The US elections are approaching fast and if there is one sure thing, it is that uncertainty is high… Trump now has a very small lead in every swing state, and markets have been increasingly pricing in a Trump win, with Treasury yields and the US dollar on the rise. Even in nationwide polls, the Harris lead has tightened dramatically. Kamala Harris is still likely to win the popular vote, but the candidate with the most votes can still lose the election, as the president is not chosen directly by the voters, but by an electoral college. This was the case when Hillary Clinton won the popular vote in 2016 but lost the election to Trump at that time.

Ahead of this milestone, and amid tensions in the Middle East and the earnings season, markets have been quite noisy and trendless. A good illustration of this is that a benchmark comprising some trend-following CTA strategies is down 4.5% in the past month and down 7% in the past three months (NEIXCTAT Index). The trend reversal in US rates is likely to be the main culprit for that.

In this context, we address the question of how to position portfolios ahead of the US election, from a cross-asset perspective. In our view, the US election is the tree that hides the forest. We believe that investors should focus on macro conditions and corporate fundamentals, which remain supportive, and forget the election uncertainty. On rates, the key question is whether a Trump victory, which is not a given, would necessarily cause a bond market selloff because his trade agenda is inflationary. Although there is potentially a huge gap between what he says and what he will do if elected, we recommend marginally reducing the duration of bond portfolios and keeping a slight long US dollar bias ahead of the event.

On US equities, we show in this report that election uncertainty is the tree that hides the forest. In effect, in the past 50 years (since the 1972 election), we note that the S&P 500 has experienced a significant rally in the aftermath of US elections, irrespective of the winner’s political party. For sure, 13 occurrences do not make a robust sample. But the recurrence of the pattern is eye-catching. The small number of outliers were 2000 and 2008, when US equities fell in the aftermath of the election, for exogeneous reasons. The 2020 election was also an outlier, but in a positive direction, since the vote took place a few days before Pfizer announced its Covid-19 vaccines, triggering a massive equity rally. Setting aside the election, both the buoyant economic momentum and the corporate earnings picture are tailwinds for the US market. Valuation is the big headwind for sure, which limits our risk appetite. But in the near term, the earnings season remains supportive. More than 180 companies in the S&P 500 have reported earnings as we go to press. The extent of positive earnings surprises remains elevated, and they are outpacing sales surprises, suggesting that margin pressures are contained compared to expectations.

In Europe, the macro picture is bleaker than in the US, and in this context, EUR rates have not tracked the upward trend in USD rates. We show in this report that the spread between USD and EUR rates has widened massively in the past few weeks, both at the short end and at the long end of the curve. In this context, we reiterate our call in favour of European equity sectors that would benefit from falling bond yields, notably bond proxy sectors. Real Estate (OW) has been somewhat under pressure lately, but Telcos (Strong OW) and Utilities (OW) have been more resilient. In the last couple of months, we have also started to upgrade some hard cyclical sectors that would gain from lower rates in the eurozone (Semis, Construction Materials, Travel & Leisure, all rated OW). We are more cautious on globally exposed sectors that could be vulnerable in the event of a new trade war (Autos UW, Cap Goods UW, Luxury N).

We also come back on the European earnings season. Overall, despite the gloominess in Europe, the earnings season has so far been slightly better than expected (earnings beat rate of 51%), especially for the Utilities, Financials, and Healthcare sectors.

Week ahead: a busy macro agenda in the US with a spate of data releases on the job market, including non-farm payrolls and unemployment for October, as well as the September JOLT survey. The Conference Board consumer confidence and the ISM manufacturing surveys will also be available, on top of the PCE price index. In the euro area, the first estimate of Q3 GDP will be released, as well as the preliminary October CPI. In Asia, the Bank of Japan will meet and is expected to stay put on rates. In China, PMIs will provide insights into the recent macro momentum, which is expected to have remained weak. On the corporate front, 172 companies in the S&P 500 will report earnings, including Ford Motor, Visa, PayPal, Mastercard, AMD, Intel, Alphabet, Meta Platforms, Microsoft, Amazon, Apple, Pfizer, Eli Lilly, Bristol-Myers, Cardinal Health, ExxonMobil, and Chevron. In Europe, 74 companies in the Stoxx Europe 600 will report earnings, including Novartis, ASM International, STMicroelectronics, Ferrovial, Lufthansa, easyJet, Airbus, HSBC, Standard Chartered, Société Générale, BNPP, UBS, Raiffeisen, Danske Bank, ING, Erste Group, Intesa Sanpaolo, Santander, BBVA, Banco Sabadell, CaixaBank, Amundi, Volkswagen, BASF, Maersk, AB InBev, BP, OMV, Shell, Repsol, TotalEnergies, and Technip Energies.

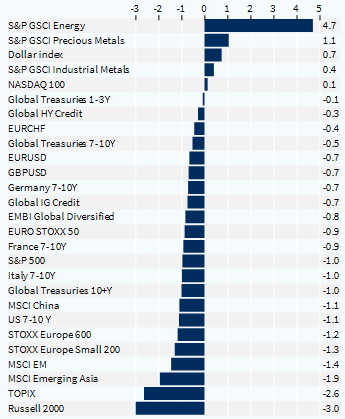

Cross-asset performance (last week, %)