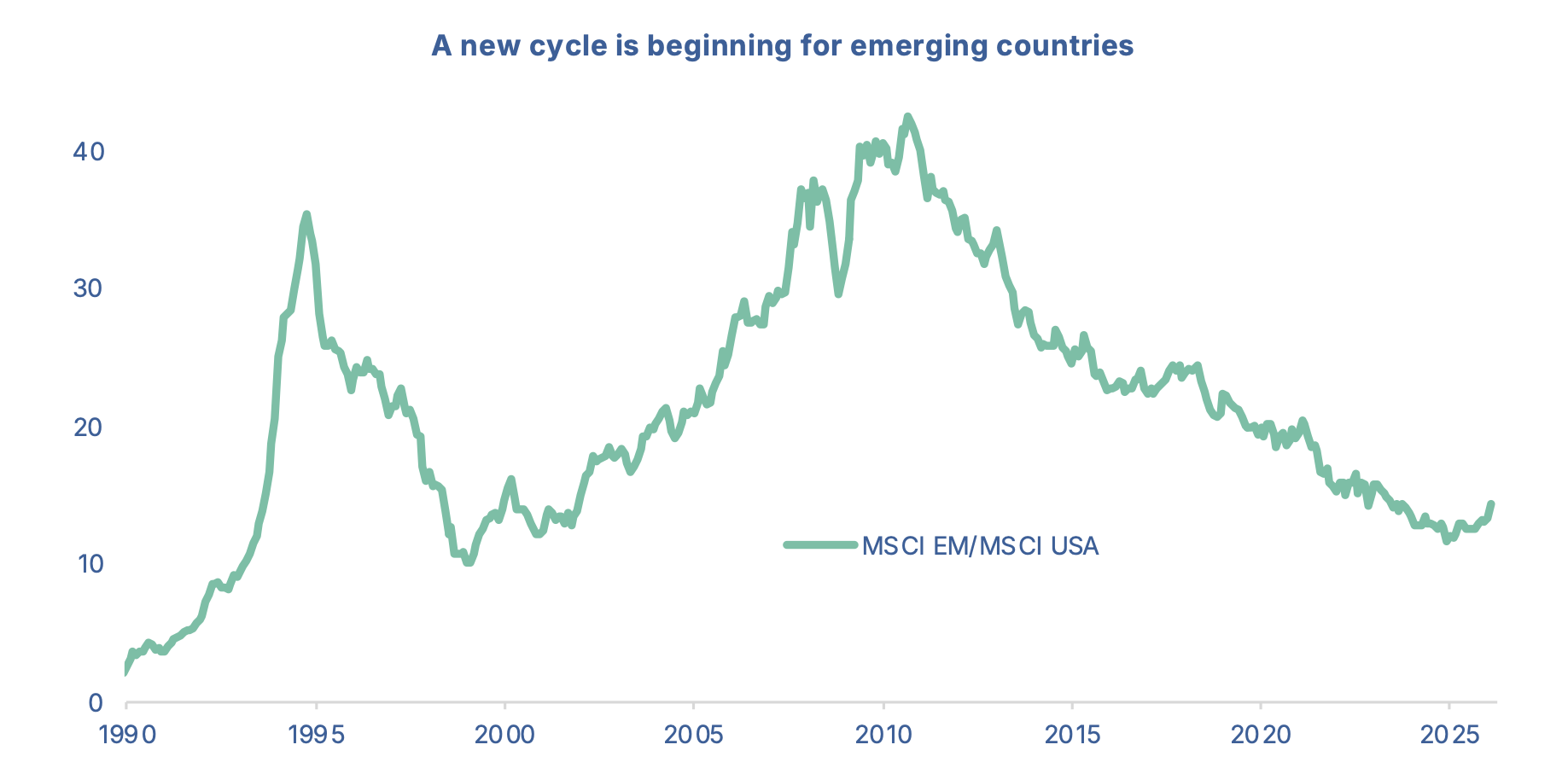

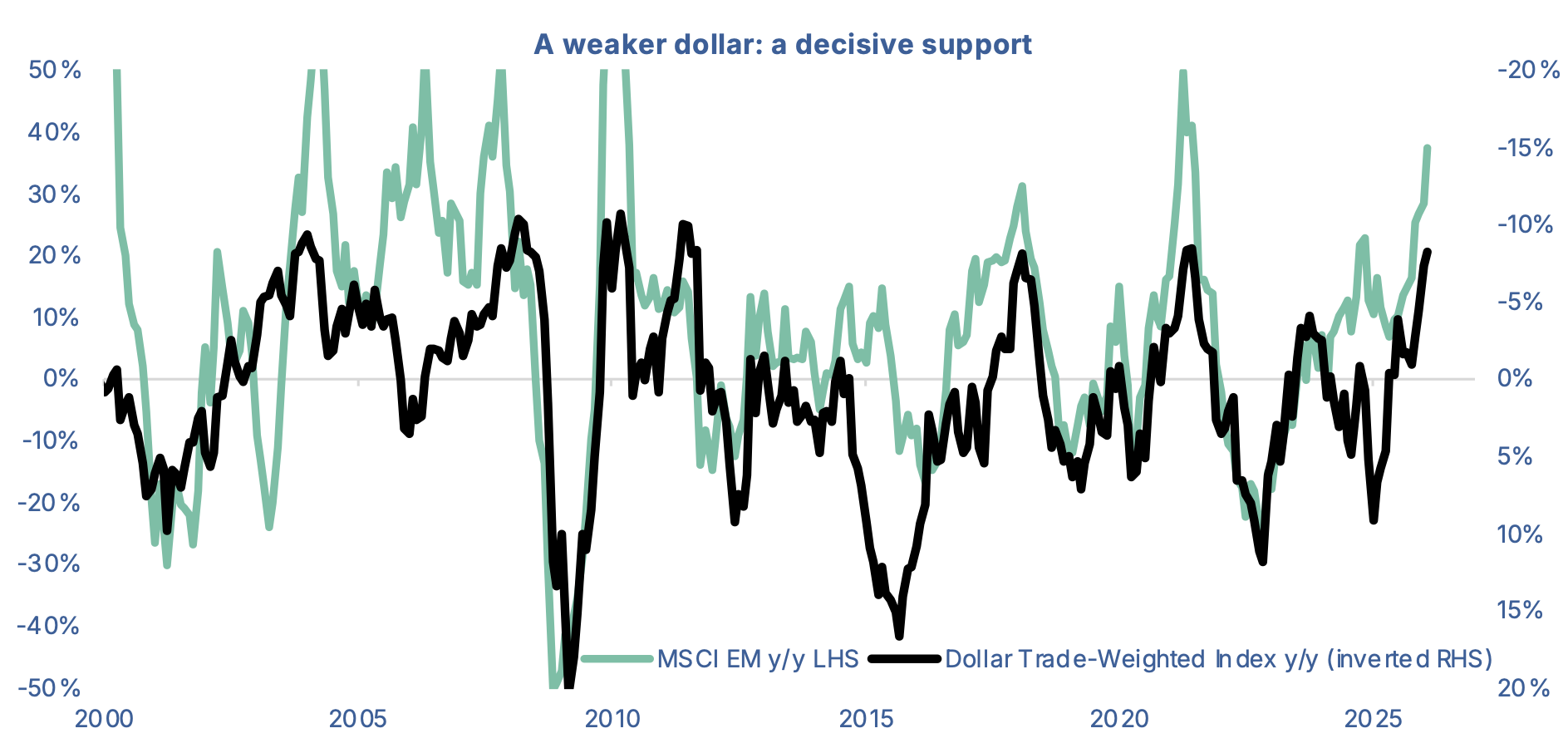

The dollar is naturally the transmission belt for these international reallocations. Historically, its depreciation has been a powerful driving force for emerging markets. Thus, cycles of the greenback's decline are synonymous with outperformance of developing economies relative to the United States. The last emerging market "supercycle" occurred in the first decade of the 21st century, between the bursting of the dot-com bubble and the Great Recession.

This was followed by a period of American hegemony in equity markets, marked by the rise of the latest generation of major technology companies, the GAFAM (Google, Apple, Facebook, Amazon, and Microsoft). With the United States attracting global capital, the dollar logically strengthened considerably from 2011 to 2024. But since Donald Trump's return to the White House and the US government's recognition of the need for a multipolar world, the world's reserve currency has lost its lustre, and emerging markets are benefiting.

So how do we navigate the emerging cycle that is now unfolding? To simplify this inherently complex reality, we adopt a three-dimensional framework. First, a crucial factor for these countries is macroeconomic dynamics , both local for continental countries like India, and global for more export-oriented economies like Vietnam.

Second, the technology sector has become central. The largest companies in an index like the iShares MSCI Emerging Markets belong to this segment: TSMC, Samsung, and SK Hynix. The first of these is none other than the Taiwanese semiconductor giant, while the next two are Korean and part of the global oligopoly dominating memory technologies.

Finally, commodities play a decisive role for multiple geographic regions, particularly in Latin America, the Middle East, and Africa. Of course, many countries are at the intersection of these three factors, such as China (between economic and technological sensitivity) or Brazil (economy/raw materials).