In this weekly report, we explore five key themes that, in our view, will shape market dynamics over the coming months.

The implications of trade tariffs on the global economy loom large (themes #1 to #3).

- But overall, it is increasingly apparent that the impact on US inflation (#1) is likely to remain limited and to a large extent offset by other factors such as services, housing and energy inflation, which are decelerating. The Fed Boston estimates that imported goods only represent 10% of US personal consumption expenditures.

- Yet, the impact of trade tariffs on economic uncertainty and job creation is becoming more apparent (#2). In the past three months, the US economy has barely created 30,000 jobs per month on average, down from 100,000 per month back in Q1-2025.

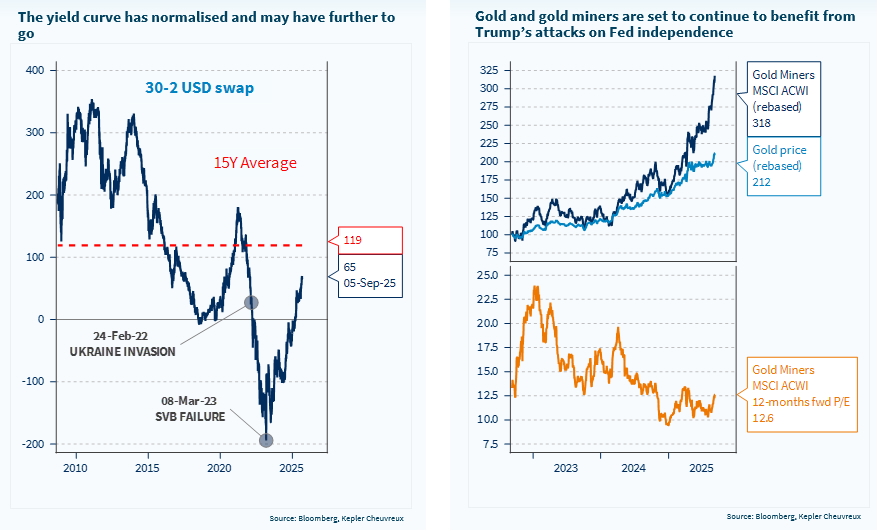

- Combined with recurrent attacks on the Fed's independence (#3), these factors should translate into significant Fed rate cuts in the coming quarters.

- To play these themes, we have been adding to bond duration in our multi-asset portfolio, hedging against further USD weakness, adding to gold and recommending curve steepeners in USD. The short end of the USD curve has been dragged lower by Fed rate cut expectations, while the long end has experienced selling pressure on the back of the lack of fiscal discipline in major developed markets. This is set to continue in our view.

Europe at the crossroads (theme #4). Coupled with excess savings, the new trade rules have us in cautious mode regarding European equities (Underweight). Earnings expectations for 2026 have been revised down, and the growth rate (+12% vs. 2025) looks optimistic. Yet, specific European thematics continue to outperform broad regional indices, such as our equity basket that aims at leveraging the German stimulus package.

- On the political front, France will hold a confidence vote today in Parliament, and Macron will be searching for a new Prime Minister before potentially calling snap elections later in Q4 if a moderate PM does not manage to gather a majority in Parliament. The discount on French assets appears to be significant, but as long as the political turmoil persists, the discount is unlikely to translate into outperformance. Within France, domestic stocks outperformed global stocks vulnerable to trade tensions since the beginning of 2025. But this trend has started to reverse, and this may continue as global stocks bring more protection against political uncertainty.

Looking for diversification in Asian equities and EM sovereign credit (theme #5).

- Ishiba’s resignation in Japan and the softening of inflation expectations are contributing to weakening the JPY, which is positive for Japan stocks. This is reinforcing the case for the asset class, which brings diversification vs. other developed markets.

- In China, our Overweight stance on equities is more related to the trade de-escalation with the US than local fundamentals, which remain weak, but at the same time, this calls for additional stimulus measures.

- Finally, EM sovereign credit in hard currency benefits from a weaker USD and also brings portfolio diversification. Spreads have tightened significantly, but the asset class yields more than 6.5%.

Week ahead: confidence vote in France (Monday), CPI/ PPI in the US and China (Wednesday), ECB meeting (Thursday), US Michigan preliminary consumer sentiment (Friday).

The weakening job market and the lack of fiscal discipline in the US may further fuel curve steepeners and precious metals