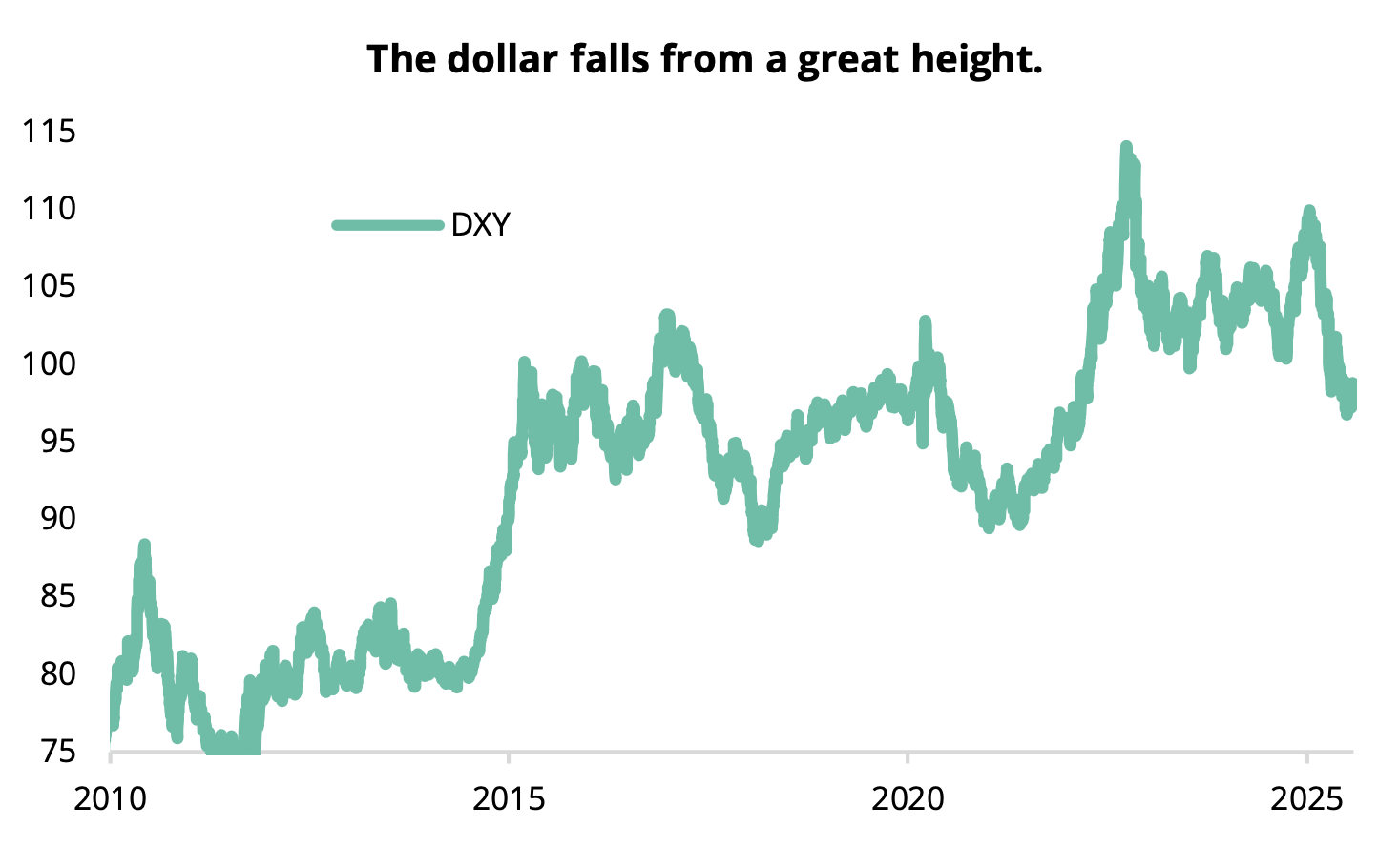

The dollar has experienced a turbulent 2025. After reaching record highs in January in the wake of Trump’s reelection, the greenback reversed sharply, to the point of experiencing its worst first half of a year since 1973, losing just over 10%.

Within our allocation, we had surfed the “Trump trade” to overweight the dollar from November 2024, a choice that paid off for two months. But starting in March, as downward pressure began to accumulate, we decided to neutralize the position. This proved insufficient, as an underweight would have been more appropriate given the sharp drop in early April. What lessons can we learn from the dollar’s rapid depreciation and what are the prospects for our tactical and strategic choices?

First, let’s review the factors driving the dollar’s decline. They are macroeconomic, but also political and technical. Second, we explain why we believe the dollar should stabilize by the end of 2025, before resuming a gradual depreciation, which remains the path of least resistance. Thus, we maintain our neutral stance and plan to move to underweight between the end of 2025 and the beginning of 2026.

1. The fall in the dollar exchange rate in the first half of 2025

“In economics, things take longer to happen than you think they will, and then they happen faster than you thought they could.” Rudiger Dornbusch, theorist of exchange rate overshooting.

Let’s start with some macroeconomic elements to set the scene. For the past ten years, the DXY index (representing the dollar’s nominal exchange rate against the United States’ main trading partners) has experienced a structural appreciation, driven by interest rate differentials and economic growth favorable to the American economy. The decade was marked by two periods of strong appreciation, sharing similar causes. First, between 2014 and 2015, growth made a big comeback while European countries continued to pay the price of the sovereign debt crisis. The Fed therefore began preparing for the end of QE from mid-2014 and to raise its rates at the end of 2015, while this same period marked the transition to negative rates and the major beginnings of QE in the eurozone. Then, between 2021 and 2022, the inflationary slippage caused by the post-Covid recovery forced the fed to quickly raise its rates by more than 500 basis points while growth remained well above that of other developed countries, against all expectations.

Sources: FactSet – data as of 30/07/2025

Past performance is no guarantee of future performance.

This “American exceptionalism” has also been reinforced throughout the last decade thanks to the advent of American technology giants, which have attracted capital to American stocks. Two other upward legs, more measured but attributable to Trump’s tariffs, can be identified: the first in 2018-2019, during Trump’s first trade war with China, the second at the heart of the “Trump trade” between mid-2024 and early 2025, that is, around Trump's re-election. These developments allow us to trace the genesis of the strength, and even overvaluation, of the greenback at the beginning of 2025.

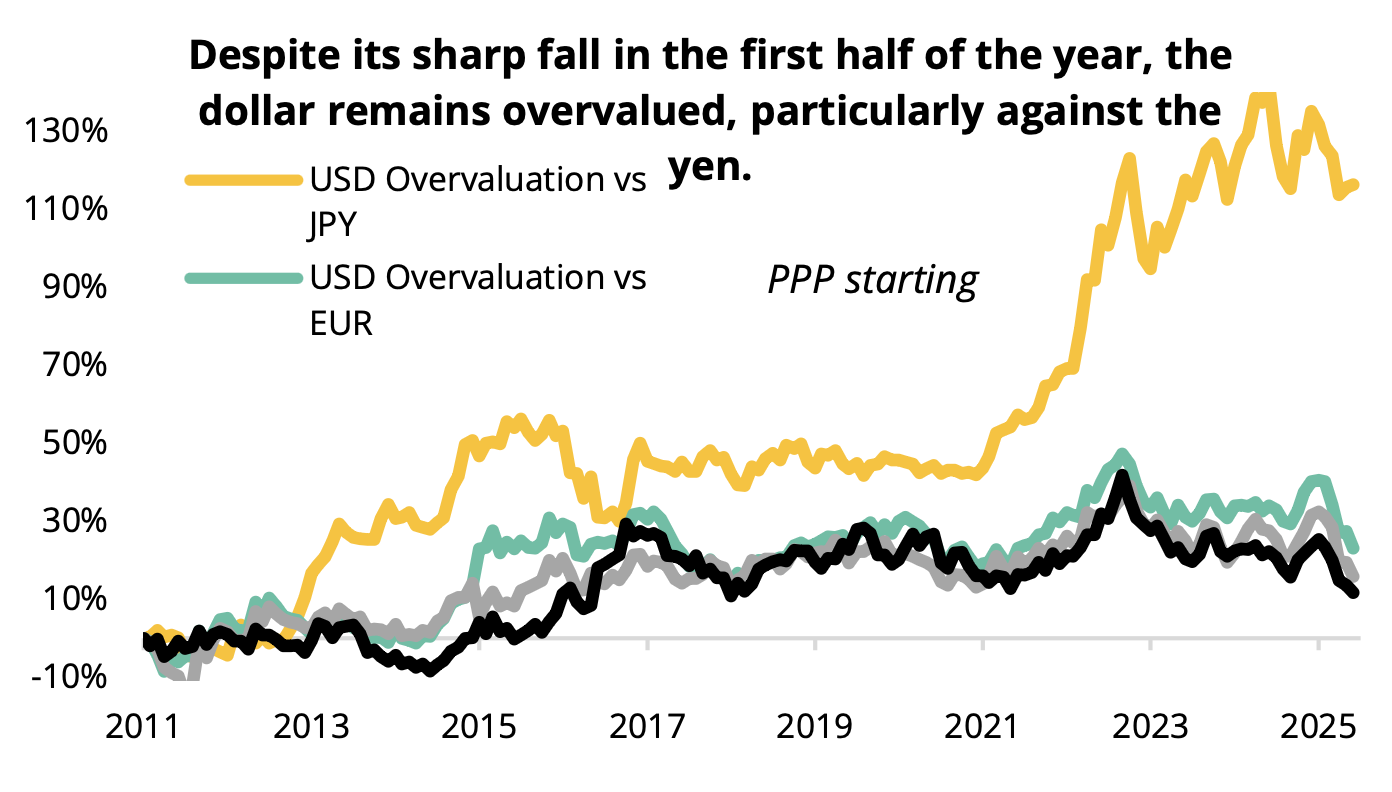

To quantify this overvaluation, we used the classic macroeconomic model of purchasing power parity. Like any model, it has the drawback of simplifying a multifactorial reality by focusing on inflation differences between countries. However, it remains a good guide over the long term. Starting our analysis in January 2011, at the end of the 2008 crisis, we observe an overvaluation of the dollar of 12% against the pound sterling, 16% against the Swiss franc, 23% against the euro... and 116% against the yen!

Sources: FactSet – data as of 30/07/2025

Past performance is no guarantee of future performance.

In the political sphere, the dollar’s surge has not gone unnoticed. Since his first term, Donald Trump has made no secret of his desire to weaken the overly strong dollar, which he associates with the deindustrialization of the United States. He also believes that the interventions of his trading partners on their exchange rates explain the weakness of their currencies against the greenback. As we discussed earlier, solid macroeconomic arguments have explained the dollar’s strength for years, without any manipulation being necessary. But the Trump administration is not known for its ability to accept macroeconomic realities, and it has set itself the goal of weakening the dollar. And it has been successful in this first half of 2025. One person has embodied this effort: Steve Miran.

President of the Council of Economic White House Advisors, he published in November 2024 an article entitled A User’s Guide to Restructuring the Global Trading System, a veritable economic policy manifesto for the Trump administration. While many of the findings are correct (particularly that global balance of payments imbalances are reaching worrying levels), the proposed solutions are enough to send shivers down the spines of investors.

Miran notably envisages levying “user fees” on holders of American debt, which would allow the American government to recover part of the coupons paid to foreign investors. In addition, he opens the door to “Mar-a-Lago Accords”, a reference to the Plaza Accords which had launched the depreciation of the dollar in the second half of the 1980s. At that time, the dollar’s collapse had been extremely violent (and painful for the United States’ partners, such as the Japanese, who have long seen the record appreciation of their currency as one of the causes of their lost decade from 1990 to 2000). Miran’s proposals therefore served as a reminder that “country risk” was not reserved for emerging countries and that violent movements in the world’s reserve currency could not be ruled out.

Donald Trump has also contributed to the dollar’s plunge. Since his first term, the US president has been in open conflict with Jerome Powell, the head of the Federal Reserve. The former has been demanding interest rate cuts from the latter. Although this has long since ceased to be the norm in developed countries, where the central bank must remain independent of the executive branch, Trump’s attacks on the Fed have exacerbated the dollar’s decline. And if Trump doesn’t “fire” Powell, investors are not forgetting that Powell’s term ends in May 2026, and the president will then be able to propose a replacement, perhaps more inclined to heed the White House’s directives. All of this has eroded investor confidence.

A final factor, of a technical nature, may explain the sharp correction of the greenback. It lies in the hedging strategies of foreign investors. Since the 2008 crisis, the overvaluation of the dollar has manifested itself in a permanent breach of the theory of covered interest rate parity. In other words, there is a cross-currency basis gap, which means that hedging dollar positions is more expensive than economic theory suggests.

In a context of structural appreciation in recent years, many investors have therefore chosen not to hedge. A study by the Bank for International Settlements ( US dollar’s slide in April 2025: the role of FX hedging ) shows how this backfired in early April 2025, when the deluge of tariffs announced by Trump revived fears of recession. As markets anticipated rapid rate cuts from the Fed, the dollar fell sharply. Investors then rushed to hedge, which accelerated the dollar’s decline. In short, they rushed to buy fire insurance when the house was already on fire. So it cost them dearly... and the dollar fell even further.

2. Medium-term support factors

a. The sentiment has become excessively negative

A first supporting factor comes from the intensity of the decline and the change in investor sentiment. The reversal on the dollar was particularly brutal. The consensus was very bullish on the dollar the day after the election of Donald Trump as President of the United States of America before becoming increasingly negative during 2025.

With more than a third of respondents bearish on the greenback in the last Bank of America survey in July 2025, we are close to an extreme level, often a sign of a turning point in a contrarian approach, especially since the speed of deterioration has been particularly strong. In other words, it is not the same to have more than a third of investors bearish on the dollar for many months and to reach this level in the space of a quarter.

b. The United States remains the world’s military hegemon

The reserve currency status conferring the exorbitant privilege that Valéry Giscard d’Estaing, then French Finance Minister in the 1960s, spoke of was not acquired overnight. Previously, the pound enjoyed this status while the British Empire dominated the world on land and sea. Since the second half of the 20th century, the United States has become the world’s policeman, being the leading military power. Its defense investments reach nearly $900 billion per year, or 38% of global spending. Including NATO’s spending, this bloc even accounts for more than half of defense spending.

The American administration is exerting increased pressure on its partners to spend more and aims to pass the $1 trillion mark. The bombing of Iran’s nuclear facilities last June was also a demonstration that the United States does not want to lose its status on the international stage. In these times of intense geopolitical tensions, investors have remembered that the dollar remains a safe haven.

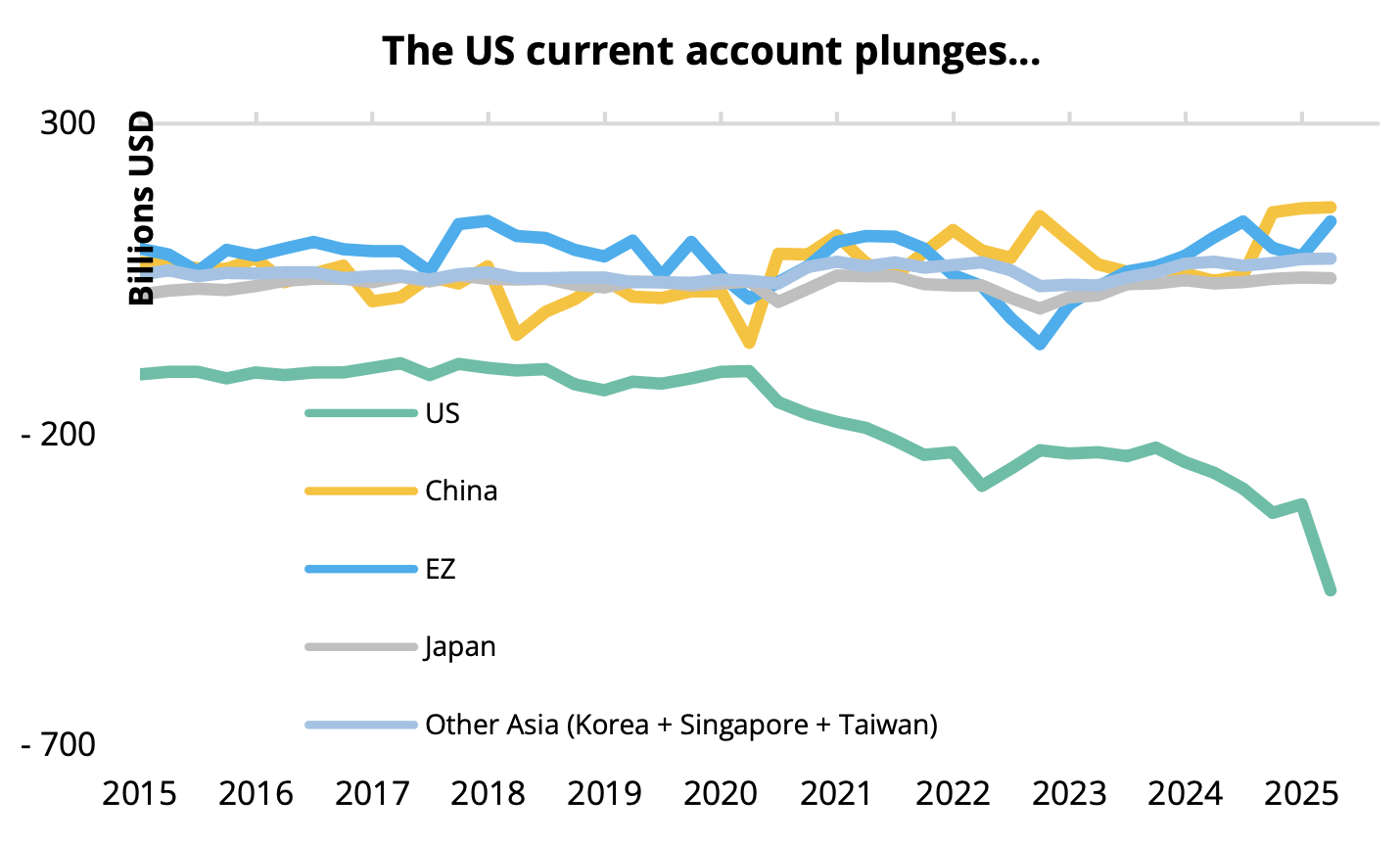

c. The current account deficit is not as huge as it seems

The monumental US current account deficit is often presented as a factor in the depreciation of the dollar. Indeed, US external deficits have been worsening rapidly over the past decade, while other geographic regions have accumulated symmetrical surpluses. As a result, global macroeconomic imbalances are mounting. The argument is that a falling dollar would be the safety valve that would allow the system to rebalance in the medium term. In theory, this is an advantage of floating exchange rates.

Sources: Silex, FactSet – data as of 30/07/2025

Past performance is no guarantee of future performance.

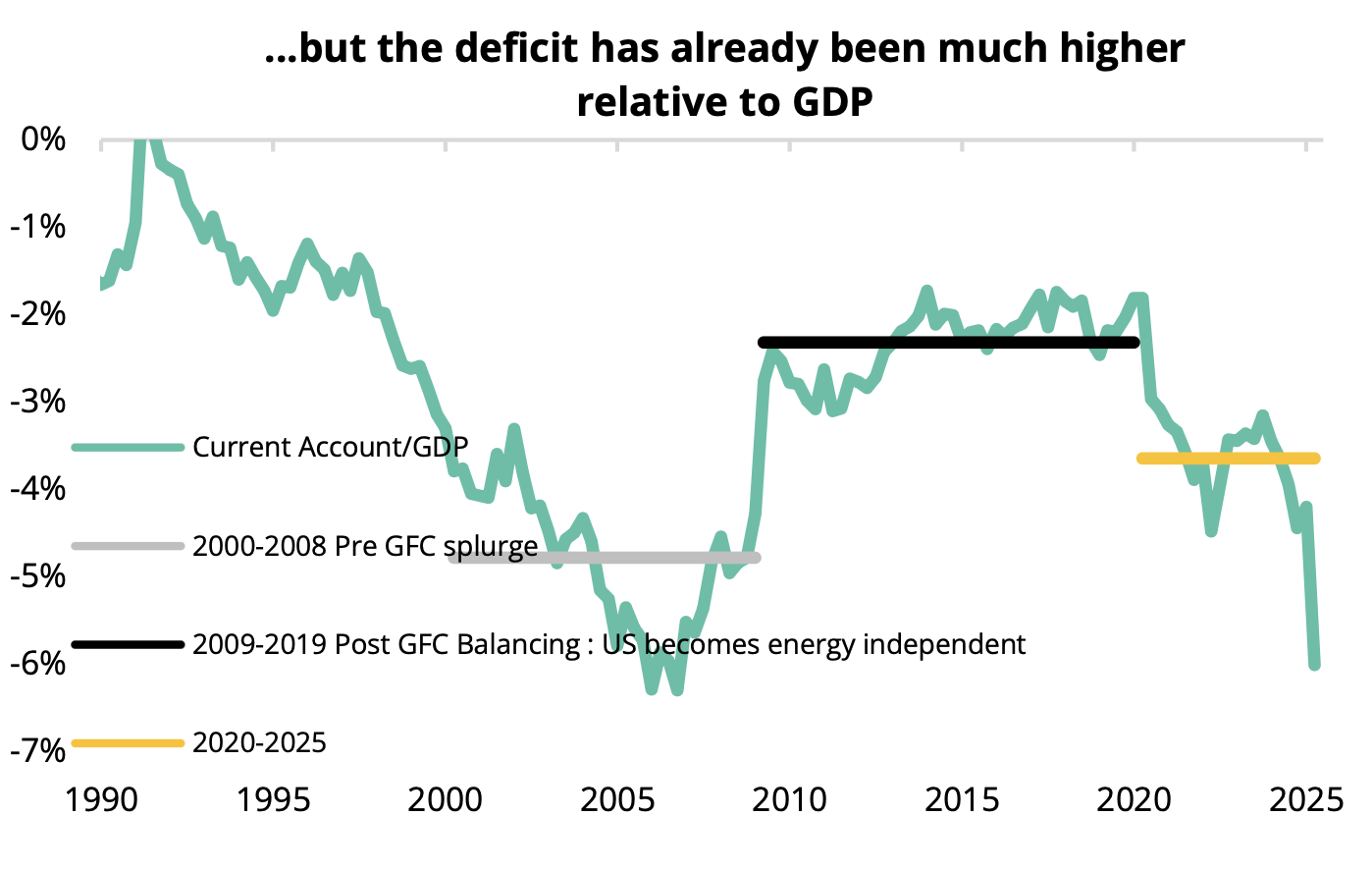

However, while this argument has the merit of reminding us that excessive imbalances sooner or later lead to asset price corrections, it fails to compare the US external deficit to GDP. Since US growth has been robust in recent years, the picture is less worrying, especially if we consider the collapse of the trade balance in early 2025 (explained by the surge in imports aimed at filling inventories before Trump’s tariffs) to be exceptional. The weight of the balance of payments deficit in GDP was more worrying in the decade leading up to the 2008 crisis, a time when America was literally absorbing excess global savings. Therefore, we can conclude that the US external deficit is not so extreme as to require an immediate dollar correction.

Sources: Silex, FactSet – data as of 30/07/2025

Past performance is no guarantee of future performance.

d. The current account deficit is not as huge as it seems

A strengthening of the dollar or a pause in its weakening must come from flows more favorable to the greenback. We can identify three segments of the financial markets that can generate this type of behavior.

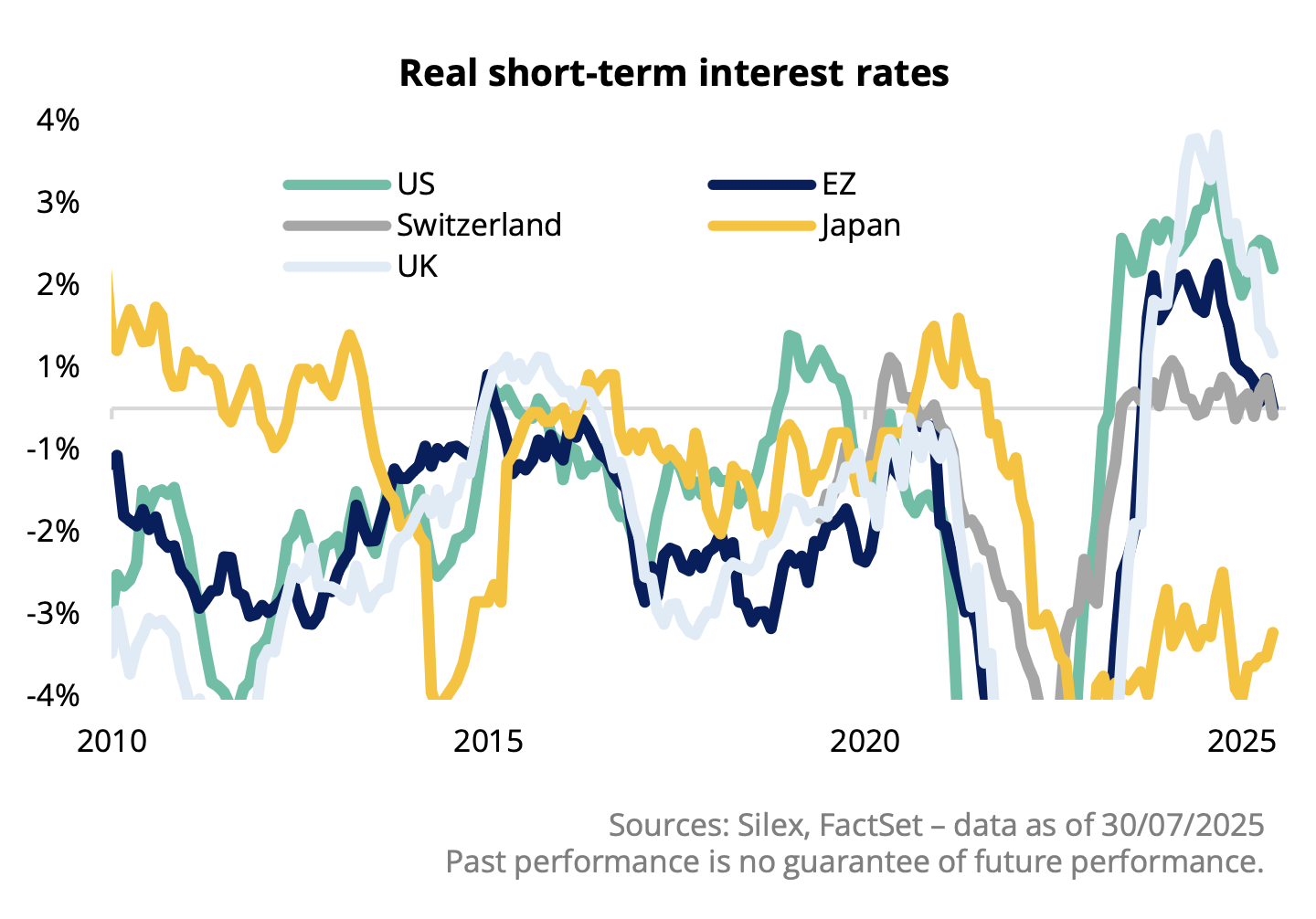

- To begin, let’s look at short-term rates. In the wake of the rate-cutting campaigns of the SNB, the ECB, and, to a lesser extent, the Bank of England, real rates (after inflation) are now negative or close to zero in all G7 countries, with the exception of the United States, where they are around 1.7%.

Sources: Silex, FactSet – data as of 30/07/2025

Past performance is no guarantee of future performance.

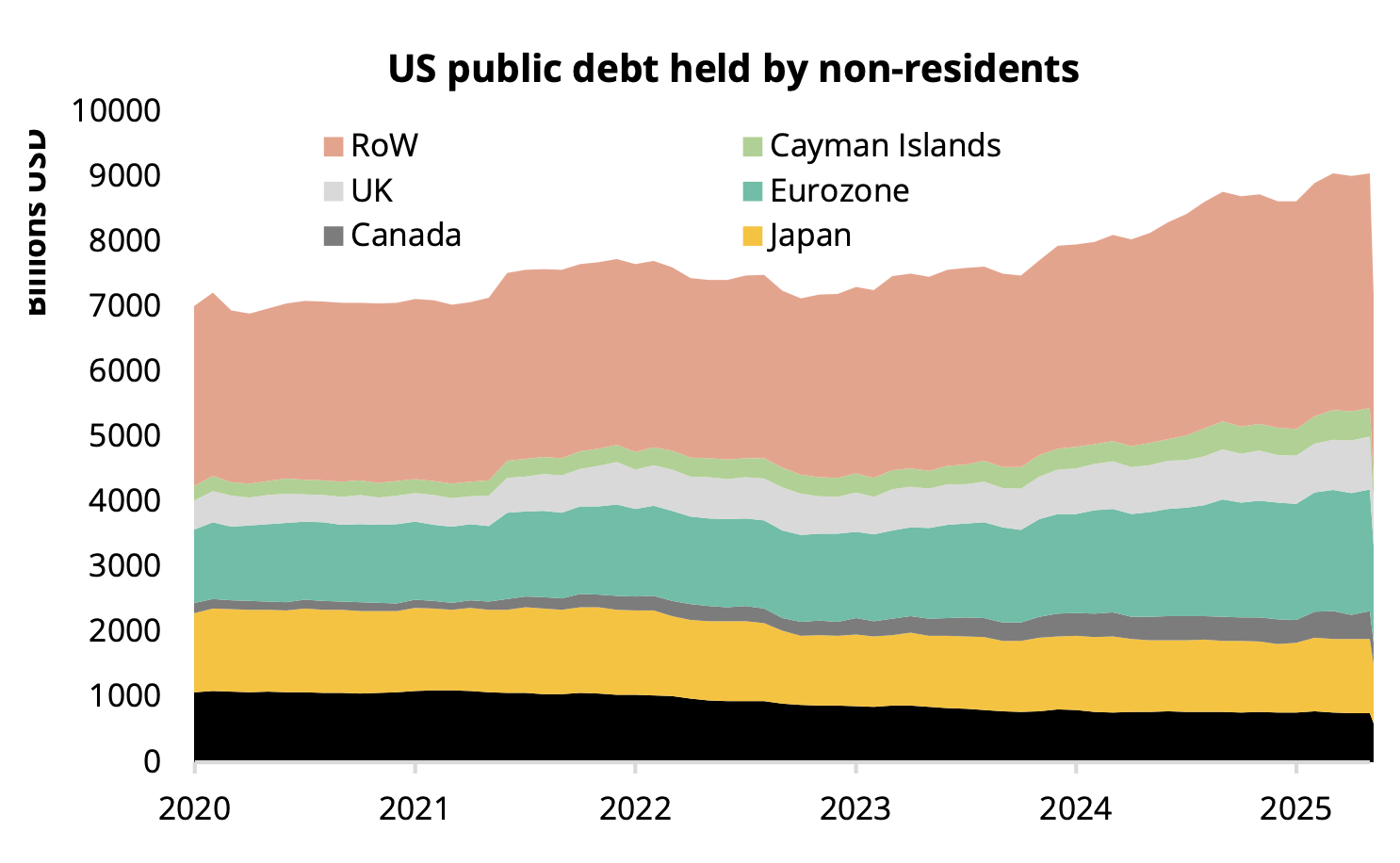

- In terms of longer-term debt, it should be noted that the United States has continued to issue debt, due to a colossal budget deficit. Even though three-quarters of this debt is held in the United States, foreign investors are still keen on American paper, even though the countries have changed somewhat in recent years. With repeated trade pressures on China for more than 10 years, the Middle Kingdom has significantly reduced its holdings of US Treasury bonds. But China is an exception, as the G7 countries have either stabilized or increased their holdings, like the Eurozone. The United States has therefore had no trouble “exporting” its debt.

Sources: Silex, FactSet, OPEC – data as of 30/07/2025

Past performance is no guarantee of future performance.

In terms of equity markets, the weakness of the greenback in H1 2025 also corresponds to the temporary weakness of the American tech giants, first at the end of January with the announcement of Chinese competition in the field of artificial intelligence embodied by Deepseek, then because of the fear of customs duties. Since April, earnings releases and pre-announcements have tended to reinforce the thesis of the strength of technology giants in the field of artificial intelligence with massive investments that also benefit from the support of the American administration with the publication of a decree on July 24 to accelerate the development of AI infrastructure and the resumption of exports of chips dedicated to the Chinese market. Investments in AI are not weakening and this growth is proving profitable, all of which should further attract flows towards American stocks in the absence of a credible alternative in the rest of the world.

Factors influencing the dollar: estimated impact for the next 6 months

| Reserve currency | + |

| Military power | + |

| USD positioning | + |

| Rate short- term real | + |

| Customs duties | + |

| Flow to US tech giants | + |

| GDP growth gap | + |

| Current account | = |

| Holding US debt | = |

| Currency hedging | = |

| Independence of the Fed | - |

| Valuation in purchasing power parity | -- |

| Economic Doctrine (Miran) | -- |