The war between the US/Israel and Iran is entering its second week. Markets are increasingly concerned about the risk of oil and gas supply disruptions, as an extended closure of the Strait of Hormuz would have major repercussions for the global economy.

- European and Asian equity markets fell the most last week, as both regions are net energy importers. US equities proved more resilient, benefiting from energy self‑sufficiency and the technology bias of the benchmarks.

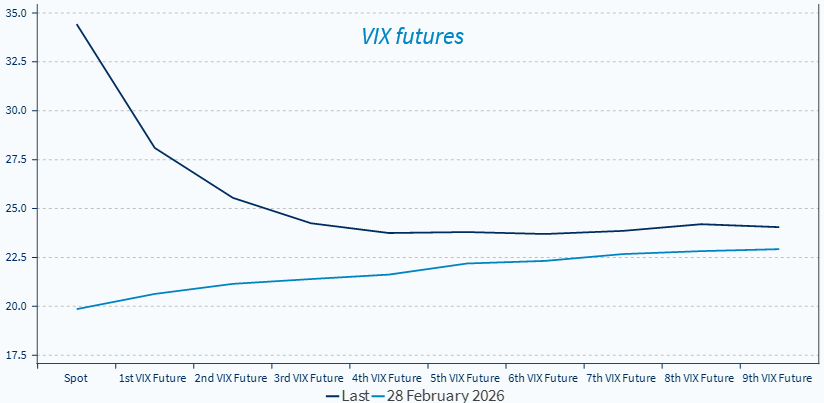

- Front‑end implied volatility has surged, but similar spikes have historically offered medium‑term opportunities. This is a war of choice rather than a war of necessity, and it could be halted quickly.

- The key question is the pain threshold required to stop it. In that context, the looming US midterms are an important constraint on Trump, as oil above $100/b threatens his majority.

What’s next? Geopolitical instability in the Middle East is not new, and financial markets have been able to cope with it without major and long-lasting implications in the past decades.

- The worst-case scenario for investors is the stagflation risk, like in the 70s. In this scenario, a major energy shock causes a simultaneous recession and surge in inflation, leaving investors exposed to losses on both their equity and bond holdings. Inflation-linked bonds, commodities, and the USD are the very few hedging options within this framework, on top of volatility arbitrage strategies.

- Yet global energy intensity is now much lower than in the 70s, and supply is also more diversified geographically. Although the Middle East is potentially more problematic than Russia from a global energy supply perspective, the fact that Iran is isolated is a positive.

- Overall, we do not expect the hostilities to escalate into a regional conflict. No one is standing by Iran to re-arm or fund it. But we don’t either expect Iran to give in to US demands. Every Iranian political leader in the past 50 years has grounded their ascent in anti-US rhetoric. The civilian protests a few weeks ago resulted in several thousand deaths. Hence, it is unlikely that a democratic leader (or moderate conservative) aligned with the US will emerge anytime soon. Iran’s choice of Khamenei’s son as supreme leader signals continuity of hardline policies.

In the short term, markets may remain unstable amid ongoing airstrikes. We therefore see no reason to add risk in portfolios. In fact, we moved to a long USD position earlier last week in order to take advantage of its safe-haven status and the fact that Fed rate cuts are being delayed due to renewed inflation uncertainty.

- Commodities and the US dollar remain effective hedges, although oil could experience sharp downside movements. The G7 is discussing the release of strategic reserves, which will not dramatically change the picture.

- Government bonds are losing their safe-haven status at present, due to the associated inflation risks.

- The US oil & gas equities theme remains relevant, as US investment and the revival of Venezuelan production have become all the more critical, though this will take time.

In the longer term, defence remains a structural theme, although it is richly valued based on conventional 12-month forward metrics. We also reaffirm our Overweight stance on low-volatility/defensive sectors such as utilities and telcos.

Can the situation get out of control? Beyond the implications for financial markets, there is a broader question that comes to our minds related to the so-called butterfly effect. We can trace the Russia-Ukraine conflict back to the Cold War and the Second World War. In the same vein, we can see the rise of populism and the far-right in Western democracies as a consequence of the Arab Spring in 2011 and the massive migration flows that followed.

- Iran is a country of 90 million people. As a side effect, the US/Israeli intervention could be sowing future chaos, the consequences of which are hard to predict at present. Iranian citizens and businesses have been pushed to the edge after decades of sanctions, weak economic growth, and high inflation. The latest turmoil could be the tipping point that will give rise to broader instability.

Front‑end implied volatility has jumped, usually offering medium‑term value