Preliminary signs of de-escalation at the start of last week ultimately proved misleading, and the conflict in the Middle East continues to intensify. Our base case still assumes a near-term resolution, as it remains in the interest of all major stakeholders (the US, Europe, China, and Gulf countries). However, risks are clearly skewed to the downside. Iran has gained significant leverage through the blockade of the Strait of Hormuz and does not appear eager to reach a deal. At a minimum, Tehran seems intent on imposing its own terms – namely, financial compensation and/or control over Hormuz - which are unacceptable to the rest of the world. The longer disruptions to energy markets persist, the greater the damage to the real economy and corporate earnings.

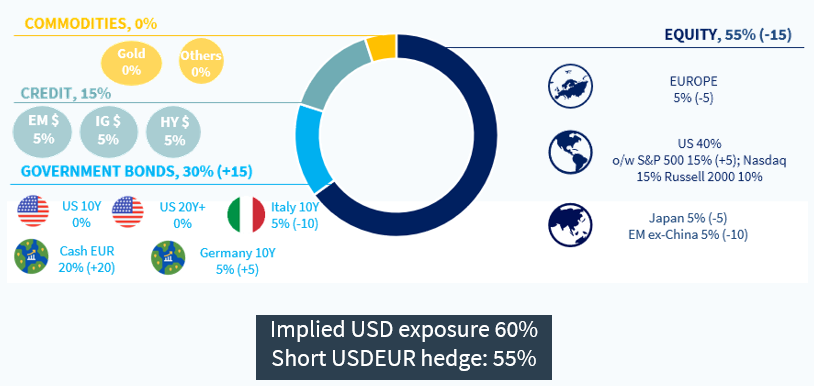

Against this backdrop, we trimmed our exposure to risk assets at the end of last week and now hold 20% cash in our model portfolio. We reduced exposure to the segments most vulnerable to energy supply disruptions: Euro area equities, EM Asia, Japan, and Italian BTPs. That said, as a swift reversal cannot be ruled out, we maintain a slight overweight in equities (55%), primarily through US equities (40%), following a 10% drawdown from the peak.

While we typically maintain a medium-term perspective, the rising likelihood that oil prices remain above $100/b for several more weeks is prompting a more tactical stance. Weekend reports suggesting the conflict could last an additional 2-4 weeks add to the downside risks.

- Time is running out. As shown in slide 7 of the report, alternative supply sources (unsanctioned Iranian and Russian inventories, as well as IEA strategic reserves) have partly offset the estimated 8.8 mb/d shortfall in crude and refined products caused by disruptions in the Strait of Hormuz. However, even if the conflict were to end immediately, we estimate it would take around 30 days to restore production and shipping flows to Asia. In short, if the conflict persists beyond the next ten days, a meaningful slowdown in global growth is likely, and Brent crude could rise towards $150/b.

- In such a scenario, we may need to further reduce equity exposure in the coming days. That said, a sudden policy reversal from Trump or a breakthrough agreement with Iran cannot be ruled out.

We see three broad economic outcomes: 1) a quick resolution is reached, with limited damage to the global economy (best case, whose probability has declined); 2) structural damage to oil infrastructure triggers a prolonged energy shock (worst case); and 3) a scenario in between (1) and (2), where the conflict continues with a partial reopening of Hormuz (the current situation). From a market standpoint, investors face an imminent binary scenario of either an immediate deal or further military escalation with unpredictable consequences. The entry into the war of the Houthis during the weekend further increased the odds of the latter scenario. Under the quick resolution scenario, we expect Brent oil prices to average USD80-90/b until end-Q3 and to cool down to USD75/b at year-end.

The inflation outlook appears more manageable today than in 2022, which is supportive for bonds. While central banks clearly have the 2022 playbook in mind, there are important differences in the current environment.

- In the US, household savings are now very low, whereas they were elevated in 2022 (post-COVID), enabling consumers to sustain strong spending. At that time, resilient consumption was reinforced by expansionary fiscal policies, further fueling inflation. No comparable fiscal support is expected in 2026.

- That said, central banks are likely to remain highly sensitive to upside inflation risks, particularly given that they were late to tighten policy in 2022.

- Our conclusion is that bond duration still faces near-term headwinds as markets reprice central bank rate expectations. However, the global economic backdrop appears more vulnerable to shocks than in 2022. In this context, duration could soon become attractive if downside risks materialize, likely in the form of a sharp slowdown in growth rather than a renewed surge in inflation.

Finally, we believe several themes will emerge structurally stronger from the crisis.

- Defence and sovereignty, which we have been discussing in this report in recent weeks.

- Electrification should also benefit from the current energy crisis. We keep an Overweight stance on Utilities and believe that renewables may also emerge stronger, especially in Europe.

Asset allocation: Sharpe 1 strategy