Autumn is knocking at our door. In our first weekly note after the summer break, we summarise the main takeaways and discuss the outlook.

Summer recap

- Fundamentally, the summer has been free of nasty surprises capable of derailing risk assets. The real bad news has been US tariffs on Switzerland and the renewed uncertainty due to French politics.

- Trump has stepped up his attacks on the Fed, but without any dramatic impacts on markets so far, probably as the Fed itself sounded more open to cutting rates, with inflation and employment data tending to back such a move.

- Tariff discussions continued to dominate headlines, with the EU failing to impress but securing a “manageable” deal, particularly compared to Switzerland. The fragile truce between the US and China seems to be holding.

- Consistent with the widespread frontrunning of tariffs and the resilient US economy, companies’ earnings have been mostly reassuring on both sides of the Atlantic, especially for US Big Techs. The Magnificent 7 are back to their relative peak and continue to report stratospheric figures. More importantly, corporates’ guidance hasn’t triggered significant earnings cuts, although “uncertainty” is mentioned by companies at a record level. Stoxx 600 EPS for 2026 has barely been cut since the end of June, despite forex and tariff headwinds. The S&P 500 EPS for 2026 has been revised upwards by 1%. The data is similar for the Topix and MSCI China (two of our key calls in our cross-asset allocation).

From a market perspective:

- As we hinted above, US data tends to back the possibility of a rate cut in September, with a weakening labour market and contained inflationary impact from tariffs so far. This was confirmed by Jay Powell at the Jackson Hole summit. However, there was no shocking data to indicate a sharp weakening of the US economy. “Soft landing” best defines the picture.

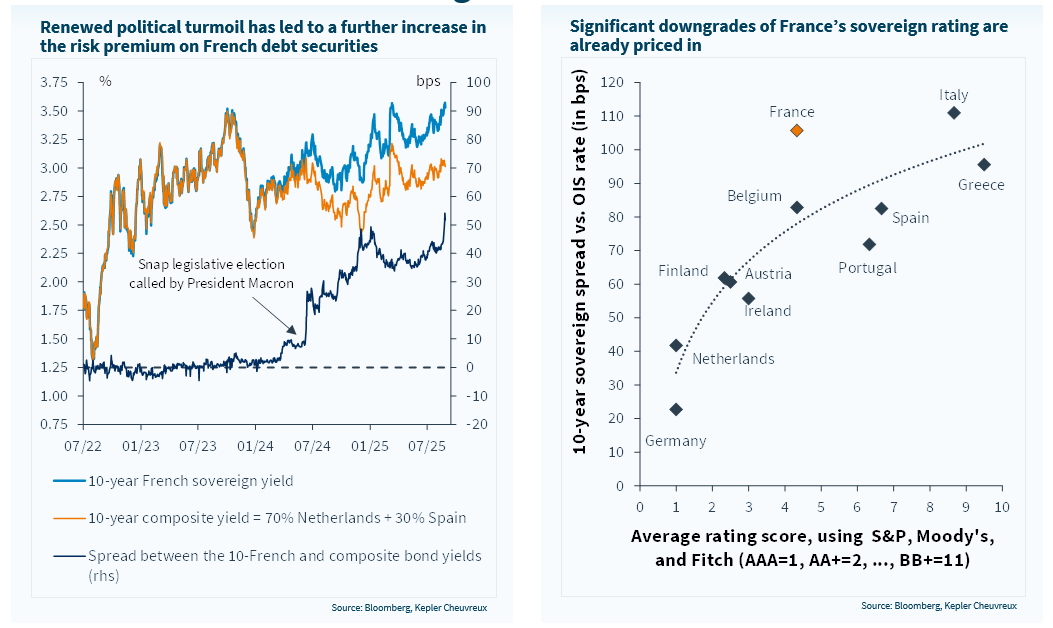

- Despite some 10bps fall in the US terminal rate, the US 10Y yield remained roughly flat at around 4.20% (our year-end target), suggesting continued risk aversion for long duration. Rate expectations and bond yields in Europe have barely moved. The French 10Y spread certainly moved up but remains in its post-2024 dissolution trading range. We note 30Y yields continued to trend higher almost everywhere but in the US.

- All of the above supported global equity markets, which performed well. Our diversification theme towards Asian equities (OW China / Japan) has paid off in Q3 as trade visibility with the US improved, and activity remained resilient.

- European equities (UW) have lagged, as the two largest equity markets (France and Germany) have been flat. German growth stocks have been pressured, and the incremental rally of German banking stocks wasn’t enough to offset the decline. European Value has outperformed Growth by 5 points so far this quarter, consistent with the upward pressure on long-term yields.

- It’s interesting to note that Ukraine ceasefire talks – a possible catalyst for renewed strength in Europe – made little progress, although Putin and Trump met. Europeans managed to convince Trump not to give in too easily to Putin’s requests and secured some US backing for a European peace enforcement mission that could be deployed in Ukraine. Meanwhile, the war rages on, and recent reports suggest Ukraine appears to be hurting the Russian supply of petroleum-refined products.

What’s coming?

- This week, US labour data will be closely watched to confirm the latest signs of a weakening labour market and confirm the likelihood of a September rate cut. We expect a 25 bp rate cut from the Fed on 17 September as the labour market weakness is contained by a shrinking labour force, stemming from Trump’s migration policy. Also, timing the potential inflation spike from tariffs has proven elusive so far because of inventories. These inventory effects will not last forever, and surveys continue to suggest companies will indeed increase prices.

- Another topic likely to be closely monitored is the French confidence vote on 8 September, along with expected rating downgrades. Two scenarios are possible: 1) Bayrou’s government falls (highly likely); or 2) Bayrou wins. In the first scenario, markets would face significant uncertainty amid coalition talks and snap elections. Our view had been that Bayrou would remain in office to handle the tricky work ahead of the presidential elections, basically functioning as a technical government. There is still a chance of that, but the odds now look low. In any case, French assets are already at a discount, and fundamentals aren’t that bad. With no political solution in sight, though, it is difficult to get excited.

- Market-wise, we have no reason to change our recent messages:

- In the very short term, the seasonal window for a pullback in equities (Neutral, cut from OW early August) isn’t closed yet, especially after a price performance this summer that was significant compared to earnings revisions, notably within AI. We downgraded Europe to UW in early August, and the latest developments in France are worse than we expected.

- Diversification remains a core theme, as we expect the dollar to resume its weakness from Q4 on the back of Trump’s policies.

- We are neutral on long-duration bonds due to a lack of alternatives, but OW cash (10%).

- Lastly, unless geopolitics unexpectedly derail fundamentals, we would expect another leg down in the oil price as oversupply should build up significantly from Q4. This could, on the other hand, ease the Fed’s job and support long duration.

French political uncertainty is once again taking centre stage