Amid continued weakness in US large caps and sharp rotations both across and within sectors driven by the AI scare trade, several positive signals are being overlooked by markets:

- Earnings season remains strong in the US (but weak in Europe). Q4 2025 EPS growth stands at 13% year-over-year for the S&P 500, compared to -1% for the STOXX Europe 600. US Tech earnings are growing at 30%. Yet Mag 7 stock prices have largely stalled since September last year, as shown in our report. The positive takeaway is that US large-cap valuations are easing, as strong earnings have not been accompanied by further market gains.

- We have been gradually downgrading US large caps in our multi-asset portfolio since December on valuation grounds and due to some fatigue in the Tech trade after years of outsized gains. At the same time, we upgraded and remain Overweight on US small caps, Japan, and EM (ex-China) equities.

- The US economy remains surprisingly resilient. Even the previously perceived weak spot, the labor market, appears firmer following the January jobs report. With improving employment data and a rising ISM index, we see potential for a recovery in manufacturing. Additional support comes from the “Big Beautiful Bill,” the sharp increase in digital infrastructure spending by Big Tech, and easing trade tariffs (agricultural products in Q4 2025, and potentially steel and aluminium in the near term). We also have greater confidence that corporate investment commitments from Asian countries, in exchange for lower tariffs, will materialize.

- The Eurozone economy is also proving more resilient than expected. Policymakers appear increasingly aware of the need to protect corporate profitability. Despite national differences, there is broad consensus across Europe on reforms to improve competitiveness. This should remain supportive for European equities (Neutral), although earnings momentum is less compelling than in the US.

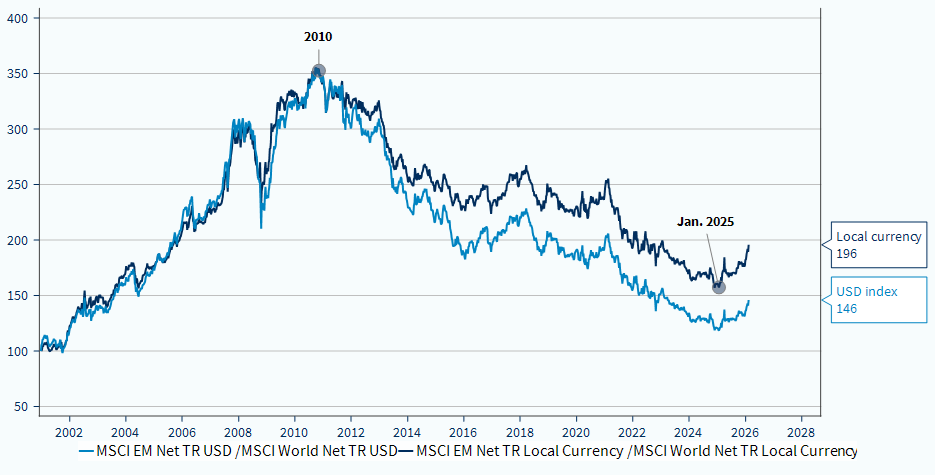

Overall, we maintain our preference for equities over bonds. In this report, we focus on reiterating our Overweight stance on EM ex-China equities for the following reasons.

- Strong growth dynamics. EM Asia economies (India, Vietnam, the Philippines, Indonesia, China, Malaysia) continue to grow faster than the rest of the world as part of the broader economic convergence process, whereby lower-income countries expand at a quicker pace.

- Supportive monetary backdrop. Emerging market central banks are in rate-cutting mode, broadly aligned with the Fed’s easing stance. Despite lower rates, EM currencies have strengthened against the USD, providing an additional source of performance.

- Broad-based equity outperformance. We expect EM performance to remain diversified: Latin America benefits from its commodity bias (upstream of the AI value chain), EM Asia from exposure to Tech and consumer electronics, and South Africa from gold miners.

- Latin America, and Brazil in particular, stand to gain from the commodity boom. Brazil could become a key player in rare earths, given its ample untapped deposits. According to the US Geological Survey, Brazil holds the world’s second-largest rare earth reserves, representing 23% of global reserves. While China currently dominates the sector - controlling around 60% of global extraction and more than 90% of processing capacity - Western countries are actively seeking alternative sources after Beijing restricted exports. The US and Europe are both pursuing agreements with Brazil on critical raw materials, with potential joint investments in lithium, nickel, and rare earths.

- India and China have lagged in recent months. India may have room to rebound, particularly if a trade deal with the US restores investor confidence. China, however, remains challenged by weak domestic consumption and a struggling real estate sector. The key question is whether additional policy support for housing will emerge after four years of downturn. Such a move would prompt us to reassess the Chinese equity market. For now, we remain Overweight EM ex-China equities.

- Attractive diversification benefits and valuation. EM equities currently exhibit relatively low correlation with developed markets. Latin America and South Africa remain appealing from a valuation perspective. Korea also appears attractively valued within EM Asia, despite its strong rally over the past twelve months.

The EM vs. DM trade in equities has scope to further outperform after 15 years of US dominance