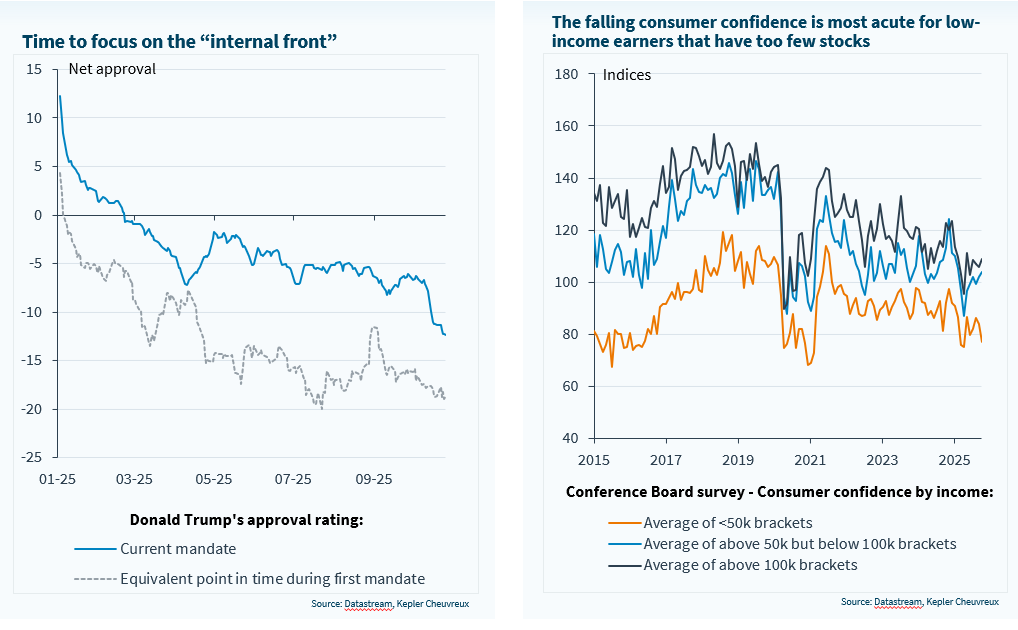

The affordability crisis among mass US consumers came back to bite Donald Trump in the recent elections that took place in New York, New Jersey, and Virginia. Without being overwhelmingly disastrous for the Republicans, according to commentators, the election outcomes showed that the Democrats have strong momentum ahead of the midterms in November 2026. In fact, the defeat led JD Vance to concede “we have to refocus on the internal front” on Twitter.

Since then, the administration seems to be brainstorming actively about how to address the K-shaped economy: lower tariffs on some grocery products, portability of mortgages, 50Y mortgages, and USD2,000 tariff dividends. On top of that chorus of ideas, Trump remains convinced that the Fed needs to help lower mortgage costs.

In aggregate, consumption shows no sign of strain, but lower-income groups have not enjoyed the wealth effects of the booming equity rally in the past three years. Although they capture only a small share of wealth creation, they represent a large voter base increasingly dissatisfied with Trump’s handling of the economy. His majority is increasingly at risk, and he remains mindful of his setback in the 2018 midterm elections.

Trump has not shown great interest in fiscal discipline during his presidential mandates, and credibility could be further dented by the idea of sending cheques to citizens. Although funded by the tariffs to compensate consumers for the hit from inflation, they would entail fiscal slippage that could reignite inflation and bond yields. We see the probability of this occurring rather low. But there will be some fiscal gifts in 2026. From an investment perspective, we bear in mind that a stimulated economy is more supportive of equities than bonds. But in the near term, we see the recent repricing in yields as an opportunity to lock in a higher carry as the US economy could eventually be showing signs of deceleration. Critically, the end of the shutdown will shed light on the job market and consumer spending trends in the coming days. Any weakness, as we expect, will rapidly reverse the trend in yields.

We show in the report that the recent rise in bond yields does not appear to reflect high inflation expectations and higher credit risks. Rather, it looks like the Fed’s stance, which has become a tad more hawkish than expected in October, had transmission effects across the yield curve. However, the Fed’s current stance will evolve pretty soon, with Powell leaving his role as chair of the FOMC in May, and Trump nominating his successor early next year.

The affordability issue is taking its toll on Trump’s popularity. Fiscal handouts on the horizon?