Beyond the summer turbulence in risk assets, the main development in recent weeks has been the resurgence of the Democrats in the US presidential race. In this report, we explore the market implications of such turnaround and find that small caps, the USD, and equity sectors such as Autos, Banks, and Tech have been negatively impacted by the Trump pullback. Energy, Industrials, and Healthcare appear less influenced by election polls. Yet, isolating the US-election effect on markets is challenging as recent moves were concomitant with the deterioration of labour market conditions. The pullback in commodity prices also makes it harder to establish the link between the performance of the energy sector and election polls.

Meanwhile, still in the US, the cooling of the labour market bodes well for the start of the monetary easing cycle next month and the associated curve steepener trade. As Powell said at Jackson Hole late last week, “the time has come for policy to adjust”. But there is no free lunch as Fed funds futures are pricing in 100bps of cumulative rate cuts by year-end, which would require a sharper deterioration in economic activity.

Actually, the risk of a US recession has increased but it remains relatively low in our view. Job openings are elevated, layoffs remain in check, and domestic consumption has been resilient. Monetary stimulus should help to find a new equilibrium and avoid a recession. Business surveys (PMI) continue to depict weakness in manufacturing, but business activity in services remains strong. The Q2 earnings season was well oriented, and no signs of recession emerged from earnings calls.

We are nonetheless back to square one. US equities are richly valued, China’s economy remains in the doldrums, and excess capacity in industry poses major challenges to European companies. The only positive side effect of China’s continued weakness has been the pullback of commodities, which contributes to the disinflation picture.

Below we lay out our main convictions for the near term. Considering the fact that September will be a critical milestone on the US election front, devising a midterm outlook at this stage is challenging. Kamala Harris will face major tests in the coming weeks: her first sit-down/ in-depth media interview by the end of the month and her first debate with Donald Trump (scheduled for 10 September). This will be critical to consolidate her momentum as it is reportedly not her main strength, and it could reignite the Trump candidacy.

Key call #1: Expect sector rotations as US election approaches critical milestones

- Small caps, the USD, Tech, Autos, and Banks vote Trump

- Kamala Harris to face first major tests in the first half of September

Key call #2: Favour defensive segments within European equities (Pharma, Utilities)

- In Europe, consumers remain cautious, and Chinese competition in industry weighs on earnings prospects across many sectors.

Key call #3: Caution on China, commodities, and European Luxury

- Visibility remains very limited in China due to a constantly adjusting real estate market, which undermines consumer confidence. No truce is in sight for trade wars, which are expected to escalate in the coming quarters.

Key call #4: Increase duration in Bond Portfolios

- The economic slowdown should continue to drive inflation toward central bank targets. Gradually extend bond duration in portfolios and avoid high-yield credit.

Key call #5: Hybrid and financial notes in European credit

- Hybrid notes offer attractive yields with moderate risk given the quality of issuers (investment grade). AT1 and bank Tier 2 also present notable appeal in terms of risk/reward.

Key call #6: Emerging market sovereign debt to play USD depreciation

- The Federal Reserve is expected to start cutting rates from September, which should contribute to dollar depreciation. Emerging market debt (in dollars) is an asset that should benefit from this.

Week ahead: US consumer sentiment (Aug.), PCE price index (July), Euro Area August CPI.

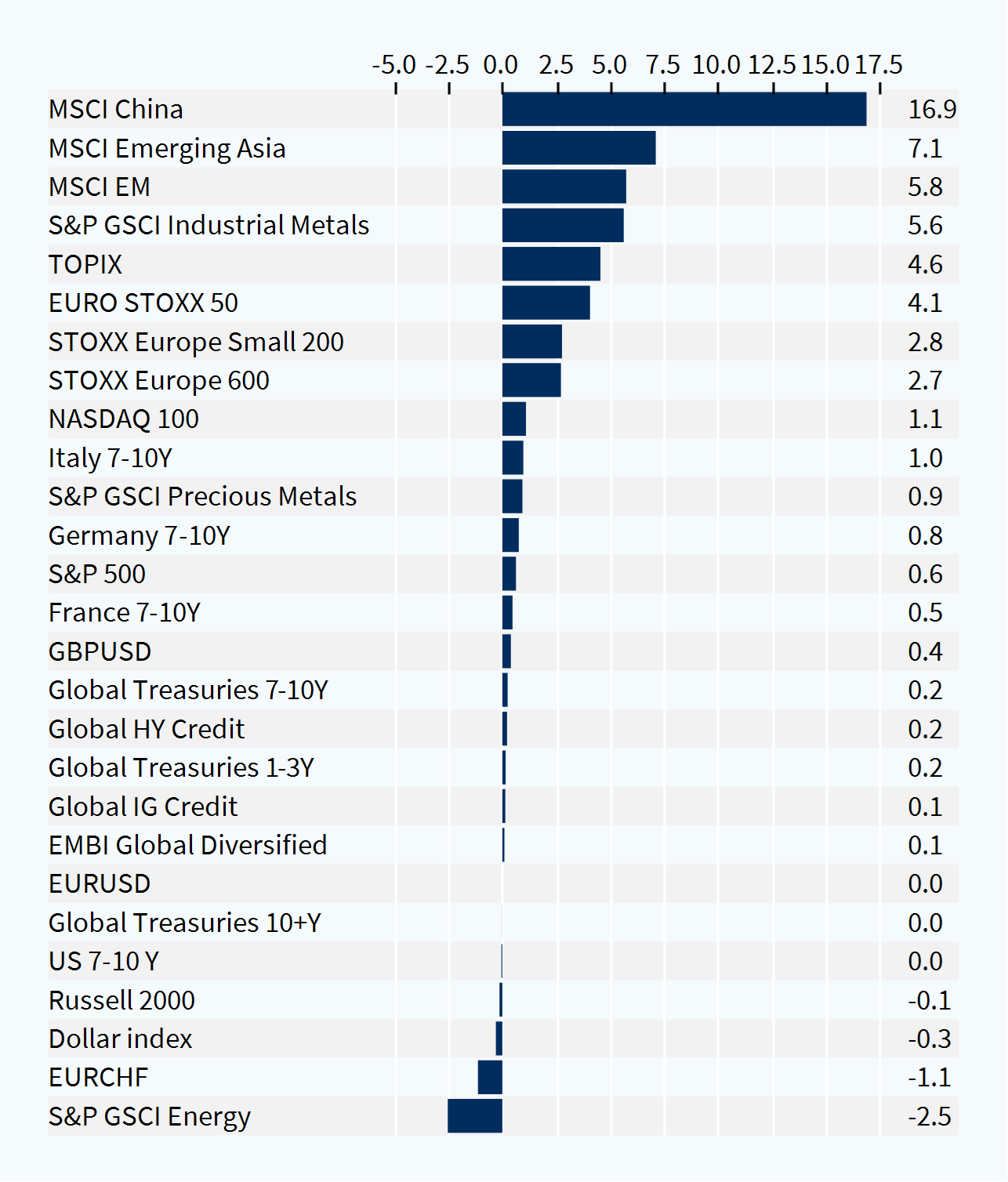

Cross-asset performance (last week, %)