The impossible trinity is a theory in international economics which states that it is impossible to have, at the same time, a fixed exchange rate, free capital movement and independent monetary policy. A good illustration of its validity relates to the experience of Emerging Markets across Asia and Latin America some decades ago. In the mid- to late nineties, they tried and failed to simultaneously pursue all three goals. By then, currencies were pegged to the US Dollar and capital movement was relatively free, while Greenspan was hiking rates in the US. The lost monetary independence forced them to adopt restrictive policies that hurt growth prospects and led to massive capital outflows, dramatic devaluations, and debt defaults.

In the post-US election context, we argue that Trump faces his own impossible trinity. His aggressive rhetoric on immigration and trade has probably largely contributed to his victory. But it turns out that such policies are impossible to implement without reigniting inflation, which was the top issue for voters in polls. Hence, it is not possible for voters to get protectionism, no immigration, and low inflation at the same time. Most estimates suggest that the trade and immigration agendas, taken separately or together, would hurt the economy and fuel inflation. Fiscal stimulus, deregulation and improved public spending efficiency could help to balance growth, but the net impact of his programme would still be deeply adverse. The main risk with Trump’s playbook is thus the stagflation risk, which is adverse for both equities and bonds, like in 2022. Commodities, the US Dollar, and inflation-linked bonds would be among the very few hedges for long-only portfolios in that scenario. Yet, radical policies come with their own checks and balances, more so in the US than elsewhere.

Voters are asking for policies that would be adverse for investors, but voters are also investors. We show in the report that US households have a significant share of their financial assets in equities. Any controversial policy causing a severe pullback in equities would be adverse for Trump’s opinion polls and would put at risk the Republican majority in Congress ahead of the 2026 midterm elections. There is evidence that Trump’s trade war was a key factor behind the Republican defeat in the 2018 congressional midterm election, as Republican candidates lost support in counties more exposed to tariff retaliation but saw no appreciable gains in counties that received more direct US tariff protection. Then, with regards to mass migrant deportation, it would cause severe labour shortages and wage increases in agriculture-producing States that vote Republican… In this context, the key challenge for Trump will be to avoid disappointing his voter base, while he probably knows that there is almost no path to deliver on his programme while keeping inflation in check. The next Treasury Secretary, Scott Bessent, will have a tough and precarious job…

Where do we go from here? From an investment perspective, there are several paths as we head into 2025.

- Cautious and risk-adverse investors will argue that Trump is sufficiently unpredictable and determined to go on. Under this scenario, there is a volatile year ahead of us, with markets willing to test Trump’s determination, like in 2018.

- In our view, Trump is surrounded by money-managers who understand financial markets and can warn him when he is not the right track. We are not fully sure whether he will pay attention to them. However, the recent hesitation surrounding the Treasury Secretary nomination suggest that Trump is paying attention. Moreover, the S&P 500 is one of Trump’s yardsticks for evaluating success. Overall, richly valued US equity markets and the strong performance in recent years do not point to a massive opportunity across US market segments. But small caps remain attractive, and we also expect US banks and consumer discretionary stocks to perform well going forward. Tech-related stocks are having their own cycle, which remains supportive in 2025 as mass AI adoption continues to take shape.

- In Europe, challenges are big enough to cause political instability in France and Germany. Every country is polarised around immigration issues, purchasing power concerns, and limited fiscal room to satisfy voters (Germany does not have this latest problem, at least). Low growth, vulnerability to trade wars, and to China, have international investors on the sidelines. It seems too premature to play European consumer discretionary names (Luxury, Autos) but many European companies have business in the US and are in good position to capture growth opportunities there: we recently upgraded Medias (top pick Publicis), we stay Overweight Telecommunications (Deutsche Telekom to play the US market) and Utilities (high dividend, domestic exposure, rate sensitivity but rates in euros have diverged from rates in USD). We also recently reweighted banks (shareholder-friendly policies, no exposure to trade wars, valuation). SocGen would be the largest beneficiary if European integration accelerates, in reaction to Trump’s isolationist policies, and the banking sector consolidation moves forward.

- We stay away from China and EM equities but continue to find value in EM sovereign credit. Finally, we stay Overweight US High Yield credit to leverage the buoyant economic cycle (low default rates) and low duration features. In FX, we stay long the USD despite the recent rally, which may continue in our view.

Week ahead: Preliminary estimate for the euro area’s November CPI will be released. In the US, consumer confidence (for November) and the October PCE deflator (the Fed’s preferred measure of inflation) will be released.

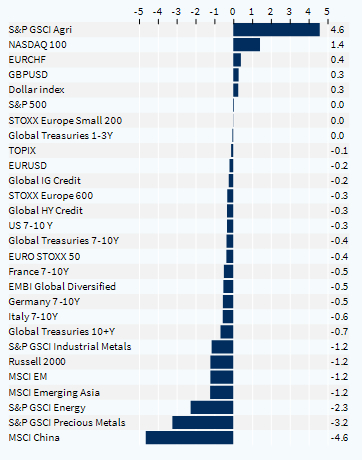

Cross-asset performance (last week, %)