Attacks on energy infrastructure last week marked a serious escalation in the Middle East conflict. Meanwhile, memories of 2022, when inflation climbed to multiple-decade highs, have forced central banks to communicate on the possibility of rate hikes ahead. Fears of renewed inflation have translated into a selloff at both the short and long ends of the curve, as energy subsidies could further widen budget deficits. For investors, that leaves limited options to protect portfolios, and cash is king. Like in 2022, even gold has failed to protect portfolios, as the rise in bond yields increases the opportunity cost of holding gold.

The real damage to the economy will depend on how long the conflict lasts. Like us, most investors we have talked to assume that it will be short-lived, as the US, Europe, and China have a strong interest in preventing a prolonged spike in energy prices. Yet, as Iran is setting its own conditions, an unsecure Strait of Hormuz could be the norm going forward, and the conflict could become a lower-intensity conflict, but with persistently high energy prices.

Looking for convexity. Assuming the conflict ends before the end of March, the damage would be limited, with oil prices easing towards USD80-90/bbl for at least a couple of quarters, in our view. This would still represent a c. 20% increase versus pre-conflict levels, translating into 25bps and 70bps of additional headline inflation in the US and Europe, respectively. The impact would likely be temporary and thus unlikely to result in a significant tightening of monetary policies (unlike in 2022). However, as many investors expect a swift resolution, any further escalation – or just the passing of time without a resolution – could accelerate equity and bond losses, resulting in a concave payoff. The next couple of weeks will be critical in that regard, but as usual, the best opportunities arise when markets panic, which is not yet the case on a broad basis. That said, beneath the surface, some dislocations are beginning to appear.

Excess confidence, the pain threshold, and the “TACO” trade. It is now apparent that after Maduro’s capture in Venezuela, Trump believed Iran would be a quick win. He was wrong to assume that the Revolutionary Guard would fail to fight for the regime’s survival. The blockade of the Strait of Hormuz has emerged as an economic weapon to gain leverage in negotiations, and it was clear to most experts that Iran would not hesitate to use it.

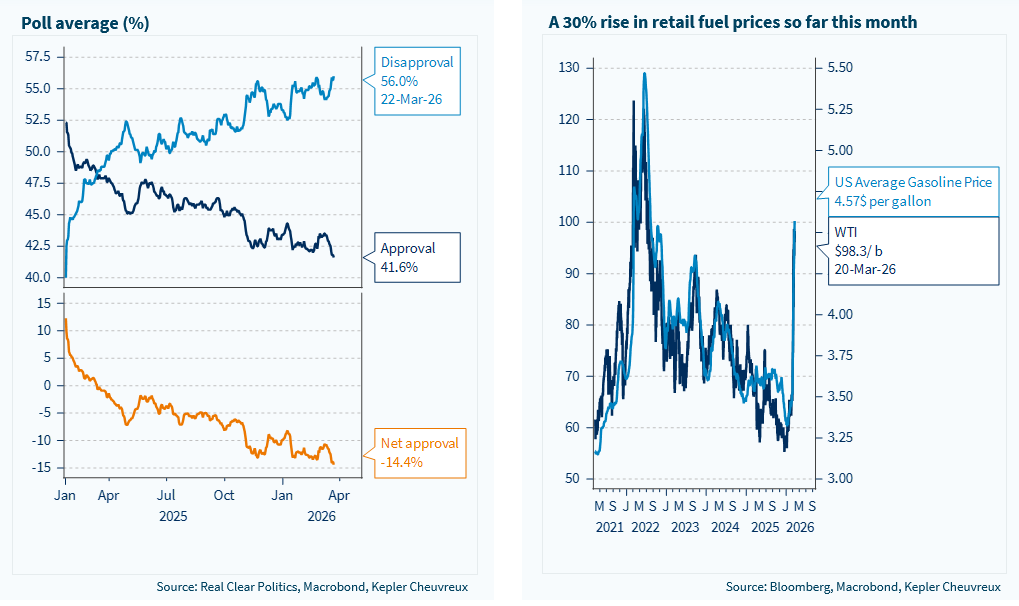

Yet, the pain threshold has already been reached for US voters, with gasoline prices up by more than 30% so far this month. There is a correlation between declining net approval ratings for Trump and rising US retail fuel prices that may force him to back down soon. In sum, while we expect uncertainty to persist in the near term, we continue to see the risks to global economic activity as relatively moderate. This energy shock may not cause a global recession, and a 10% additional global equity market pullback would begin to look attractive to us. In the meantime, we believe it is prudent to keep some powder dry and adopt a more cautious tactical stance in our asset allocation, including a downgrade of energy-sensitive EM equities. This further extends the de-risking of our portfolio, following last week’s downgrades of European equities and Italian BTPs.

Nuclear energy: a structural investment theme. Geopolitical risk and tensions over energy supplies are durably reinforcing the themes of energy independence, defence, and sovereignty, which we have discussed in editions of this report in recent weeks. Europe’s and Asia’s dependence on fossil fuels represents a major source of vulnerability – one that has been brought back into sharp focus by recent developments. Even ahead of the spike in recent geopolitical tensions, the nuclear sector was regaining a central role in energy policies, driven by a shared imperative to produce stable, decarbonised, and sovereign energy. In 2022, the EU included nuclear in its green taxonomy, recognising its contribution to the fight against climate change. This decision paved the way for a massive return of institutional investment in the industry. France has launched the construction of six new reactors, Japan has reopened plants shut down since 2011, and more than twenty nations have committed to tripling global nuclear capacity by 2050.

Investor interest in nuclear power reflects this paradigm shift. According to Kepler Cheuvreux’s TrackInsight, assets invested in nuclear themed ETFs increased by more than 60% between 2023 and 2025, signalling growing enthusiasm for an energy source increasingly perceived as green, strategic, and sustainable. This rise reflects a profound market repositioning, in which nuclear power is once again becoming a natural component of portfolios focused on the energy transition. We show in this report a global equity basket of nuclear names covered by our equity research team (and partners), as well as several ETFs that provide exposure to the theme.

Trump’s approval ratings are falling fast, as retail fuel prices climb