In recent months, Argentina has taken another step forward in its economic reforms. Progress is becoming more evident, and the peso has been freed from a strict foreign exchange control regime. Capital controls have been largely eased, and the IMF is convinced by Buenos Aires' efforts. Argentine financial assets are becoming investable again.

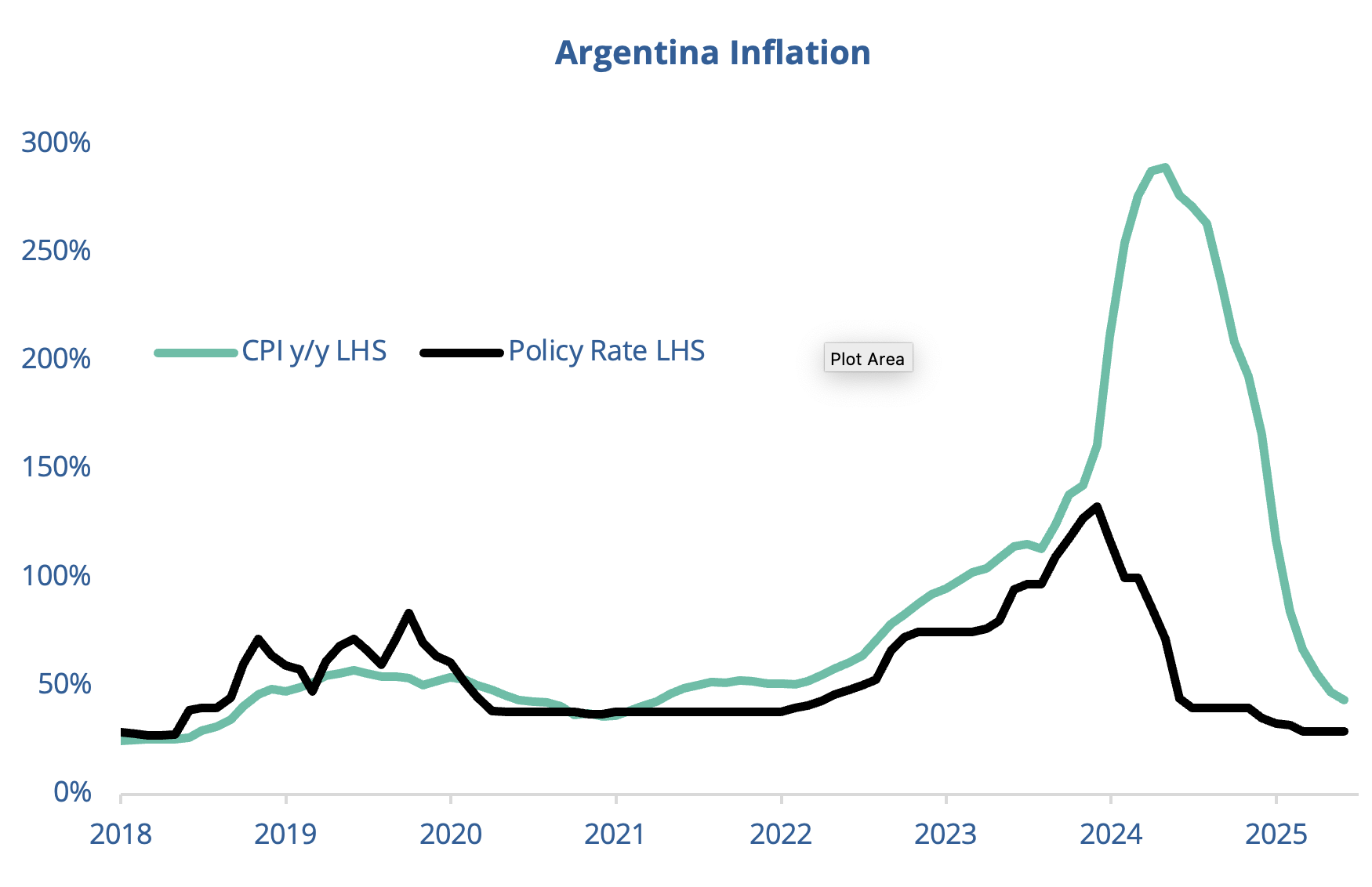

Argentina continues to make steady progress on the path to liberalizing its economy. Disinflation is ongoing (+43.5% year-on-year in May 2025 compared to +292% in April 2024). Growth is also present for the third consecutive quarter: +0.8% quarter-on-quarter in Q1 2025. A sign of Argentina's strong economic momentum, the IMF has revised its 2025 growth forecast upwards from 5% to 5.5%, despite a gloomy global context marked by trade wars. Fiscal and external balances continue to stabilize. A notable event in the first quarter was the reversal in the poverty rate. President Milei's "chainsaw policy" initially led to an increase in poverty from 40% to nearly 53% in the first half of 2024 (poverty defined by the national statistics institute as the ability to purchase a basket of necessary goods). According to Indec, the national statistics institute, it fell to 38.1% in Q1 2025, mainly due to the rapid decrease in inflation and the rise in real incomes. It is often forgotten, but inflation is a form of tax on the poorest. Any progress on this front contributes to the fight against poverty.

Source : SILEX, Factset, as of 04.07.2025

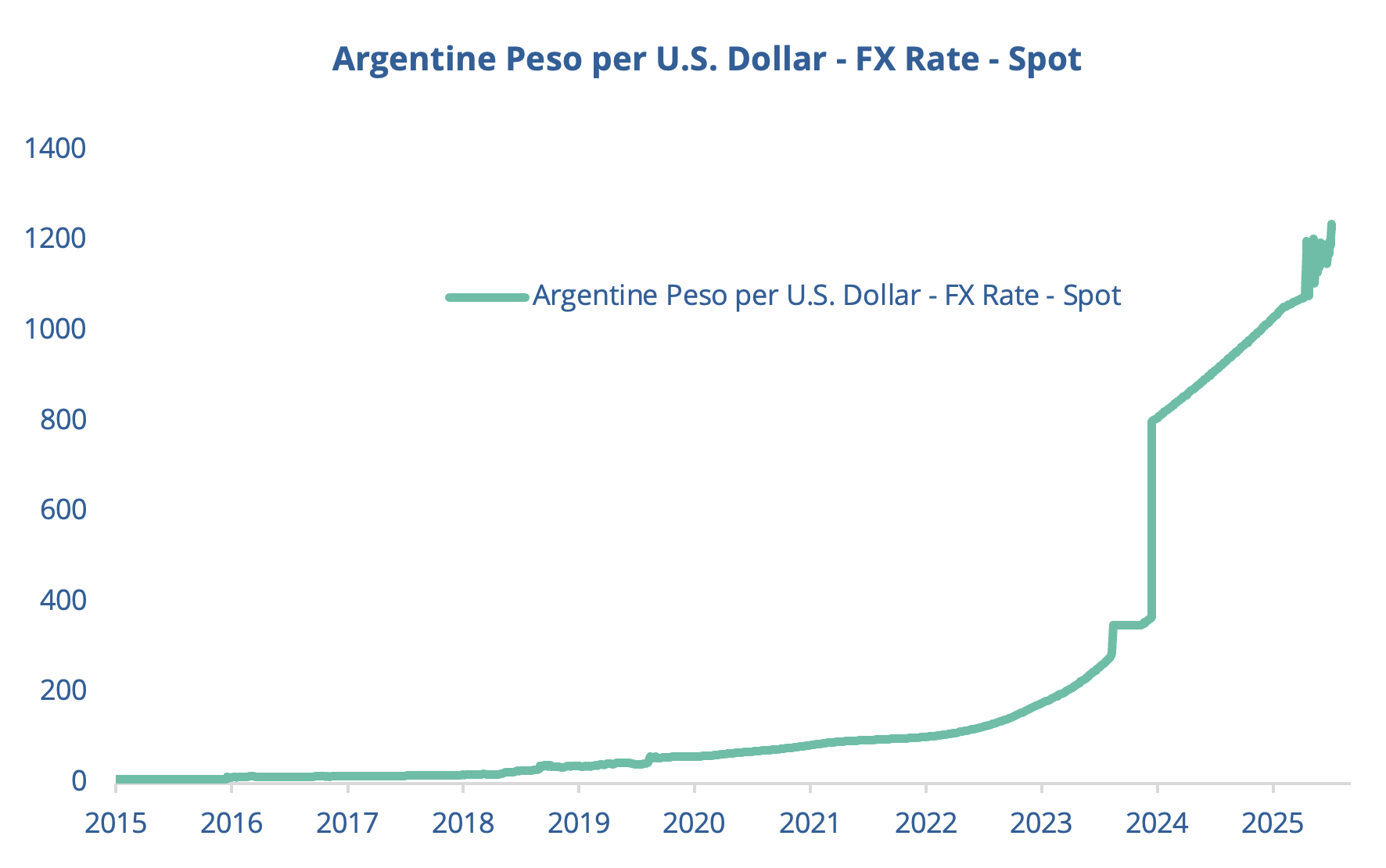

The most important event of the first half of the year was the end of a foreign exchange control regime that had been in place for most of the past 15 years. After managing the depreciation of the official exchange rate to bring it closer to the blue dollar rate, Argentine authorities allowed it to fluctuate between 1000 and 1400 per dollar since April 14. While many Cassandras predicted the failure of this policy, the trust capital built by the Milei administration over the past 18 months supports the peso, which is fluctuating in the middle of the range (USDARS at 1240 on July 4, 2025). Its credibility is reinforced by the support of the IMF, which granted Argentina an additional $20 billion, replenishing the central bank's foreign exchange reserves. Likewise, Javier Milei’s good relationship with the Trump administration is facilitating his negotiations with the Washington institution, while allowing Argentina to avoid attacks from the U.S. president—an exception in a world marked by trade wars. It should also be noted that Argentina had a trade deficit of just over $2 billion with the United States in 2024, which shields it from “reciprocal” tariffs.

Thus, one can see the Argentine glass as half-empty if one focuses on the levels of economic and financial indicators, or as half-full when considering the improvement in those same indicators. One illustration of this phenomenon lies in the sovereign default risk. Ten-year CDS (Credit Default Swaps) still reflect a 50% cumulative default probability over the next 10 years. But the trend shows the progress made, as the Argentine CDS spread has been divided by more than three since August 2024, with a downward trend that plateaued in Q1 2025 before resuming its decline following the lifting of currency controls in April 2025. On that occasion, Fitch upgraded Argentina's rating from CCC to CCC+. Even though the Argentine peso is expected to continue depreciating, progress on inflation is also reflected in the slower pace of depreciation, now around 20% per year against the dollar, a level similar to what is now priced in by currency futures. The last flare-up in early April corresponded to the "Liberation Day" on U.S. tariffs and reflected extreme investor pessimism about the economy and markets at that time. It had no direct link to the policies implemented in Argentina. Further progress on inflation should reduce pressure on the peso in the future.

Source : SILEX, Factset, as of 04.07.2025

Argentina's three defaults on its debt over the past 25 years (2001, 2014, and 2020) prevent it from accessing long-term financing. Government borrowing rates are only available for short-term maturities. In early July 2025, 3-, 6-, and 12-month yields are between 32% and 33%. This level does not offer a positive real return, with inflation still at 43.5%, making the investment unattractive even for an Argentine investor not exposed to exchange rate risk. However, an investor who believes that the risk of default is gradually decreasing could theoretically achieve a 10% dollar return over one year by buying a 12-month Argentine government bond and hedging the exchange rate risk on the futures market.

As Argentina's economic problems intensified, its stock market was progressively downgraded, moving from emerging market to frontier market in 2009, and eventually becoming a sort of pariah outside of any classification from 2021 due to capital controls. As such, Argentina is no longer part of any equity manager allocation grid. The recent lifting of capital controls should eventually lead index providers to revise their policies and make the Argentine market investable again for foreign investors. Its market capitalization is not negligible: about $135 billion.

Today, only the Global X MSCI Argentina ETF, ticker ARGT, remains to invest in the Argentine equity market. This ETF is fairly large, managing nearly $1 billion. Its investment universe differs somewhat from a pure index of peso-denominated stocks in Argentina. In fact, the ETF is listed in U.S. dollars and primarily invests via ADRs and U.S.-listed companies with significant exposure to the Argentine market. The fund's top holding is Mercado Libre, though its weight is capped at one-quarter at each index rebalancing. Mercado Libre is a company founded by Argentinians but headquartered in Uruguay, with its primary listing on the Nasdaq in the United States. The presence of Mercado Libre significantly alters the investment profile. Without it, Argentine equities would be 70% concentrated in three sectors (finance, utilities, and raw materials). This giant is often described as the Amazon/PayPal of Latin America, giving the ARGT index a high-growth profile, allowing it to post a positive return of over 50% in dollars over a rolling year. This point is very important, as it is common not to hedge currency risk when investing in equities, and the performance in pesos of the Argentine market has been very strong for over 10 years. The risk would have been a simple monetary illusion, which is not the case with this investment vehicle.

Source : SILEX, Factset, as of 04.07.2025

In terms of valuation, the Argentine market trades at about 14 times expected profits over the next 12 months, having generally benefited from better valuation since the second half of 2024. This valuation level is quite expensive compared to other emerging markets, but this premium also reflects the ongoing economic reforms and the presence of a unique growth stock in Latin America—Mercado Libre.

Source : SILEX, Factset, as of 04.07.2025

Investment Conclusion

The ongoing economic reforms are finally addressing hyperinflation and putting the Argentine economy back on the right track while reducing the risk of another default. Even though the Argentine peso is expected to continue depreciating, it is possible to lock in attractive bond yields over one year. The equity market remains uninvestable for most investors. The only remaining ETF on the Argentine market offers strong performance even in dollars, benefiting particularly from Mercado Libre’s strong growth momentum. Argentina once again offers investment opportunities in financial markets.