Trump and von der Leyen reportedly reached an asymmetrical trade agreement—like Japan’s—over the weekend. The trade negotiations leave a bitter aftertaste, as the US will impose a 15% trade tariff on most of the EU’s exports, including Autos and Pharma, while the EU will stay put. Also, the key EU nations have shown a clearly divided position. Macron has tried to push for a position of strength, while Germans and Italians, on the other hand, likely influenced by their big exporters, have sought to avoid confrontation.

- The initial market reaction is positive, as the trade deal increases visibility, but this outcome was largely priced in. In Japan, the initial market reaction was also positive when the trade deal was announced last week, but it appeared to fade rapidly.

- Markets can live with a 15% tariff rate, which basically involves a near status quo versus the situation which had been prevailing since April, when the 10% universal tariff was imposed by the US on every trade partner on top of existing duties.

- A 15% rate will still be a pretty significant headwind for European exporters on top of the euro appreciation (5% YOY but +10% YTD). Our stance on EU equities remains Neutral.

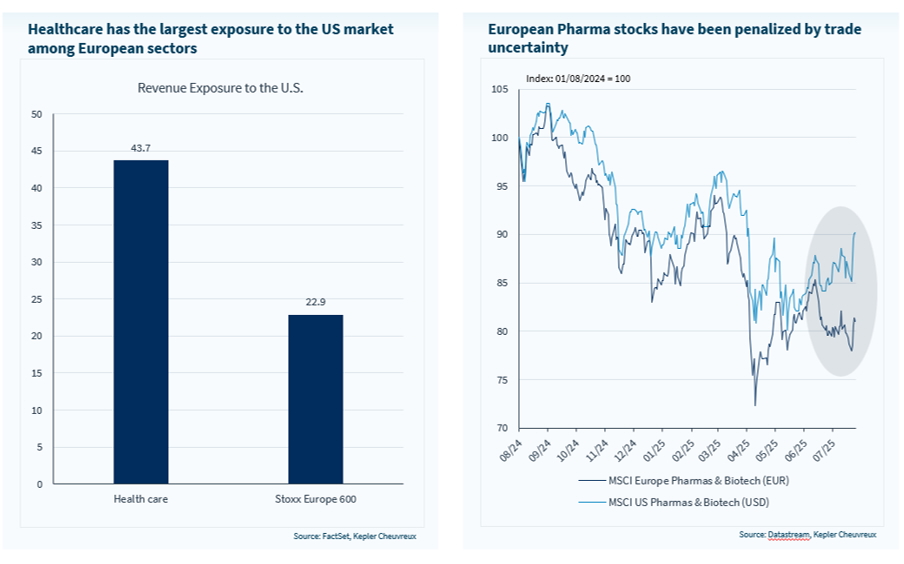

Although the details for healthcare are still pending, a reasonable EU/US trade deal could be a welcome piece of news for the pharma sector (Overweight). We explain why there is a buying opportunity in the sector. All the more if equity markets end up consolidating, as they often do in August with thin liquidity, their defensive characteristics and laggard status (i.e. attractive valuation) should both be welcome.

With regards to broader market developments:

- The global earnings picture stays supportive. With one-third of the companies listed in the S&P 500 having reported quarterly earnings for Q2 so far, the vast majority (83%) have released earnings above consensus expectations. The aggregate surprise stands near 7% (i.e. cumulated earnings vs. aggregate expectations in dollar terms for the 168 companies that reported). In Europe, 146 companies listed in the STOXX Europe 600 have reported earnings, and circa 60% have reported above expectations. In Euro terms, the aggregate surprise stands lower than in the US, at circa 3.5%.

- Sentiment on China stays upbeat. Despite rather weak economic fundamentals and rising barriers to trade from the EU as well, the market sentiment continues to improve on the back of ongoing US/ China trade negotiations. The equity market rebound, led by offshore stocks, lies on fragile ground but remains an attractive investment theme tactically. Longer term, the commitment of the authorities towards providing support remains key. Stimulus expectations have been disappointed so far, but the compromises on trade are a clear positive. We stay Overweight EM equities.

- Govies keep struggling. The ECB meeting last week was a tad more hawkish than expected, and the repricing of yields at the short end of the curve also pushed the long end higher. The inflation figures will be the ultimate driver of rate expectations. We believe that the strong Euro/ low energy couple will have lagging and negative effects on inflation in H2, leading to another rate cut from the ECB before year-end. The preliminary CPI for July that will be released next week will provide additional insights into the exchange rate pass-through. We keep preferring corporate credit vs. govies despite tight spreads.

Week ahead: in the US, watch the FOMC meeting (no rate cut expected), the job market reports (JOLT and NFP), the PCE inflation measure and ISM surveys for signs of growth resilience that would push risk assets higher. In the euro area, the July CPI will likely soften recent bond market concerns. The preliminary Q2 GDP will be released and is expected to show a stagnant economy after a rather strong Q1. In Japan, the BoJ will meet and discuss the timing of another rate hike. In China, the PMI business survey remains a market mover.

- On the earnings front, 163 companies in the S&P 500 will report quarterly earnings, including Microsoft, Meta Platforms (Facebook), Amazon, Apple, Boeing, Merck, United Health, ExxonMobil, and Chevron.

- In Europe, 171 companies in the STOXX Europe 600 will report quarterly earnings, of which L’Oreal, AstraZeneca, Airbus, Orange, Telefonica, Amundi, AXA, UBS, Barclays, HSBC, Intesa, Santander, BBVA, Societe generale, BMW, Mercedes-Benz, Renault, Stellantis, Adidas, BASF, Vinci, Bouygues, ACS, Saint Gobain, Hermes, GSK, Shell...

Trade deals (EU, CH) would help sentiment for this US-centric sector