Key insights from our autumn conference with 220 corporates. Two dominant themes emerged throughout the conference: diversification and the French political situation, both for obvious reasons. European sovereignty was also a recurring topic (reach out to us for our recent thematic basket on this topic), with companies like steel giant ArcelorMittal calling for stronger support from the European Commission.

- Corporate visibility remains limited, but sentiment on the European macro backdrop – and particularly on France – suggests either a stabilisation compared to the first half of the year or a slight deterioration. Notably, Edenred (restaurant vouchers) and Accor (hospitality) expressed cautious views. Construction company Eiffage appeared optimistic on the German plan but cautioned that tenders are unlikely to come before H2 2026 or 2027. Meanwhile, companies in the luxury and beverages sectors reported no signs of recovery over the summer, especially in China and the US. Overall, investors seem to be looking to 2026 as the likely timeline for a meaningful recovery.

- In his keynote speech, Enrico Letta, author of the Single Market Report, stressed the importance of European nations working together to avoid missing business opportunities currently being captured by competitors like the US. Note that on the same day in Strasbourg, Ursula von der Leyen outlined a roadmap to 2028, aimed at incorporating Letta’s proposals, including deeper financial, telecom, and energy market integration. Lastly, 2027 presidential candidate Edouard Philippe expressed cautious optimism that the new prime minister may still succeed in getting through a budget, as French MPs gradually learn to work within a coalition framework.

One of the most unexpected equity market rallies in recent history. The recent rally in US equities reminds us of the 2023 and 2024 market rebound. At that time, investors were in a cautious mood, expecting the aggressive rate tightening by central banks to trigger a recession, which never occurred. In 2025, investors fear the adverse impact of trade wars on consumer and business confidence, which is becoming more apparent. But so far, this has failed to derail risk assets.

- The upcoming Fed rate cuts have lifted sentiment, and a popular belief is that risk assets rise in the months following a monetary easing cycle. We show in our report that this is not the case. First, there are not enough observations to draw such conclusions. And second, the Fed rate-cut cycles in the past thirty years were never followed by a sustainable market rally. When a growth slowdown takes shape, the central bank provides monetary accommodation, but investors tend to overestimate the central bank’s power to reverse the trend. The rate-cut cycle starting in early 2001 did not prevent the S&P 500 from falling by double-digits in the two years that followed. In September 2007, the start of the Fed rate-cut cycle failed to stop the S&P 500 from falling dramatically in 2008.

- Going forward, we continue to believe that risks are asymmetrical with the cooling of the US job market, while US equities are valued near multi-decade highs. Based on that, we turned Neutral equities in early August.

Looking East. As part of our willingness to diversify our exposure beyond the US and Europe, we have been advising to re-weight Asian equities. We revisit and reiterate this call here, reflected in our Overweight stance on Japan and China equities.

- In Japan, all bets are off regarding who will be the next Prime Minister. The LDP will need to pick a new party leader to replace Ishiba, and local media reported that the vote could happen in early October. The two main contenders are Sanae Takaichi and Shinjiro Koizumi. The former, who is apparently leading the opinion polls, has discussed her intention to run. If elected, she would be the first woman to lead the country. She supports loose fiscal policy and monetary easing. The JPY has experienced some weakness in recent days, as the likelihood that she will be elected has increased. Takaichi narrowly lost to Ishiba in a runoff in the LDP’s leadership race last year. Shinjiro Koizumi is the son of a former prime minister. He is seen as fairly hawkish on monetary and fiscal policy. If the probability that he wins rises, that would be bullish for bonds versus equities and would probably lead us to revisit our Overweight stance on Japanese equities.

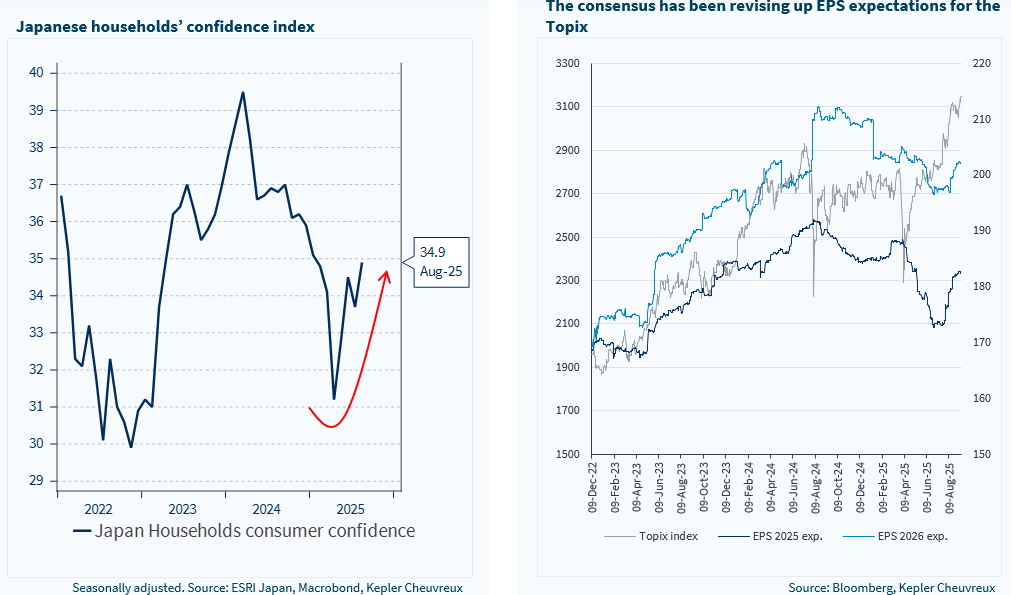

- Meanwhile, our stance on Japan has also been driven by better-than-expected economic figures and the likelihood that the BoJ will move very cautiously amid the current political turmoil. The OIS curve suggests one additional rate hike from the BoJ in the next six months, which looks likely, in our view. Inflation swaps suggest consumer prices will revert to the 2% target in the coming quarters. Earnings expectations have been revised up for the Topix in recent months, and consumer confidence is also rebounding.

- In China, our OW stance on equities that we will revisit in detail in upcoming reports has not been motivated by macro fundamentals. In fact, real estate indicators suggest renewed weakness, and this factor remains a critical headwind for consumer spending. Our positive view is instead related to the trade war de-escalation with the US, along with expectations of additional fiscal stimulus. In that regard, China is preparing to tackle the significant backlog of unpaid bills owed by local governments to the private sector. The arrears have been estimated to be as high as USD1trn.

European equities: revisiting bond proxies. Against this backdrop of asymmetric risk on US equities and rather weak European macro, we recommend seeking shelter in bond proxies, notably the inflation-protected ones. While Fed rate cuts expectations have already been adjusted significantly, rising odds of Trump’s control over the Fed would pressure real rates further. This is a process that could help “long duration” equities, notably those that have a capacity to defend their top line. Within these, we would favour the most domestic ones. We flag notably real estate, telcos, and utilities.

Week ahead: US retail sales and the FOMC meeting will be the key market movers. The Fed is widely expected to restart its rate-cut cycle, on pause since the end of 2024, with a 25bp rate cut. In Japan, the nationwide CPI will be released on the same day as the BoJ meeting on 19 September. We don’t expect the BoJ to hike rates amid the current political turmoil. In the UK, the August CPI will be released the day before the BoE meeting (no change expected).

Ishiba’s resignation, potential end of the BoJ rate hike, visibility on trade with the US, and higher consumer confidence are supportive for corporate earnings