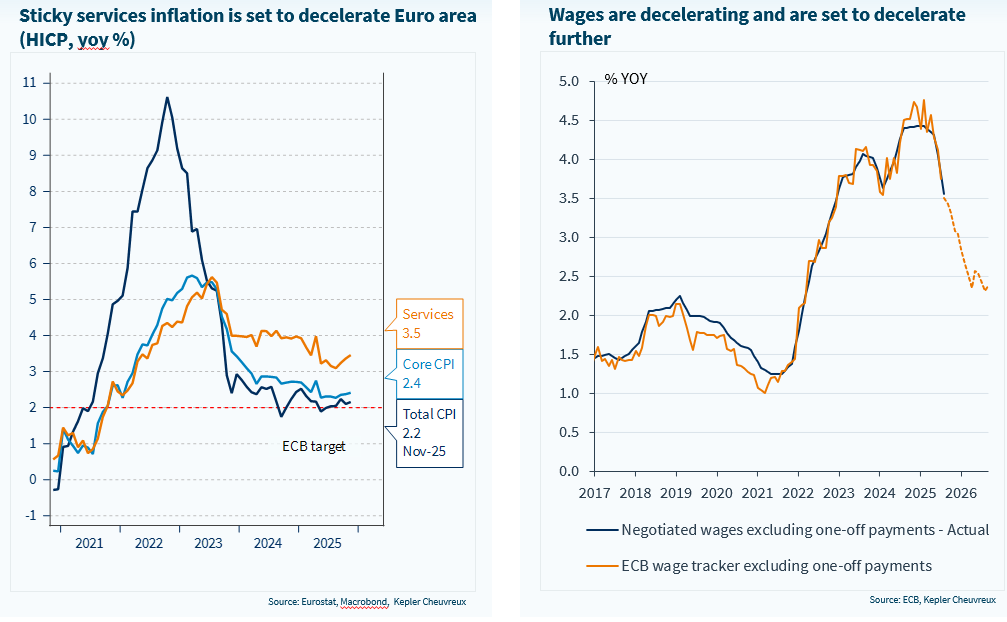

In our view, the sharp fall in oil prices and the strong euro appreciation in 2025 will have negative implications for inflation next year. Also, services could be the next shoe to drop. The CPI services, which represents 45% of the total CPI in the euro area, is rising at a rate of 3.5%. However, there is substantial room for a deceleration, as labour cost growth is falling. Advances in AI adoption could also be disinflationary, as it reduces employees’ bargaining power. But this factor could take a bit longer to materialise. Who remembers labour shortage concerns in the post-Covid years? They are long gone. The other side of AI could be rising unemployment and, in fact, lowflation.

As we are right in the midst of year-end central bank meetings, we take the opportunity to focus on rates, and by extension on small caps, which are rate sensitive. We must admit that the recent European bond market correction has taken us by surprise. However, we continue to assume it is temporary and that the ECB monetary policy meeting on 18 December could be the opportunity for Lagarde to soothe bond markets.

Among the main causal factors, we note a widening gap between the communication of the ECB and the Fed, which managed to cut rates by 25bps last week. While Powell affirmed last week that rate hikes are not on the agenda, Isabel Schnabel, one of the most influential ECB governing board members and the most hawkish, floated the idea of future rate hikes. Their respective communication is influenced by their mandate: the Fed has a dual mandate and is bound to consider the weakening employment picture in the rate equation, while the ECB’s mandate is to focus essentially on the inflation target. But the outcome resulting from these institutional differences is problematic. Despite lower growth and no prospect of a substantial improvement soon, as well as lower inflation, the euro area has experienced a sharp rise in long-term yields this year, while they have fallen in the US.

We show in the report that the recent bond market correction has been driven predominantly by the increasingly hawkish attitude of the ECB. Shifting monetary policy expectations at the short end of the curve were amplified at the long end. However, this is unrelated to inflation expectations, which have barely changed. The market is taking the ECB’s current stance at face value and extrapolating a more hawkish reaction function into the medium term. Strictly speaking, the current ECB tone is aligned with its mandate (“we are in a good place because inflation is at the target level”). But what matters going forward is not where the CPI was in November, rather where it will be in 12 months’ time.

Another driver of the bond market correction in Europe may have been the shifting supply/ demand dynamics, as the Dutch pension reform is moving forward. A lower duration gap under a defined contribution regime would reduce demand at the very long end of the curve, and Dutch pension assets are just massive. Around EUR550bn of Dutch pension fund assets will be transferred to the new system as early as January 2026. Yet, sovereign issuers are also contemplating reducing supply at the very long end to adapt the duration of issuance programmes to match new demand features. We believe this factor is rather technical and should not change the mid-term picture.

What are the implications for SMID caps, which tend to be more sensitive to interest rates than large caps?

After a strong start to the year versus large caps, supported by their higher domestic exposure amid the German fiscal plan and trade-related tensions, SMID caps have since given back all of their outperformance. Interest rates remain a key driver of SMID-cap performance, and the segment has been clearly affected by the upward repricing of long-term bond yields this year. Their greater vulnerability to rising yields can be partly explained by their higher leverage than large caps (on average). Here, sector composition also plays a role: SMID caps have a significantly larger exposure to Real Estate, a sector particularly vulnerable to higher rates.

That said, interest rates are not the only factor behind their recent underperformance.

- The easing of trade-war concerns since the summer and the associated stabilisation of the EUR/USD have clearly benefited large caps, which tend to be more internationally exposed (ex: Healthcare).

- Moreover, Eurozone leading economic indicators for manufacturing have tended to soften somewhat in recent months, weighing more heavily on cyclical small caps.

In the near term, we would advocate a neutral stance on European SMID caps, as the underlying growth momentum in the region remains subdued and the bar looks high in Q1 for any ECB rate cut. The sectors we favour in our allocation also tend to carry a larger weight in large caps than in smaller caps (e.g. Healthcare, which we rate Strong OW).

Looking further ahead, our stance remains positive on SMID caps, which should benefit from a more supportive interest-rate environment in 2026 (we anticipate the 10-year Bund yield could fall to around 2.5% by year-end), as the window for some rate cuts could reopen later in H1. Finally, valuations remain highly attractive, with SMID-cap share prices lagging their earnings outperformance, and offering a favourable entry point for long-term investors.

Chart of the week