As we approach year-end, we take a fresh look at the current market dynamics. Another strong earnings season in the US Tech and Consumer Discretionary sectors (Google, Apple, Amazon) has helped to sustain global risk appetite, fuelling equities higher. The trade truce between China and the US also brings renewed visibility.

- The bullish mood has been reflected in massive ETF flows globally, with over USD40bn per week collected for a record seventh week into the end of October, according to Kepler Cheuvreux/Trackinsight ETF teams. Every asset class recorded inflows, though recently, gold and EM equities/China have seen some outflows.

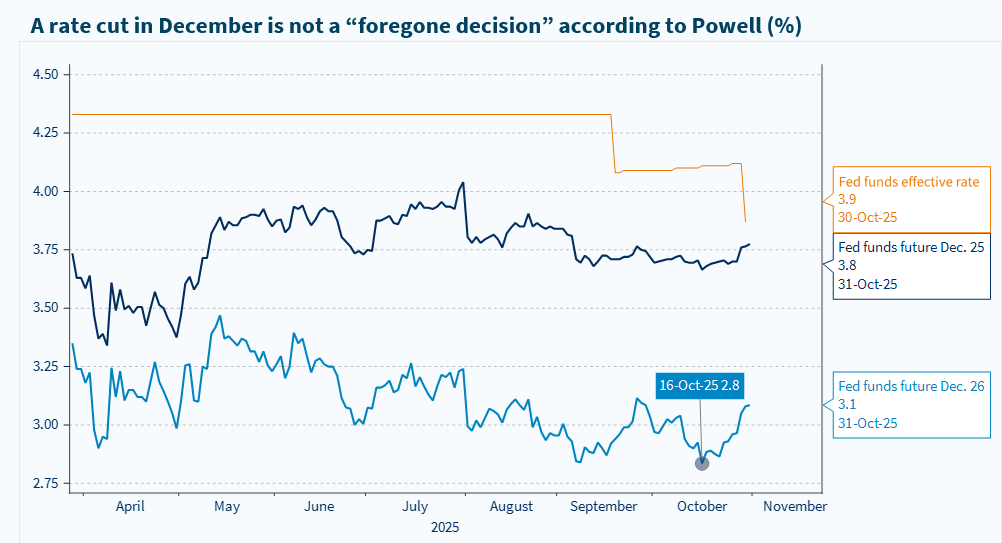

In the face of prevailing bullish sentiment, investors must navigate yet another period of lofty valuations across asset classes, except perhaps in sovereign bonds. The room for disappointment is thus limited. Also, the Fed appears slightly less supportive of risk takers, with Powell guiding short-term rate expectations higher, despite a largely expected 25bp rate cut at the FOMC meeting last week.

- In our view, Powell’s slight hawkish bias, saying that a December rate cut was far from certain, is rather positive, as FOMC participants’ concerns over the labour market have receded slightly. Meanwhile, Powell sounded confident that the tariff shock would not result in any meaningful increase in inflation.

- The government shutdown is leading the Fed to act more cautiously, but overall, we see the repricing in US rates as an opportunity if it gains some traction. Keep in mind that the Fed reshuffle will have a dovish bias in the next months as Trump moves early next year toward nominating the next Fed chair.

Earnings surprises suggest there is no reason to be excessively defensive. With more than 60% of S&P 500 companies having reported quarterly earnings, the key takeaways are as follows: 1) earnings growth for those companies having reported stands above 10% in Q3 (YOY) at the time of writing. If confirmed, this would be the fourth consecutive quarter of double-digit EPS growth; 2) among the 318 companies that have reported, 75% were above expectations, with Technology and Financials in the 80-95% range; and 3) the largest surprises in dollar terms also came from these two sectors, as well as from Industrials, Materials, Healthcare and Consumer Discretionary.

- In Europe, less than 50% of the companies listed in the STOXX Europe 600 have reported quarterly earnings. The main takeaways are: 1) earnings growth stands at 6% so far in Q3; 2) among the 245 companies that have reported, 60% managed to beat expectations, with Healthcare and Consumer Staples above 80%. Interestingly, the largest aggregate surprises (in euro terms) also came from Technology and Financials, as well as from Industrials, Materials, Utilities and Real Estate.

Gold: The winning streak faces a reality check. Is this the end of the story? A couple of weeks ago, we highlighted that Gold appeared to be technically overbought. In the past two weeks, price momentum has faded and Gold ETF’ recorded outflows. In our view, following a strong performance, Gold was due for a breather. Also, ETF flows appear to reflect retail sentiment, which can be volatile. Gold is indeed a risky asset, with realised volatility slightly above that of the S&P 500 in the past three years. But gold’s appeal in portfolios remains intact.

- We show in our report that, over the past twenty years, gold has delivered the same performance as equities, without a significant correlation to the latter. A resolution of the Ukraine–Russia conflict would be a negative for gold, at least temporarily, much as the recent easing of trade tensions between the US and China appears to have contributed to its pullback over the past ten days. However, the Ukraine–Russia conflict seems unfortunately unlikely to be resolved in 2025.

Eurozone macro: Slightly better than expected, the ECB stays put, what’s next? A flurry of economic indicators (PMI, Q3 GDP, economic confidence, IFO Germany) suggests that economic activity remains weak but slightly better than expected. According to the ECB, monetary policy in the euro area is “in a good place”, but in our view, there is no reason for celebration. Weak growth conditions, low oil prices, and a strong euro should push inflation below the 2% target in 2026, and we believe the ECB will reinitiate rate cuts in H1 2026.

- With regards to European equities, while we upgraded the Technology sector to Neutral a month ago, our preference is for attractively valued Defensive Growth such as Healthcare. We show in our report that both European pharma and MedTech continue to experience a positive reversal, along with Luxury stocks.

The repricing of rate expectations offers opportunities, as Trump will nominate a dovish Fed chairman in early 2026