In a context where US inflation came in below expectations for December, bond markets rebounded after difficult weeks which saw 10-year Treasury yields approaching the 5% psychological threshold. The relief in bond yields also took place as Scott Bessent, the Treasury Secretary nominee, had a confirmation hearing before the Senate last week. He expressed his support for an independent central bank and the need to address budget deficits. He is highly likely to be confirmed, a positive for risk sentiment.

The relief in bond yields had global implications, with rates in the euro area heading south as well last week. Yet, going forward, bond markets remain on cautious mode and continue to express concerns over Trump’s trade and immigration policies which could reignite inflation. Our view is that Trump will prove less controversial than feared but he is still expected to cause a higher volatility regime across market segments.

In Europe, the luxury sector, which we find attractive form a midterm perspective, was boosted by strong quarterly earnings from Richemont. Led by high-margin jewellery and own retail, and without a recovery in China, the magnitude of Richemont's holiday season trading beat cannot be overstated. In our view, the luxury sector is hampered by its exposure to the Chinese consumer, which remains in the doldrums, but markets still underappreciate its exposure to the US consumer, which remains a tailwind.

On the French political front, the new government survived his first confidence vote, which has contributed to ease the French sovereign CDS spread. The far-left France Unbowed party filed a no-confidence motion against Bayrou’s government which did not pass as Socialists and the far-right did not supported it. We believe there is room for French political tensions to cool down and we expect this government to stay in power in H1-2025. This is proving supportive for OATs and French banks, though the road ahead is likely to remain bumpy.

In this report, we focus on European credit, and on hybrid notes in particular. This segment of European credit markets experienced stellar returns in 2024 and is an appealing alternative to high yield credit in our view. We show in the report that returns last year were boosted by the real estate sector, which is unlikely to be repeated in 2025 as spreads tightened significantly. Yet, we believe the average premium of 100bps that hybrids now offer compared to the corporate BBB index (excluding financials) remains attractive in the current market context. The investment-grade issuers – including for hybrid notes – continue to enjoy abundant access to the primary market and extension risk is limited. However, investors may become more selective in their investments. In conclusion, we reiterate our recommendation to overweight corporate hybrid notes over investment grade senior peers. We continue to favour large hybrid issuers with established call and replacement policies, such as Enel, EDP, Repsol, TotalEnergies, and Volkswagen. Additionally, we see opportunities for companies like Naturgy and Syensqo, which are removing hybrid bonds from their balance sheets.

In conclusion, we reiterate our recommendation to overweight hybrid corporate bonds relative to high-quality senior bonds. We continue to favor large hybrid issuers with well-established repurchase and replacement policies, such as Enel, EDP, Repsol, TotalEnergies, and Volkswagen. Furthermore, we see opportunities for companies like Naturgy and Syensqo, which are removing hybrid bonds from their balance sheets.

What’s to come this week: earnings season will pick up speed, the BoJ is expected to raise rates, and January PMIs will be available for major economies.

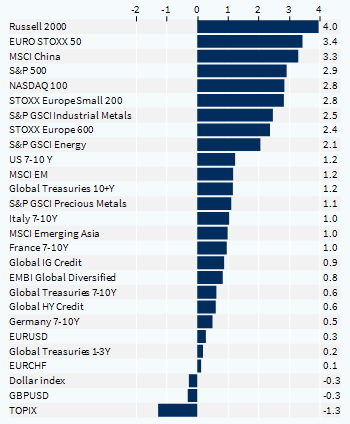

Cross-asset performance (last week, %)