Equity volatility picked up at the end of last week on the back of a higher probability of recession in the US and renewed trade fears. With the great confusion caused by the implementation of US trade tariffs and last-minute deals, market sentiment is deteriorating. The rebound in equities since April pushed valuations to rich levels, and a pullback is probably due. Expectations that trade-related issues would get clearer after the early August deadline are being revised down. Pharma is again in the eye of the storm of the US administration, and negotiations continue with the EU on some specific sectors.

- The deadline for the eventual implementation of “reciprocal tariffs” is on 7 August, which still leaves room for negotiations (Switzerland, India?). But it is now increasingly clear that the lack of visibility on trade-related issues will persist, most probably until Trump’s term ends in 2028...

- Yet, markets have learned to live with trade wars since his first mandate, and we continue to believe that Trump will try to limit the damage to consumers with exemptions. He is also likely to reverse course if the market sanctions his decisions.

The resilience of the US economy was put to the test with a poor job market report and sharp revisions to recent job creation figures. Job creation in May and June was sharply revised down, by a cumulated 258k, bringing the 3m average monthly job creation to 35k vs 200k earlier in 2025. Yet, these numbers are in contradiction with other job market data, such as initial jobless claims, which have decreased lately, suggesting the picture is better than the revisions suggest.

Tactically, we cut equities to Neutral (from Overweight) and keep a bias towards US equities (slight Overweight) where the earnings season remains supportive. We switched from risky assets to safe assets such as govies and IG Credit in our model portfolio. In Europe, equities have been driven by Financials & Industrials, which may face some profit-taking if markets come under pressure. We turn Underweight European equities but continue to find value in the German stimulus theme. A slowdown is underway in the US and in Europe, which suggests that the risk-reward for risk assets is asymmetric in the near term.

Medium term, we remain constructive. The macro headwinds related to trade tariffs should eventually be manageable as businesses have learned to live with complex supply chains since COVID-19. There is a likelihood that the trade tariff impact can be absorbed without causing severe price rises or provoking a slump in demand. Meanwhile, we expect the US administration to mitigate the damage to the economy with exemptions, having in mind the late 2026 midterm elections.

Week ahead: with the US earnings season soon coming to an end, the corporate newsflow will soon be much lighter (Nvidia will release quarterly earnings on 27 August). In Europe, there are still more than 200companies that are due to report quarterly earnings in the coming weeks.

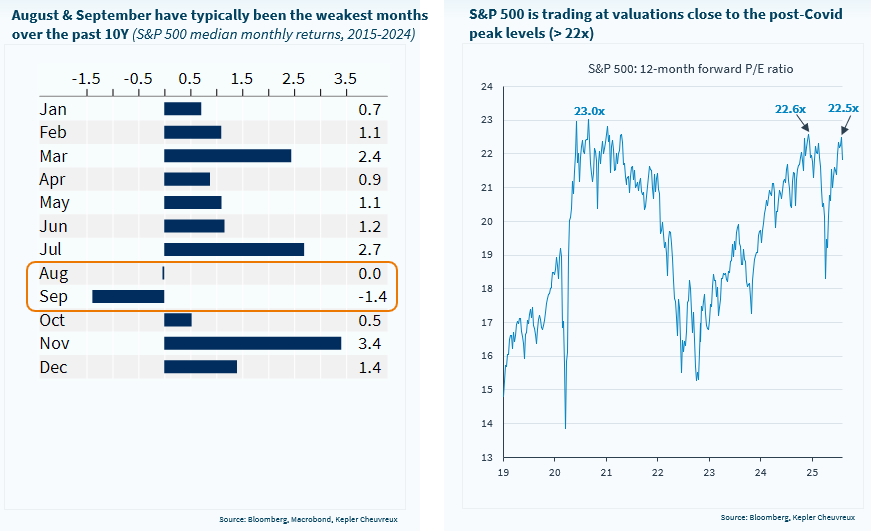

Coupled with weakening job figures in the US, seasonality and rich valuation leave global equities vulnerable in the near term