Credit risks in the US are keeping markets on edge. Concerns about the US regional banks' creditworthiness caused some market jitters last week. The KBW regional banking index was down 6.3% in a single day, after two banks (Zions Bancorp and Western Alliance) disclosed issues with bad and fraudulent loans. The regional banking industry has been under scrutiny after First Brands, an auto parts supplier, declared bankruptcy in late September.

- At the end of last week, Zions Bancorp and Western Alliance rebounded, suggesting that market concerns are easing and credit risks remain idiosyncratic, not systemic. In the large caps space, BofA’s loans to First Brands are reported to be secured by strong collateral, and Morgan Stanley communicated that they have no exposure.

- Coupled with the government shutdown and the flare-up of trade tensions between the US and China, there are good reasons for markets to take a breather after the bull run since April. Yet, US equities extended gains last week, buoyed by a string of positive earnings surprises.

Should you be concerned about the government shutdown? The ongoing shutdown that started on 1 October is on track to be one of the longest ever. We do not expect significant market implications, as shutdowns are typically short-lived and tend to affect only non-essential public sector functions. The longest shutdown lasted 35 days during Trump’s first mandate, and during that time, the S&P 500 was up 10%...

Should you be concerned about the flare-up of trade tensions with China? In the past, we were more worried than we are today about trade tensions between the two superpowers. Trump swiftly backed down after threatening an additional 100% trade tariff on China, and the meeting between Xi Jinping and Donald Trump at the APEC summit in Korea is still live. As anticipated, market vigilantes are proving to be a powerful check on Trump’s actions.

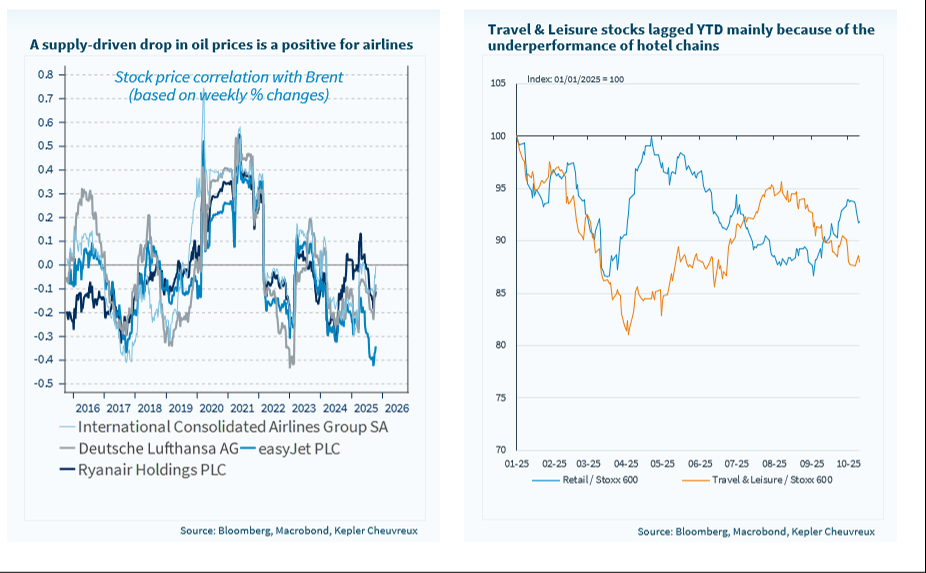

A notable positive development for consumers has been the significant fall in oil prices. We believe its decline has more to do with oversupply, and we do not think the process of adjustment is over. We see the oil price testing below USD 60/b in the coming months unless geopolitics derail the oversupply situation. We look at this in more detail in today’s report and reiterate our UW stance on the Big Oils (Energy) and our preference for Travel & Leisure stocks that benefit from low energy prices, especially airlines.

No market implications from S&P rating downgrade of France by one notch to A+. The market is rather focused on the fact that Lecornu's government survived his first test. The no-confidence motion from the opposition obtained 271 votes, while it needed 289 votes to be passed. This success was thanks to the suspension of the pension reform, which secured the Socialist Party’s neutrality. Lecornu has secured a respite but is facing some difficult weeks ahead to get the parliament’s approval for a budget. A messy dissolution cannot be ruled out early next year.

- Moody’s should follow this week on 24 October with its own rating review. We think these rating actions are already reflected in French bond prices, but we see no proper relief as long as a credible leadership gets popular support for some durable actions.

Week ahead: Earnings season is in full swing. Ninety-two companies listed in the S&P 500 will report this week, of which 21 are industrials (Lockheed Martin, Northrop Grumman, RTX, General Dynamics, General Electric…). Within the consumer discretionary sector, General Motors and Ford Motor Company will report. Within Tech/Communication Services, Netflix, Intel, IBM, Texas Instruments, AT&T, and T-Mobile will report quarterly earnings. The week will also be quite busy for the healthcare sector. Overall, the consensus expects EPS to grow 8% for the S&P 500 in Q3. With the usual positive surprises, it is on track to grow at double digits for the fourth consecutive quarter. Sectors such as Tech, Utilities, Materials, Financials and Industrials are expected to see EPS grow at double digits.

In Europe, the earnings season is at an earlier stage, with 30 companies having reported earnings so far, but it will gain momentum with 80 companies reporting quarterly earnings next week, with a large representation of industrials/materials (SAAB, Atlas Copco, Akzo Nobel, Boliden, Norsk Hydro, SSAB) and financials (Unicredit, Barclays, Swedbank, SEB, DNB Bank).

Travel & Leisure (OW) to benefit from lower oil prices