A more volatile market setting, and this is not a bad thing. After hitting record highs in late October, US and European equities have faced downward pressure. VIX futures spiked as investors grew cautious about AI and Tech valuations.

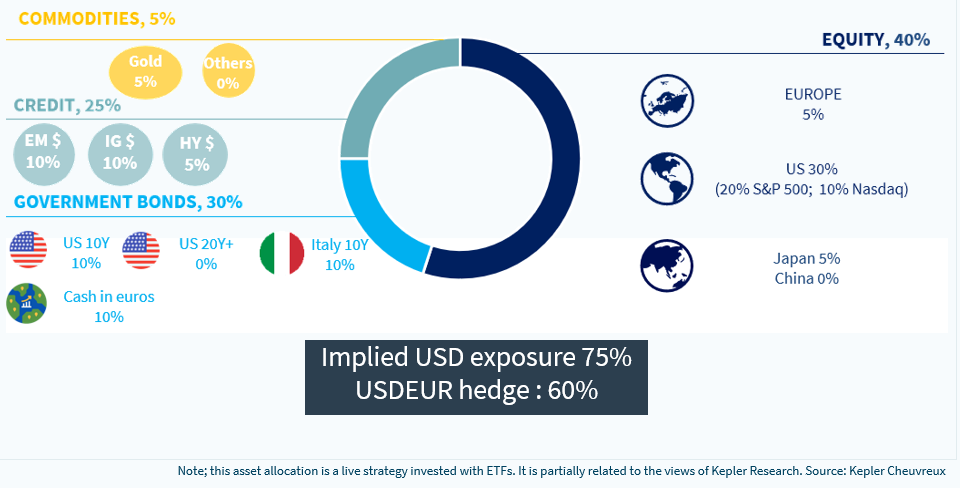

- Globally, the most volatile segments—Chinese equities and Nasdaq—saw the sharpest retracement last week, while bond yields declined. As expected in risk-off conditions, the US dollar rebounded. This aligns with our asset allocation view (see slide 6), and we are currently reassessing our defensive stance following the pullback.

- Last week, Nvidia’s quarterly earnings wrapped up the US earnings season, and the very bullish words of Jensen Huang fell flat as an initial market rally stalled. According to Huang, “we have entered the virtuous cycle of AI (…). AI is going everywhere, doing everything, all at once”. Obviously, you don’t expect a bearish message from the key semiconductor player in the world. But the accompanying numbers are impressive. Both Nvidia’s revenues and net income grew in excess of 60% in Q3. For the overall US tech sector, Q3-25 earnings grew 28% YOY! We show in the report that the combined annual revenues of the Mag 7, despite Tesla’s current difficulties, are now equivalent to Italy’s nominal GDP ($ 2400bn)! Although there are winners and losers (watch credit risks and Oracle’s jumping CDS spread), it is hard to argue that this is a bubble and that the market is not doing its job of separating the wheat from the chaff.

- Going forward, beyond Tech, we expect further upside on pharma and banks in the US, and a potential for recovery in consumer discretionary.

The end of the government shutdown offers some clues on the US growth momentum. The September job market report released last week did not provide an updated picture of the US economy. But in the absence of more recent numbers, what we saw was rather reassuring. Job creation jumped to 120k (although there were negative revisions for the previous month), and the most recent initial jobless claims figures suggest these trends have remained in place in the past two months. Unemployment kept rising, however, to 4.4%. We thus see room for a Fed rate cut at the December FOMC meeting, which would contribute to reassure markets.

A primer on the cryptocurrency selloff. We dig into the crypto sell-off and find that it remains broadly isolated. While Crypto ETFs have experienced significant inflows in 2025, it appears that the bulk of the investor base is retail. Hence, broader financial market implications appear contained. We show in the report that cryptos are by nature volatile and risky. In 2022, amid central bank rate hikes, the space experienced a 70% drawdown, before rebounding impressively in 2024 on hopes that Trump would boost the crypto legitimacy. The 30-40% current drawdown falls thus within the norm for an asset that is at least three times more volatile than equities. In short, someone is feeling the pain, but this is not translating into forced asset sales elsewhere.

European themes: we provide a performance update of our Ukraine reconstruction equity basket, composed of 15 companies from Western Europe. Earlier in February 2025, we launched this basket amid rising expectations of conflict resolution under Trump’s mandate. It looks like the probability has increased in the past few days, although the final terms of any peace deal are not yet known. Our strategy is up 14% since launch, versus 2% for the STOXX 600 Europe.

Sharpe 1 multi-asset: we reinforced bonds in early Nov and are currently reassessing our defensive positioning after the pullback