After several months of strong positive returns, global equities are taking a breather. US and European indices reached an all-time high in late October and are experiencing a mild pullback as we speak. Against a backdrop of rich US market valuations, uncertainty has risen over the trade tariff impact on job creation and, in the end, consumer spending.

- The longest government shutdown on record is preventing investors from having access to critical information on the labour market and personal spending dynamics. Powell also noted recently that the unavailability of economic data may lead the Fed to pause its cutting cycle, as FOMC participants could judge that moving more slowly is the better option when “in the fog”.

- Last week, the Challenger Job Cuts Report, a monthly publication by one of the major outplacement firms, signalled massive layoff announcements by U.S. companies in October. To add some drama, Bloomberg reported that it was the "Most October Job Cuts in Over 20 Years". However, we note that the Challenger survey has been far from a particularly reliable indicator of labour market trends in the past. Also, other alternative data, which are usually more closely correlated with the official job numbers, have been striking a less worrying note. In particular, while both the ADP and the Revelio reports suggested that job creation remained subdued recently, they did not point towards an incremental and material weakening of labour market conditions.

- The S&P 500 is down 2.5% from the peak, and the Nasdaq 100 -4.1%. With most US companies having reported earnings, the market might lack catalysts to fuel renewed optimism in the near term. In our view, this is not the beginning of a long-lasting and significant reversal in global equities, but we have tactically cut equities to Underweight early last week. Our technical analyst expects the pullback to complete near the 50-day moving average of 6,650 on the S&P 500 and argues that a break of 6550 would confirm a bigger reversal is in play.

A preference for low volatility stocks. Although this approach does not outperform all the time, it is attractive at present in our view, as the strong recent performance and rich valuations create an incentive to crystallise returns in portfolios at this stage of the year. This could lead to additional selling flows in the coming weeks. From a strategic standpoint, the “low beta or low volatility anomaly” has long been documented in the financial literature. It suggests that low-risk stocks have better risk-adjusted returns than high-risk stocks over time, as they experience much more moderate drawdowns.

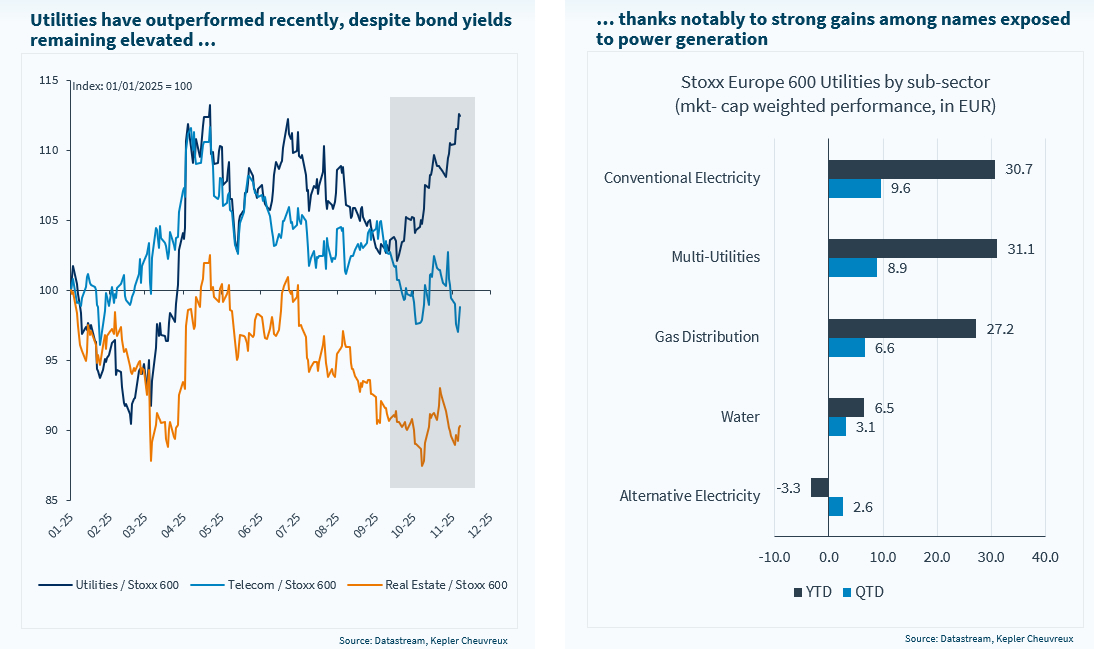

Utilities rank as one of the least volatile sectors, and we are reiterating our Overweight stance on the sector. While defensive and high dividend by definition, the sector has emerged as an AI ecosystem play around the topic of soaring electricity demand related to AI and the boom of data centres. The sector is very heterogeneous from an industrial standpoint, with companies ranging from renewable energy players to energy networks, power generators, waste/water and integrated utilities. Yet, the dispersion of stock returns within the sector is moderate. All the stocks in the sector have a market beta below 1 (vs. STOXX Europe 600), and the average beta is 0.5. From a statistical standpoint, it is thus more homogeneous than meets the eye. Compound earnings growth has also been quite strong in the past five years, despite the fact that this is considered to be a low earnings growth sector.

- The most preferred stocks of our equity analysts are EDP, E.ON, Elia, National Grid and Engie, while Iberdrola, Enel and RWE also remain strong convictions. The least preferred are Hidroelectrica, CEZ and Fortum (link to report).

Soaring electricity demand, data centres: is the hype justified and how to play it? According to a recent McKinsey report, data centres are projected to require USD6.7trn worth of capex worldwide by 2030 to keep pace with the demand for compute power. Real estate, construction and utilities will thus benefit from the side effect of exponential AI adoption. The strong increase in electricity demand from data centres is expected to support growth in electricity use in the medium term, but it is also raising some concerns over the pressure on electricity prices. The most recent IEA report states, nonetheless, that the issue is not imminent. Global electricity demand is forecast to increase by an average annual 3.7% in 2026, a moderation from 4.4% last year, but still one of the highest growth rates observed over the last decade.

- In the report, we provide an update on the KC Solutions nuclear strategy, as AI and growing electricity demand are major drivers of the nuclear revival. When we launched the strategy a few months ago, we noted that policy support for nuclear energy is strengthening in many countries, as it is one of the cleanest sources of scalable electricity production. Concurrently, several influential US tech companies have been signing deals with nuclear players or start-ups to gain access to reliable electricity for their hungry data centres around the clock.

- Flows and performance. Based on our Trackinsight database, lately we have observed massive inflows into nuclear ETFs. Performance is also meeting expectations. Since the launch of our thematic a quarter ago, our strategy is up by almost 35% (in euros) versus +11% for the MSCI World (in euros).

Within bond proxies, Utilities are standing out thanks to AI