Micro meets macro? As the earnings season gains momentum, we note that micro level trends are starting to mirror the broader macroeconomic shifts that have been brewing for some time. Cooling inflation is now being reflected in the pricing contribution of sectors that had benefited from the lower price sensitivity of consumers over 2021-23, thanks to pent-up demand and excess savings. Companies are now apparently giving back purchasing power to consumers via lower price hikes, which is more evidence that some consumers are struggling to keep spending (as shown by rising credit card delinquencies or depressed savings rates). The geopolitical risks associated with China are also starting to take their toll on some European businesses such as carmakers, luxury goods, and beverages.

Not yet a great buying opportunity for equities. From an equity strategy perspective, we think the next few weeks should remain challenging, which would be consistent with the adverse seasonality observed historically in August-September. Although the main equity benchmarks have already dropped by c. 5% since their peak (with some indices closer to 10%, like Nasdaq 100), we do not think they are offering a compelling entry point yet, especially in the US. The S&P 500 is still up by a strong +14% YTD and trades at a hefty valuation (21.4x, close to the peak observed in 2021), on demanding earnings growth expectations (+10% in 2024E and +15% in 2025E).

The global macroeconomic backdrop is unlikely to provide much support. China is struggling to revive its economy and in the Eurozone the good momentum observed in Q1 is already fading, with expectations for a second-half recovery increasingly being pushed into next year. Although the US economy remains relatively strong, economic disparities are widening, and the labour market is softening.

Central banks to the rescue? Meanwhile, Western central banks appear unwilling to ease much faster as they remain concerned about derailing the disinflation trend. This week, we expect the Fed to confirm that if a rate cut is on the horizon, it intends to proceed cautiously.

US election uncertainty. Finally, the uncertainty surrounding the US elections should lead investors to refrain from taking on additional risks. The possibility of a Harris presidency (corporate tax hike?) might not be as market-friendly as a Trump victory (deregulation and tax cuts).

In this context, we reiterate our preference for defensive sectors, which have finally started to bounce back against cyclicals in European equities. As a reminder, we recently upgraded the Utilities sector from N to OW (15/07), and we also have a Strong OW rating on the Telecoms sector. Today, we reiterate our OW stance on the Pharma & Biotech sector, which is one of the most defensive sectors in our coverage and where results have been very supportive (guidance raised at many drugmakers).

In anticipation of further weakness, this week we downgrade the Banking sector to UW (from N). The sector has performed extremely well YTD, but the earnings momentum is likely peaking as interest rates begin to decline and the domestic economy remains sluggish with normalising corporate defaults. Although French political risk seems well priced in, it also seems skewed to the downside with at best political gridlock and at worst more turmoil should French politicians need a reminder from the market that they have commitments to honour. Still, our Reduce rating is more tactical than structural given the sector’s undemanding valuation and the potential for more re-rating once the market sees where returns land, with interest rates unlikely to revisit the lows from the 2015-21 period.

Week ahead: US consumer confidence and job openings, first estimate of Eurozone Q2 GDP (Tuesday), Eurozone CPI, FOMC meeting (Wednesday), US manufacturing ISM (Thursday), non-farm payrolls report (Friday).

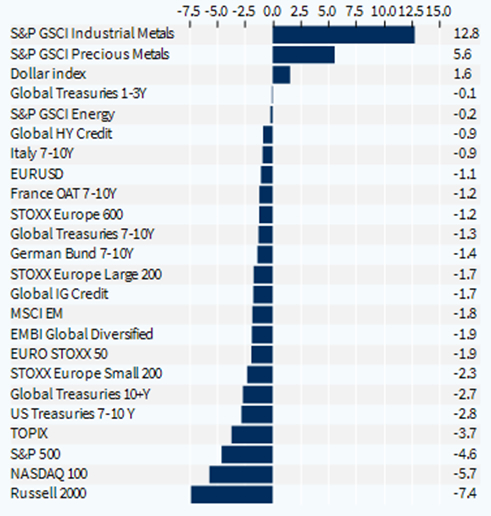

Cross-asset performance (last week, %)