It’s been nearly a year since President Macron dissolved parliament, plunging France into political uncertainty with no clear majority emerging. What’s the situation now – and which investment opportunities in France? We’re regularly asked this, as France remains one of Europe’s key tail risks in the eyes of many investors, much like Italy once was.

Investors’ caution is understandable. France faces a tough fiscal path, with a EUR40bn deficit reduction target for 2026 but no clear political consensus to deliver it.

Three broad scenarios lie ahead:

- Base case: The current government, led by center-right PM Bayrou, survives the 2026 budget vote in the autumn, with no party having a strategic interest in returning to the polls before the 2027 presidential election. A mix of spending cuts and tax hikes should be announced today on 15 July, followed by a public debate over the summer and a parliamentary vote in early October.

- Government collapse: The budget fails to be passed, triggering a no-confidence vote. Macron could attempt to form a new government – unlikely – or call fresh general elections. As a reminder, he had to wait a year after the last dissolution.

- Presidential resignation: Macron could resign, triggering early presidential and legislative elections. This is unlikely given his continued focus on foreign policy and military leadership.

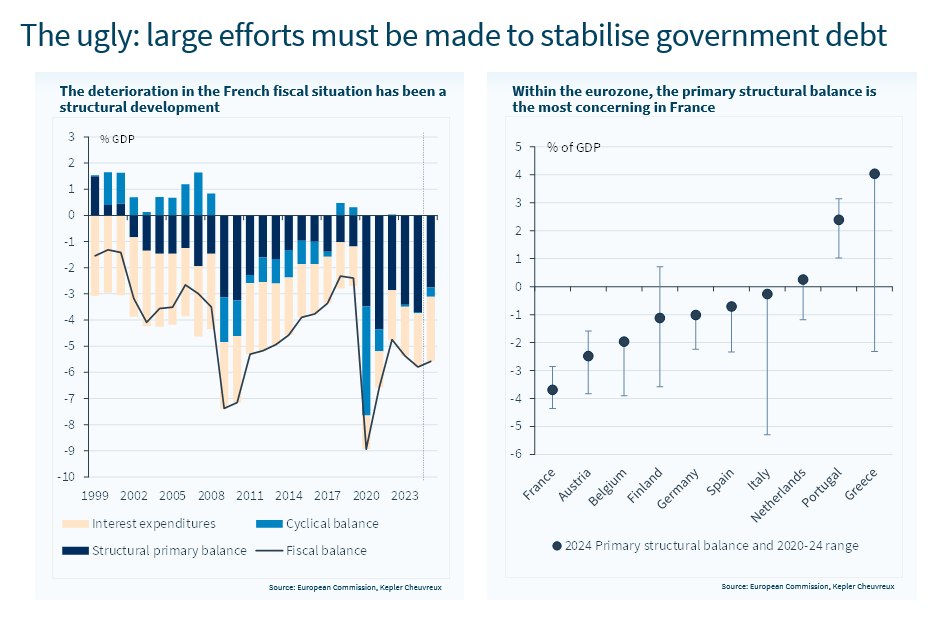

The fiscal situation is highly challenging :

- The fragmented parliament offers little scope for stable coalitions. Bayrou’s government survived the 2025 budget thanks to broad reluctance to trigger another crisis after Barnier’s fall, leading to a tax-heavy budget – including a supposedly temporary 35% corporate tax rate for large firms. Recently, the far right backed the government during a left-wing challenge over pension reform. This fragile balance may not be sustained, as the EUR40bn 2026 deficit reduction target – part of a broader long-term EUR100bn adjustment plan – demands painful decisions.

- Also, the government is supposed to provide a roadmap until 2029. But with defence and interest costs set to rise by about EUR30bn respectively by 2029, the challenge is significant.

- Politically, there are tough choices: the wealthy are heavily taxed already, while middle-income households remain unsatisfied with their purchasing power. Squeezing the elderly is not easy either, as they account for most of the traditional parties’ voters.

- Meanwhile, the French economic outlook is weakening, though not alarmingly so.

Against this backdrop:

- French bonds are already trading at spreads that imply significant credit risk deterioration.

- The French economy has limited trade war exposure on a relative basis, similar to the UK.

- The French current account is balanced, with high domestic savings.

- Structural reform space exists – if the political will returns.

- France retains unique leverage in Europe, with full nuclear and military sovereignty. A recent state study showed that its debt-to-GDP would be close to 100% had it spent as little on defence as Germany since 1995.

- Anecdotally, we believe equity investors’ sentiment is already pretty cautious on the French political risk.

Is there value in French assets?

- Fixed income: short-term spreads already price in political risks, and we note that the 5Y spread with the German bund trades as wide as the Italian spread, which looks pretty extreme. All in all, while we still favour Italian govies over French govies in our asset allocation, our base case on the political front is that Bayrou delivers, which would translate into a spread tightening.

- Equities: the CAC’s underperformance this year stems more from global market trends (trade war, FX) than political concerns. Its large caps are globally exposed, much like Sweden’s OMX or Switzerland’s SMI. Those indices could outperform if the dollar consolidates and trade deals are finalised under decent enough conditions.

- Within domestic sectors – banks, small caps, telecoms, and utilities – we see clearer signs of a political discount, especially in small caps, where we would look for stock-picking ideas. Within utilities and telecoms, Veolia (analyst rating: Buy) and Bouygues (analyst rating: Hold) screen particularly attractively.

Week ahead: US CPI & PPI, retail sales and July preliminary consumer sentiment from the University of Michigan. The Q2 earnings season will gather steam in the US and in Europe.