Reflecting current dynamics in the newsflow, we emphasise four core convictions in our weekly report.

#1: Trump’s tour of Asia. Highlighting the major role of the Asia-Pacific region in the world economy, Donald Trump has kicked off his first trip to the Asia-Pacific region since his re-election by attending the ASEAN summit in Malaysia. He signed a flurry of deals on trade and critical minerals with Malaysia, Cambodia, Vietnam and Thailand.

- As we go to press, Trump is now in Japan, and he will meet Japan’s freshly elected PM Sanae Takaichi.

- He will then head to South Korea for the APEC summit, where he is expected to hold a much-awaited meeting with Xi Jinping.

- As expected, trade talks between the US and China will materialize, and a trade deal with China appears imminent.

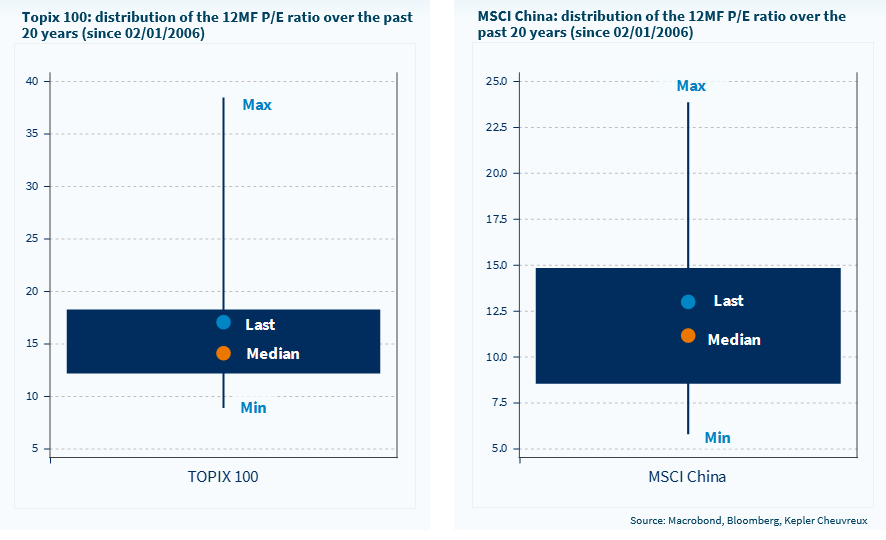

- We reiterate the Overweight stance on China/ Japan equities, as part of a diversification bucket outside US & European equity markets. We show in the report that equity market valuations are much less stretched than in the US.

#2: Despite rich valuations, the US tech rally remains unstoppable. This week will see the release of quarterly results from US Tech giants (and related companies): Microsoft, Meta (Facebook), and Alphabet (Google) will report on 10/29. Apple and Amazon will report on 10/30. Nvidia will report on 11/19.

- These stocks have an exceptional track record of both delivering earnings growth (ranging from 15% to 30% per year over the past five years) and earnings surprises versus consensus expectations. For example, Microsoft has consistently beaten consensus expectations since 2020, except for one quarter.

#3: Fed/ ECB monetary policy meetings. The ECB is unlikely to cut rates, while the Fed is expected to deliver a 25-basis-point reduction. The monetary easing theme can be implemented through curve steepeners or more broadly by taking positions on bond duration.

- This theme also has spillover effects on equities, notably through liquidity conditions. The Fed is expected to announce the end of quantitative tightening this week (ending balance sheet reduction).

- In the euro area, while the ECB has anchored rate expectations at current levels (no further cuts in the short term), we believe weak growth should pull inflation below the 2% target and force the ECB to lower its policy rates below 2% in H1-2026.

#4: In France, the attention will remain focused on the tense negotiations for the 2026 budget and how to tax more in a country that is already the champion of taxation. In the coming days, the taxation of large fortunes will be debated, and with the Socialists currently having the upper hand in Parliament, some symbolic measures will likely be adopted along with the (partial or total) rollover of the exceptional corporate tax for next year. Political stability is not guaranteed, but as long as no moderate political party has an incentive to trigger snap elections, this fragile equilibrium will likely persist at least until early 2026. The OAT – Bund spread is likely to remain in the 75-85 bps area.

Week ahead: on top of the earnings reports in major markets and central bank meetings that we discussed in the report, the shutdown in the US is still disrupting macro data releases. Yet, the Conference Board consumer sentiment survey will be available. In Europe, the first estimate of Q3 GDP will be available and is expected to be pretty weak (+0.1% qoq). The unemployment rate and the CPI for October will also be available. In Japan, the BoJ will meet, and the Tokyo CPI, an advanced indicator of the nationwide CPI, will be available. No BoJ rate hike is expected this week.

China & Japan equity markets are both reasonably valued and do not present the symptoms of a value trap