This is our last weekly report of 2024. We thank you warmly for your support and interest throughout this year and wish you a relaxing break. As we head into the end of the year, it is the right time to take some perspective about past developments and our expectations going forward. We first take a look at the key highlights of 2024.

First, the resilience of the US economy in the face of high interest rates has remained remarkable. Despite some concerns about the rise in US unemployment earlier this year, household consumption remained strong and contributed largely to buoyant economic growth. This has been a key factor behind the performance of US equities in 2024, along with the AI/ Tech theme which remains alive. For the second year in a row, US equities have delivered spectacular returns, and the Trump re-election last month further reinforced this trend. Yet, as we show in the report, the valuation of US equities has richened further, to levels rarely seen in the past. Having in mind the trade wars and their adverse market impact in 2018, one key question for 2025 is whether Trump’s controversial agenda on trade can disrupt the equity bull run.

Second, in Asia, there has been some momentum building up in Chinese equities, especially in offshore stocks, after three consecutive years of double-digit losses. We have stayed on the sidelines on Chinese equities due to the complex domestic situation on real estate and consumer confidence, as well as global trade tensions that could disrupt the export-led growth model. We have rather preferred, and keep preferring, exposure to Japanese equities, that did well as the Yen depreciated further vs. USD and in a context where investors got lured by the name and shame regime to boost corporate profitability and valuations.

Third, Europe has lagged behind the US, EM and Japanese equity markets. The loss of competitiveness partly related to higher energy costs, political uncertainty in France and Germany, exposure to weak Chinese demand have all contributed to sub-par returns. Yet, it is important to separate the wheat from the chaff and some sectors discussed below are attractive for next year. We show in the report the contribution of earnings and multiples to sector performance this year. Despite their underperformance, it looks premature to us to turn aggressive on luxury and autos.

Fourth, it was again a challenging year for fixed income and the duration risk premium. Robust growth in the US kept pushing long term rates higher, especially around Trump’s election, despite the Fed rate cuts. In Europe, the landscape for fixed income investing was more supportive for investors due to weaker growth conditions. There has been a huge divergence in rates between the US and the euro area which may widen further in 2025. We keep preferring exposure to Italian govies for the carry and, surprisingly, for political stability and better growth conditions than in core euro area countries. In European credit, we remain positive on hybrid notes, subordinated financials and insurance Tier2 bonds. In US credit, we have reweighted High Yield vs Investment Grade, to leverage strong growth conditions (i.e. low default rates) while shortening bond duration.

Fifth, geopolitical tensions remained high, and it is unclear whether in 2025 they can really cool down. The complex relationship between Iran and Israel, as well as the nuclear ambitions of the former, have the potential to cause disruptions in oil markets. Oil fundamentals remain bearish however due to excess supply vs. demand. It is also unclear whether the Ukraine/ Russia conflict will end. In our view, sanctions against Russia will remain for the years to come and Russian oil and gas will not flow into Europe before years.

Below we expose our expectations for the next year. Overall, we expect market conditions in the first half of 2025 to remain under the influence of Trump’s election, which has global ramifications. Trump brings risks and opportunities as his pro-business stance also comes with potential trade tariffs and migrant deportation which can reignite inflation and put the Fed rate cut cycle on mute. The rest of the world (Europe, Japan, China) will have to deal with the US on Trump’s term as he takes advantage of his bargaining power to impose concessions on trade. So far, our strategy has been to play the opportunity set now and to get prepared for some volatility later in 2025, potentially as early as Q2 or H2, when he will move forward with its controversial agenda. Below, we put together six key calls for 2025, though they are not written in stone. Trump being highly unpredictable will require a lot of flexibility in managing portfolios in our view.

#1: Expect higher volatility in US equities as Trump comes with risks on the back of a controversial trade agenda.

- Buy protection while it’s cheap, while staying long US equities

- Stay long US banks, autos, consumer discretionary

#2: Long European equity sectors exposed to the US: travel & leisure, medias, health care. The European equity market incorporates global companies that have the potential to leverage stronger growth conditions in the US. The above-mentioned sectors are the most exposed to the US in terms of revenues and profits. While media and travel & leisure are linked to consumers, health care has experienced some turbulence around RFK Jr.’s nomination as Secretary of Health. Yet, he is quite controversial and looks unlikely to be confirmed by the Senate, which would eventually prove supportive for the sector.

#3: Expect softer budget constraints in Germany to fund infrastructure spending (OW construction materials in Europe). Germany will hold federal elections in late February. Depressed economic conditions call for fiscal stimulus and infrastructure is in our view the segment which may benefit the most.

#4: Manage bond duration risk with US high yield to leverage buoyant economic conditions in the US (i.e. low default rates). In bonds we keep preferring exposure to the credit than the duration risk premiums in light of Trump’s potentially inflationary agenda.

#5: Stay long Italy in EGBs for the carry and the dovish bias of the ECB. We expect borrowing costs in the euro area to keep falling in 2025, with the ECB deposit rate expected at 2% by end-2025. Italy delivers a higher carry than other EGBs but also involves higher credit risk with public debt near 140% of GDP. Political stability under Meloni is a positive but growth has decelerated and reducing deficits could become more challenging under such conditions.

#6: Overweight hybrid notes, subordinated financials and insurance Tier2 bonds in European credit. These market segments are riskier than investment grade credit and are an alternative to high yield, which they consistently outperformed in recent quarters. Insurance Tier2 bonds are somewhat exotic but benefit from the sector’s inherent credit strength, with an average solid rating of A3/BAA1 for the notes, and the strong demand for longer-duration bonds. Corporate hybrid bonds also remain attractive, with the extension risk still low, combined with a market environment that is expected to remain supportive for further issuance and refinancing activity.

Week ahead: The FOMC meeting along with a new set of macro forecasts and a new guidance on rates (the “dot plot”) will be the key market event of the week. Still in the US, retail sales will be available, as well as industrial production (both for November). In major economies, preliminary PMI business surveys for December will be available, though they have lost some relevance in recent years. In Germany, the IFO business survey will be released as an alternative measure of business sentiment compared to the PMI. In the UK, the CPI will be available, and the BoE is expected to stay put. In Japan, the BoJ blows hot and cold and looks increasingly unlikely to hike.

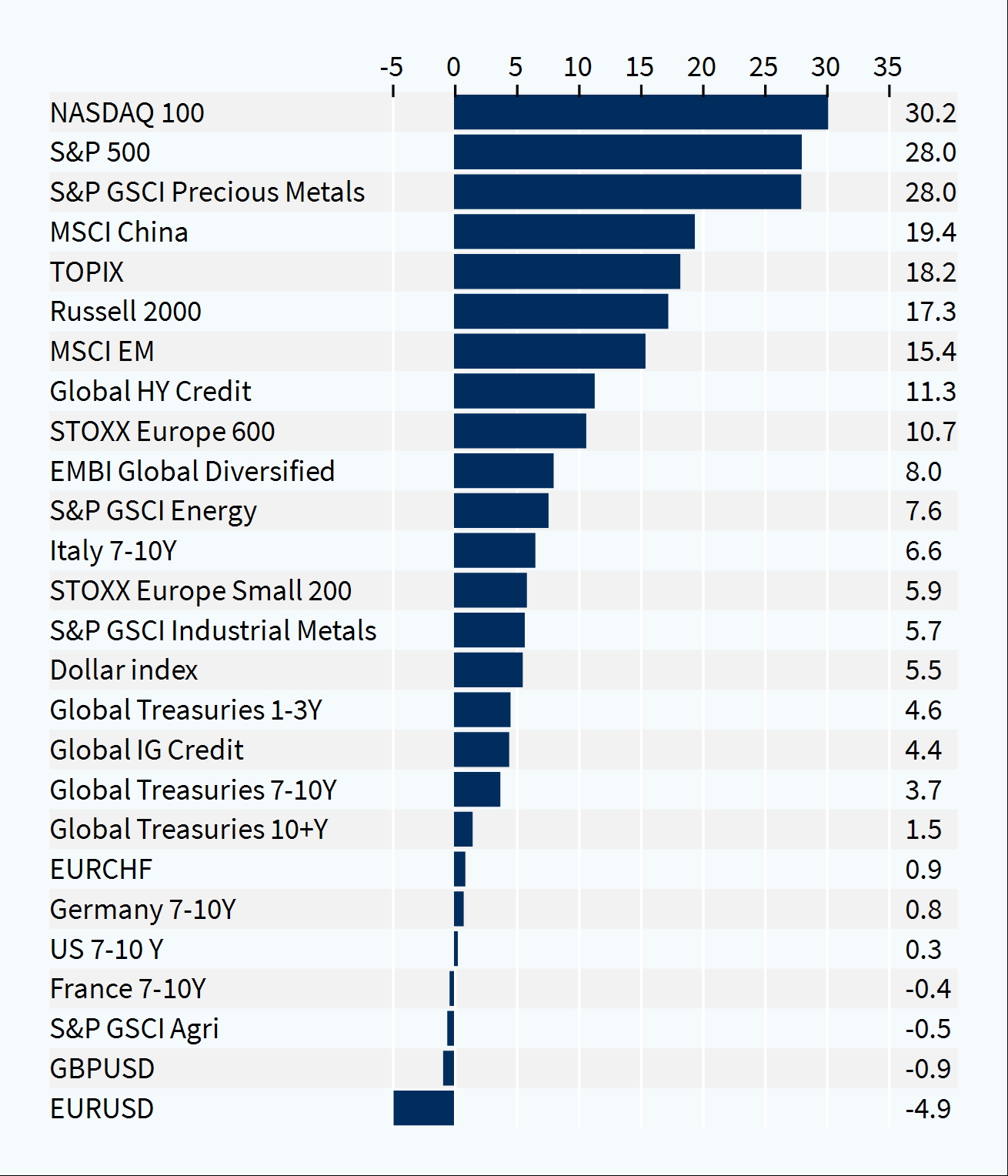

Cross-asset performance (last week, %)